Tightening cycle coming to its conclusion: What next?

MPC split three ways as Bank of England hikes by 50bps

The Bank of England's (BoE's) Monetary Policy Committee (MPC) voted by 6-3 to raise interest rates by 50bp in December, meaning UK interest rates now sit at 3.5%. A 50bp hike had been priced as the most likely outcome by markets. There was a small probability of the BoE going further with a 75bp hike, but data released in the run up to the decision, showing a marginal easing in the labour market and inflation coming in lower than expected, will no doubt have tilted the balance of opinion on the MPC towards a 50bp hike.

However, there are clearly huge differences of opinion among the MPC on the right course of action. One member of the committee was in favour of a larger 75bp increase, on the basis that price and wage pressures could stay stronger for longer than projected in the BoE's November report. On the flip side, two members voted for no change to interest rates at all, arguing that the current bank rate was more than sufficient to bring inflation back to target in the medium term, given weakness in the UK economy.

Tightening cycle is coming to a close: what next?

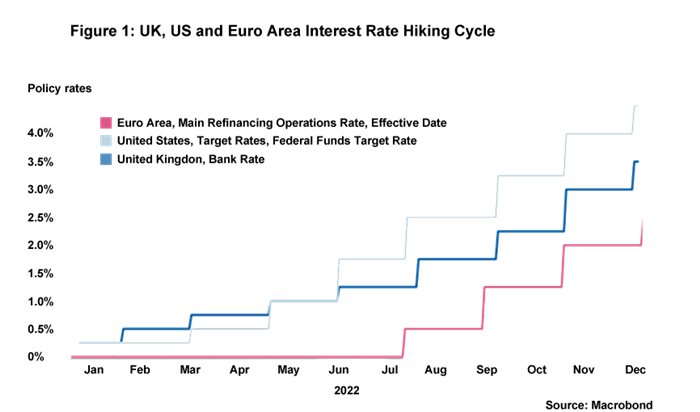

Despite the split opinion amongst the MPC, it is clear that central banks across the Western world now appear to be approaching the peak of interest rates in this tightening cycle. The US Federal Reserve increased rates by 50bp in December, down from its previous four hikes each of 75bp. The ECB also pivoted to a 50bp increase in December – although, judging by Christine Lagarde’s hawkish press conference, there may be more tightening to come in the Euro Area compared to the UK or the US. This is, perhaps, unsurprising given the Euro Area’s tightening cycle started at a later stage (see Figure 1).

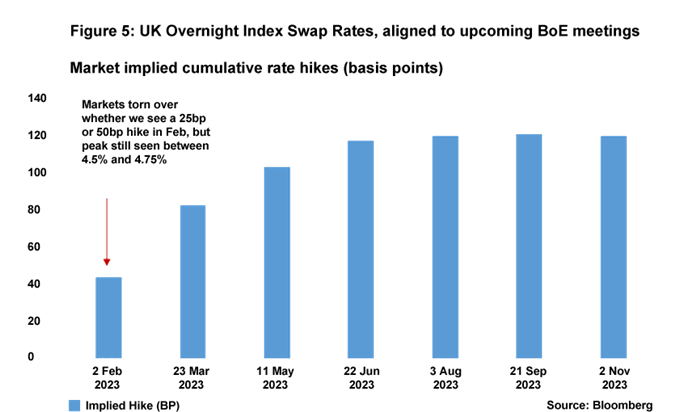

The two key questions for UK monetary policy now are where will interest rates peak and how long will they remain at the peak? The MPC will need to weigh up various competing priorities. The BoE confirms that the UK is probably in recession (GDP grew by 0.5% m-o-m in October, but this was only due to September’s print being artificially depressed by an additional bank holiday; the BoE is still predicting negative growth for Q4), which will act as a natural brake on inflation. The MPC will also be conscious of financial stability risks arising from the already started correction in the property market. All things considered, we are of the view that the BoE will increase rates further to a peak of 4%, below current market expectations.

With the proviso that we do not experience a fresh geopolitical shock, it seems likely that CPI inflation's peak was in October, with the rate falling by 0.4pp y-o-y in November to 10.7%. Factors including energy price base effects, falling supply chain disruption and collapsing shipping costs will all work to reduce inflation in 2023. That said, we do not anticipate that inflation is going to be falling close to its 2% target level in the short to medium term. Services inflation, in particular, is likely to be more difficult to remove from the system due to domestically-led pressures. At this stage, we believe this will lead the BoE to hold rates at the peak of 4% throughout 2023 and into 2024.

Quantitative tightening will further tighten financial conditions

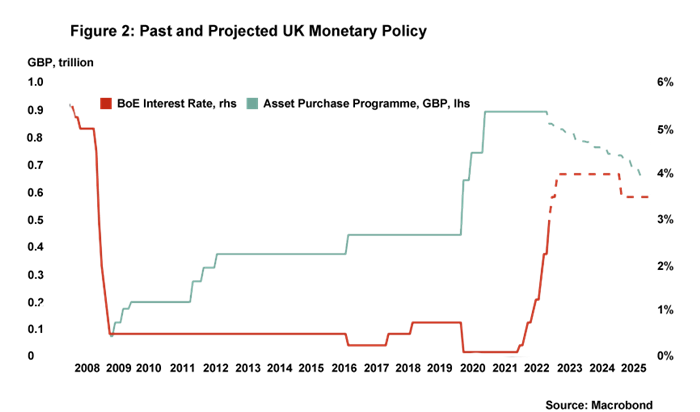

Quantitative tightening (QT), the reduction of holdings in the Asset Purchase Programme, is also a factor to take into consideration when assessing the direction and scale of future monetary policy. Assuming the BoE proceeds with the full GBP 40bn of active sales and continues passive QT (not buying new assets to replace ones that mature) until mid-2025, the BoE will have reduced its Asset Purchase Program by roughly a quarter from its GBP 895bn peak (see Figure 2). A cautious estimate, based on evidence from the United States, suggests that this would be the equivalent of increasing interest rates by 50bp on a sustained basis. Handelsbanken UK will be publishing a paper examining the potential impact of QT early in the New Year.