The heady days of summer

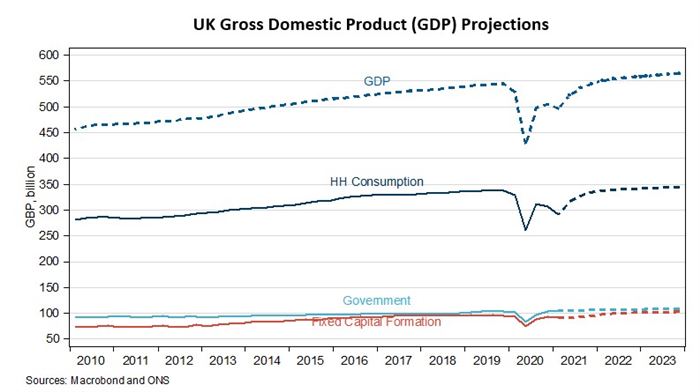

The UK economy continues its healthy expansion, driven by a consumer recovery in retail, as well as social spending. Accommodation and food service activities increased by 87.8% in Q2, (recent figures are being measured against the depths of last year’s downturn) while wholesale and retail trade increased by 12.8%, in response to the re-opening of indoor hospitality, Euro 2020 and the reopening of non-essential retail. Accommodation will receive a further boost in the months to come as international travel remains more difficult than it was pre-pandemic and many people are "staycationing" in the UK this summer; although, staff shortages may become problematic as the summer progresses. This driving force of consumer spending will naturally fade over the coming year as income that had been saved is fully reallocated back to pre-virus norms. But business investment will take its place as the dynamo in the economy and we expect this to expand by over of 12% in the next two years, driven by: the investment of as much as £120 billion in accumulated savings; the Budget generously having raised tax allowances for investment against corporation tax to 130%; and it is becoming is ever clearer where productive investments might be made. Taken together these factors result in our forecast for UK GDP expanding by 7.2% in 2021 and 5.6% in 2022, before tax rises needed to consolidate public finances begin to take GDP growth below trend to 1.3% in 2023.

Finally some guidance on the way forward

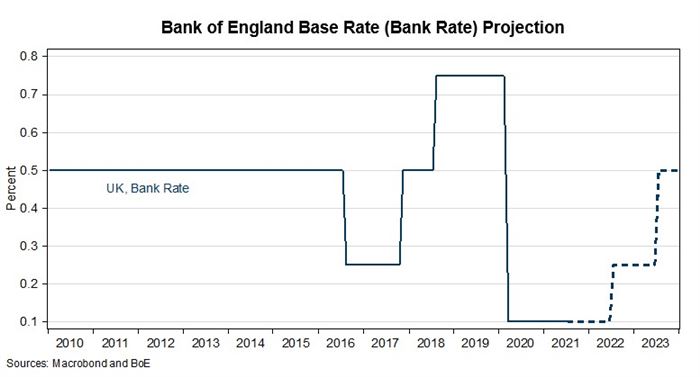

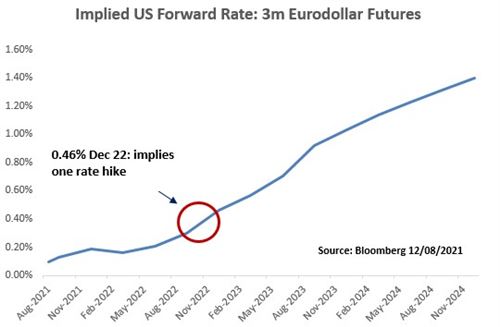

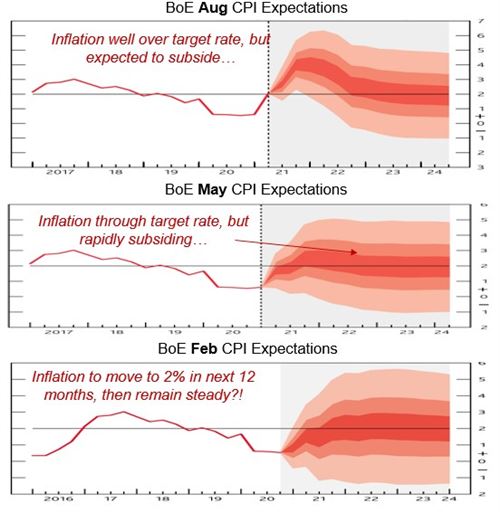

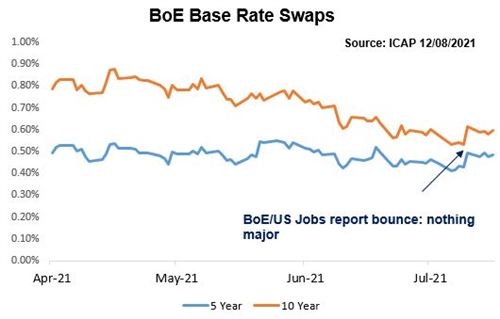

The Bank of England Monetary Policy Committee (MPC) has given some clarity on their thinking about when monetary policy might be tightened, indicating they intend to maintain record low interest rates until the economy has recovered and average inflation is sustainably above its 2% target rate. As to the £895 in Quantitative Easing (QE), the Bank of England (BOE) will start to wind this down when interest rates reach 0.5%, which they suggested is likely to happen over the coming three years. We are forecasting interest rates to remain at 0.1% through 2021, before rising to 0.25% in the second half of 2022 and rising again to 0.5% in the second half of 2023. Inflation remains the danger. The Bank of England forecast in Feb 2021 that inflation would meet its 2% target by the year end, and in fact that level was reached by midyear. However, the Bank continues to believe, and we concur, that much of the inflationary pressure is transitory and inflation will fall back to its target level over the course of 2022, although not before it touches 4% by year end of 2021. Despite this and the unease the House of Lords Economic Affairs Committee has expressed about the Bank aiding monetary financing , investors remain relatively relaxed about the UK government’s overall financial position.