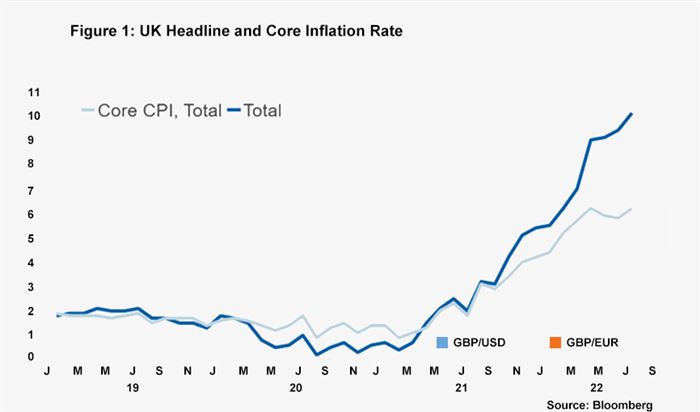

As expected, the Bank of England (BoE) lifted rates by 50bp in August, the first time such an increase has been passed in the quarter century since the bank became operationally independent from government over the setting of monetary policy. This move reflected two fundamental dynamics: the first is that the BoE is conscious of the impact that large increases in interest rates by other central banks will have on sterling at a time when the trade deficit is so high; the second, of course, is that the inflation challenge has become much more acute. The BoE now forecasts that inflation could peak at over 13% in Q4 2022, up from just over 10% in the bank’s May forecast. Subsequently, numbers for both the headline and core rates of inflation for July came in above expectations, leading to speculation that inflation could end up peaking at a higher rate than the latest BoE projections.

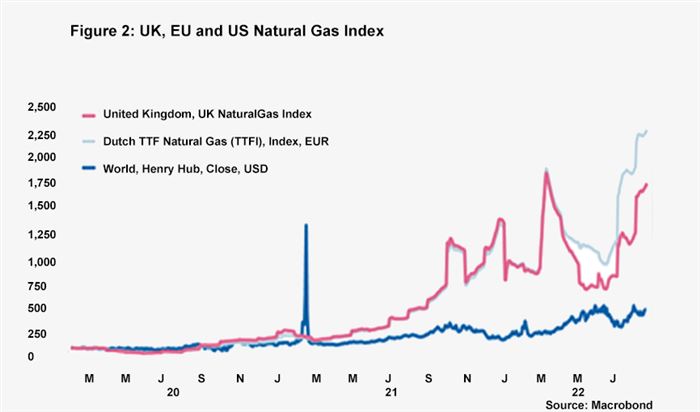

There are factors that should bear down on inflation later this year and early next year, especially the recent drop in supply chain disruption, shipping rates and many commodity prices. This will likely lead to a further divergence between the core and headline rate of inflation, which will be driven by troubles in European energy markets. Natural gas futures in the UK for January 2023 are now around 85% higher than their previous peak in the immediate aftermath of the Ukraine crisis, and it is striking just how much more serious the problem is in European markets compared to those in the US. Since February 2020, the natural gas index has risen by roughly 380% compared to over 1,600% in the UK and nearly 2,200% in the EU (see Figure 2.)

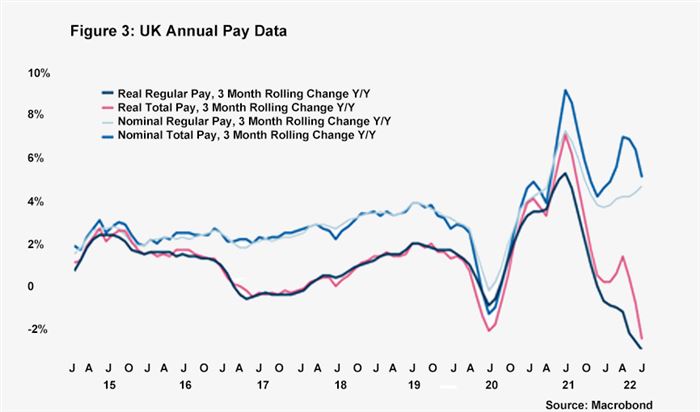

The major risk now for UK and other European markets is prolonged externally-driven inflation stoking domestically-led inflation. Conditions in the labour market may exacerbate this risk in the UK: unemployment remains low at 3.8%, inactivity levels – particularly in the 50-64 demographic – remain elevated compared to pre-pandemic levels and pay growth is higher than the BoE is likely to tolerate. Pay settlements, while considerably below inflation, are historically high. According to latest ONS figures, total nominal annual pay growth for the three months to June registered at 5.1% (far higher than market expectations of 4.5%) and the BoE’s Agents’ survey suggests settlements of 6% over the next year – all at a time when productivity is not showing any signs of improvement. According to the Office for National Statistics, average total pay growth for the private sector was 5.9% in April to June 2022, and 1.8% for the public sector. This is by no means pointing to a 1970s wage-price spiral when at one point pay settlements reached 30% and inflation was at 25%, but nonetheless the labour market figures will be weighing on policymakers’ minds.

One positive development in the last few weeks was the better than expected GDP figures for Q2. While growth registered at -0.1% q-o-q, the figures were weighed down by falling pandemic-related spending and the net loss of one working day due to the Platinum Jubilee celebrations. There were some encouraging increases in private sector activity and business investment has seen a partial rebound, although it remains 6% below its pre-pandemic level.

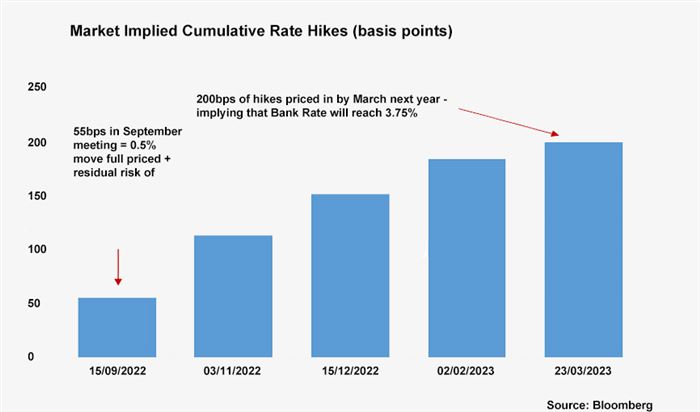

There is no doubt that all of this points to further monetary policy tightening, the question is to what extent? Our base case is that the level of interest rates in the UK will rise from 1.75% to 2.75% year end and remain at these levels during 2023, which is below market expectations that currently project rates rising to 3.5% or 3.75% in 2023. Due to better than expected US inflation numbers, it is plausible that the Federal Reserve may not raise rates as high as previously predicted and the ongoing tensions in the Euro area between tackling inflation and reducing bond spreads will likely constrain the European Central Bank, potentially reducing pressure on the BoE to hike rates aggressively. We also feel that the deflationary impact of quantitative tightening and the subdued economic outlook into the medium term will further moderate prospective increases to interest rates in the UK.

Daniel Mahoney, UK Economist