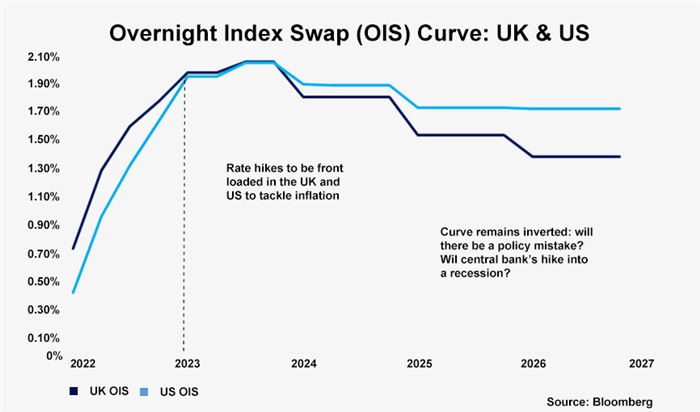

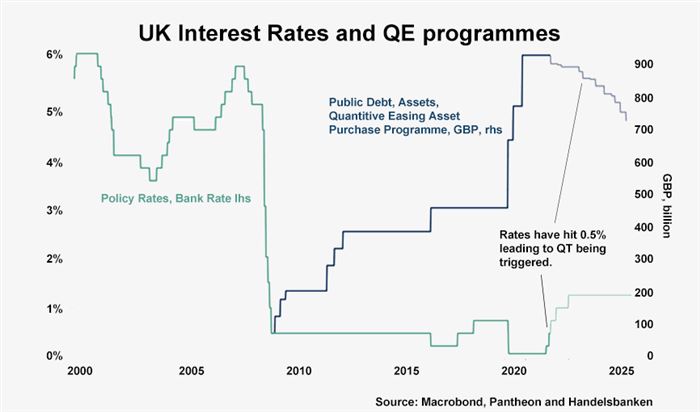

Rates to rise further in 2022; Quantitative tightening begins in March

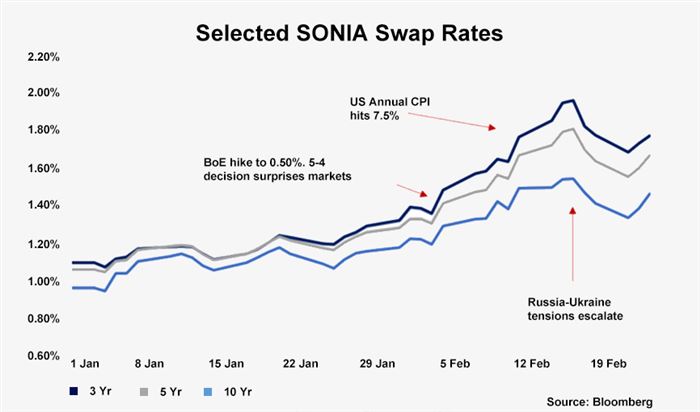

The advent of serious conflict in the Ukraine is clearly going to have an impact on the macro-economy, although the extent of that depends upon the scale of that conflict. To recap: the Bank of England (BoE) increased interest rates by 0.25 percentage points to 0.5% in February, with four out of nine rate-setters pushing for a higher increase of 0.5 percentage points. Along with higher borrowing costs, rates hitting 0.5% has triggered the process of quantitative tightening (QT). This initial phase of QT will involve the BoE not re-investing the proceeds from maturing assets in its Asset Purchase Programme, most immediately the £25bn of gilts set to mature on 7 March. It’s estimated that the impact of this rise will be equivalent to a 30 bp rise in interest rates. This QT marks the start of a process which is projected to see over one-fifth of the Bank’s bond holdings being wound down by the end of 2025 (see Figure 1). At this stage we expect this process to continue despite the conflict in Ukraine, as inflationary pressures rising and our hawkish stance is supported by reading into the BoE’s guidance, reiterated in Feb, that once rates hit 1% it will consider accelerating QT by actively selling off its bond holdings. Beyond that we expect that rates will rise to 1% in June, although with uncertainties surrounding the impact of QT – including impact on broader asset prices – we also expect the Bank of England to proceed cautiously and for rates to rise to 1.25% in early 2023.

Significant portions of the present inflationary spike are transitory, but regaining the 2% target remains uncertain

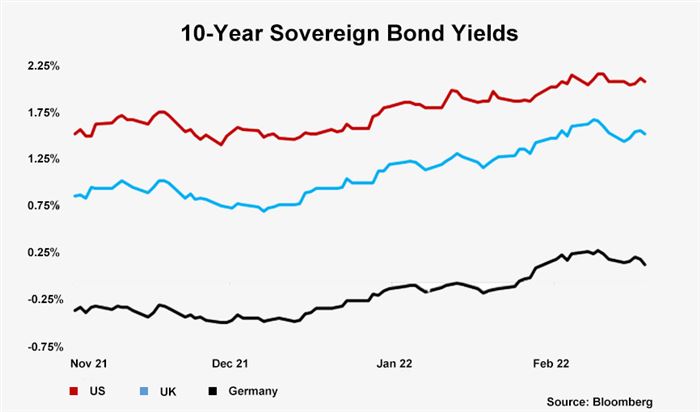

The BoE’s latest estimate is that inflation will peak at 7.25% in April when the lifting of the energy price cap and tax rises kick in; our view had been that inflation would end up being closer to 8%. With energy prices now surging in response to the Ukrainian crisis any hoped for or anticipated easing of energy prices looks to be some way off. The full impact will have to be assessed in the coming days, but the prolonging of the energy price spike makes the spill over from energy to the broader economy a good deal more likely than anticipated and core inflation is already at 4.4%. While the UK does not directly import a significant amount of gas from Russia, consumers will of course still feel the impact of from higher global oil and gas prices arising from a prolonged conflict.

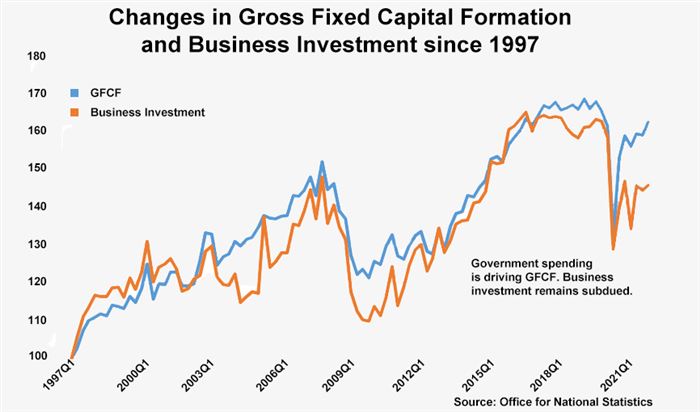

Growth in business investment, key to the UK’s recovery, is likely to be delayed by Ukraine crisis

Economic output has now regained its pre-pandemic level, despite seeing a fall in December due to omicron. However, there were always a number of uncertainties: upcoming tax and inflation pressures in April were already set to suppress consumer spending and we can now add in an additional layer of geo-political concerns. While overall gross fixed capital formation is around its pre-pandemic level, the business investment component remains subdued at around 8% below its pre-crisis level (see Figure 2). Incentivised by measures such as the super deduction – which will give companies investing in new plant and machinery a 130% capital allowance – our projection had been that businesses would start to deploy much of their accumulated savings into the UK economy, helping to drive GDP growth over the next year. It now seems much more plausible that this investment is delayed until later in 2022 when there is likely to be greater clarity on the exact scale of the Ukrainian crisis and its wider impacts.