As always, the economy gives us plenty to think about and there are three key questions going forward:

What is going to drive the recovery over the next year?

Every economic forecast has a degree of uncertainty, but encouragingly there is less doubt in today’s forecasts than normal. Much of this is down to my expectation that the biggest driving force of the expansion is the redirecting of existing income from forced savings to consumption. I am making no heroic assumptions about the desirability of a new product, or forecasting that people will take on more debt; I am merely assuming that as people are allowed out, they are going to want to return to something like normal. Alongside the big boost to consumer expenditure, I am also looking for a reasonable rise in business investment. Brexit uncertainties have been allayed and with consumer habits changing as a result of the pandemic, businesses have the necessary savings to respond to new demands.

When and how will the economy slow?

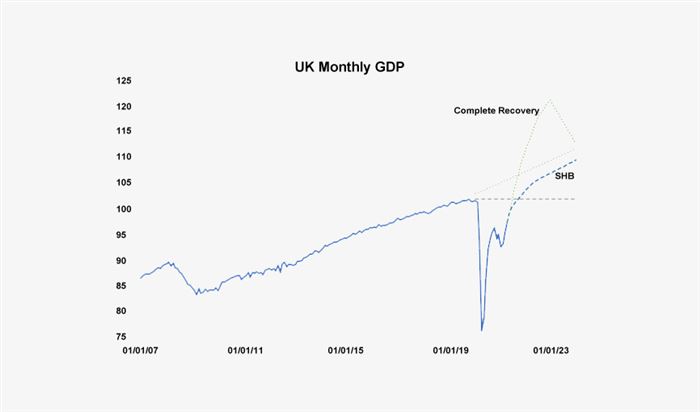

The UK’s long run annual trend rate of growth before the pandemic was some 2 percent. Forecasts vary but the overall economic growth for 2021 could be over 7 percent. Clearly the present rate of growth is not sustainable, thus a good deal of slowing of the pace of growth is going to happen over the course of the coming year. I also do not expect to regain the economic activity that we have lost since March 2020, such a move would require consumers to spend a significant portion of their accumulated forced savings. That said, even accepting a gradually slowing of the pace of growth will take us to the level of GDP seen at the end of 2019 by the end of this year or the beginning of next. This slowing will see consumer spending normalise and the business investment spree runs its natural course. Key to my assumption is that interest rates remain at or near their present low levels.

Is inflation a threat?

There is a growing concern about inflation, and we are certainly seeing more inflation recently than we have seen in some years. Much of the recent rise is down to two big effects: we are measuring today’s prices against the depressed prices of the first lockdown (what is known as the base effect); and pent-up demand is hitting businesses which are not always able to cope, so they are putting up prices (what is known as friction). Both these impacts should naturally lessen over the coming year, with the result that inflationary expectations should remain ‘anchored’, that is consumers will not build inflation into their pay expectations and they will resist price rises in shops. Longer term there are concerns about the impact of the creation of vast amounts of money (not solely a UK problem) and many governments running staggering deficits. This is indeed a reasonable concern, but it is not one which has yet manifested itself in inflation.

James Sproule, UK Chief Economist