Inflation just keeps overshooting

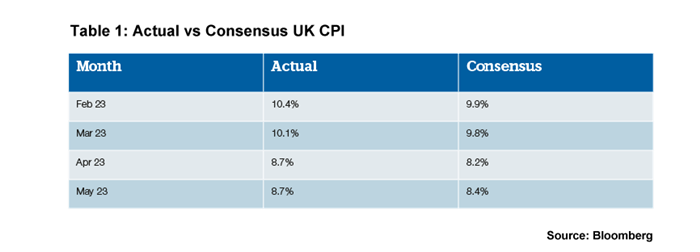

There was a febrile atmosphere in the run up to the Bank of England’s (BoE’s) interest rate decision in June. May’s CPI inflation print – which was published the day before – came in considerably above expectations with y-o-y headline CPI staying flat at 8.7%, despite predictions of a fall to 8.4%, and y-o-y core inflation continuing its advance in the wrong direction. This meant that the UK’s headline inflation rate had exceeded expectations for the fourth month in a row (see Table 1), leading to widespread concerns about the potentially entrenched nature of UK inflation.

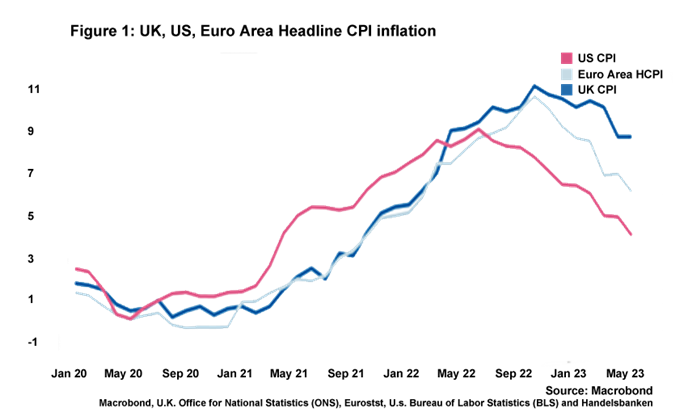

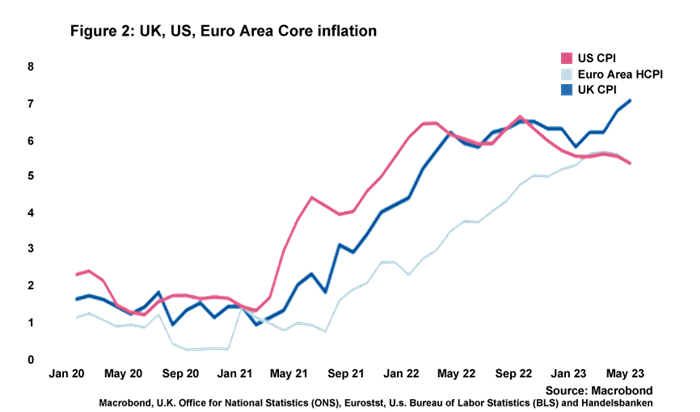

It has, of course, been widely noted that UK CPI, both the headline and core rates, sits considerably higher than CPI in the US and Euro Area (see Figures 1 and 2), so let’s take a moment to explore exactly what is going on here.

The UK is not the only developed country with inflation higher than the Euro Area (for example, Sweden’s headline rate is currently at 9.7% y-o-y) yet even so the discrepancy with the Euro Area and the US remains notable. The differential between the UK and the US is fairly easy to discern. US indigenous production of oil and gas meant that energy prices were relatively insulated from volatility in global energy markets, which helped moderate household gas and electricity prices as well as energy input prices for goods and services in the US.

The discrepancy with the Euro Area is more complicated, multi-faceted and not so clear cut. The nature of Ofgem’s price cap means that drops in energy prices somewhat lagged in the UK compared to the Euro Area. UK households will need to wait until July for electricity and gas prices to fall by 18% in absolute terms. But this does not seem to account for all of the difference between UK and Euro area inflation rates at the moment. The UK’s tight labour market – and the notable increase in labour inactivity rates since the onset of the pandemic – will no doubt also be playing a role, as this is a likely factor behind higher nominal wage growth in the UK versus the Eurozone. Other factors could also be playing an exacerbating role – for example, muted trade volumes in goods between the UK and EU and potentially a lagged inflationary impact arising from the depreciation in the pound during the autumn mini-Budget.

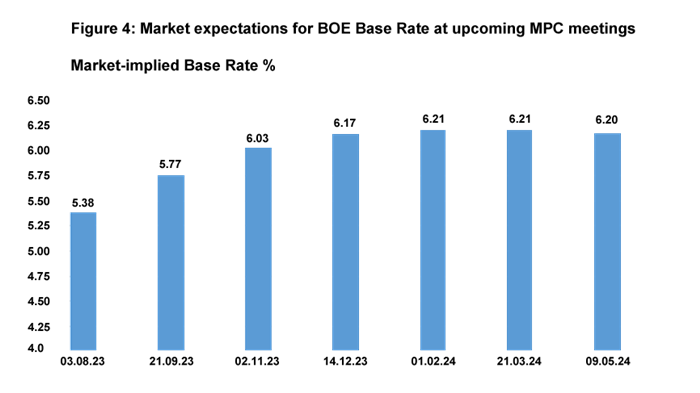

Despite inflation repeatedly overshooting expectations, markets were still predicting just a 25bp rate increase in June but the BoE’s hike of 50bp up to 5% (the thirteenth increase in this cycle!) shows just how seriously rate setters are taking the UK’s seemingly stubborn inflation. It now seems inevitable that further increases in rates will occur this year, with base rate potentially peaking at 6% by year end if market expectations are anything to go by. Whether this would mean a recession is on the cards is an open question: the impact on aggregate real household disposable income will be limited due to the structure of the UK mortgage market (although the pain will potentially be severe for those 1.3 million households that will be re-mortgaging over the next twelve months), but of course businesses whose loans are mostly floating rate will in aggregate feel the pinch much more speedily. What’s for sure is that the next set of labour market and inflation figures will be keenly watched by market participants to see just how high interest rates could end up going.