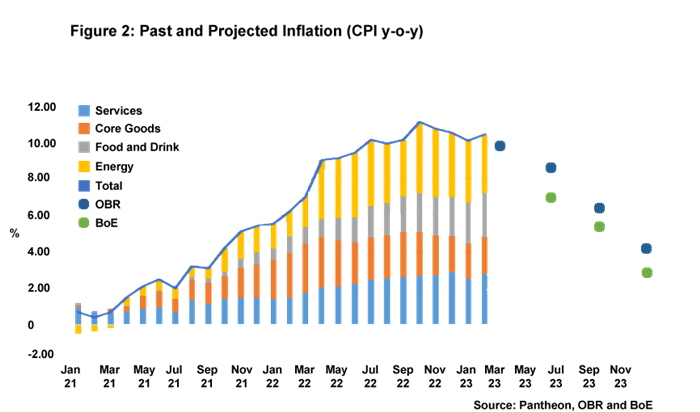

The Office for Budget Responsibility’s (OBR’s) March forecasts gave some welcome news to the Chancellor in the short term. The watchdog now predicts that inflation will drop faster than previously expected, with CPI expected to end the year just shy of 3%, while also forecasting that the UK will avoid a recession in 2023. This improved outlook gave Chancellor Hunt room to implement a series of tax and spending measures at the Budget which loosened fiscal policy by nearly 1% of GDP by 2024-25.

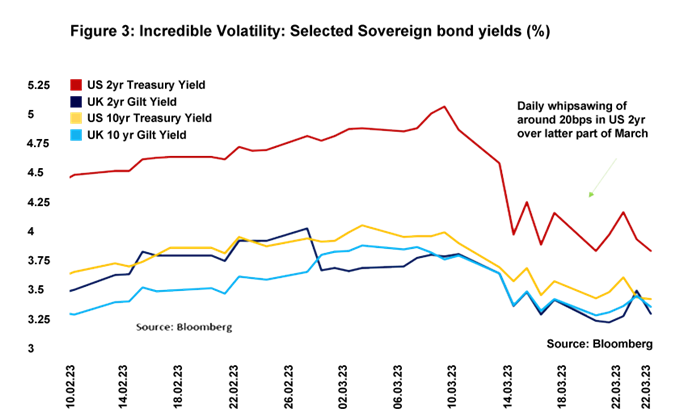

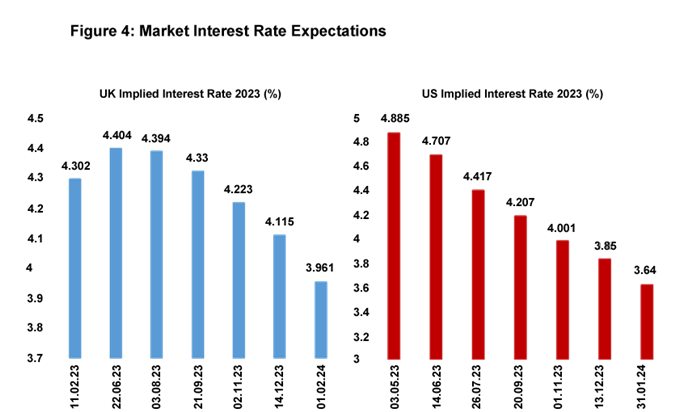

However, while the Budget would normally dominate the news bulletins, it was overshadowed by financial market turbulence arising from troubles faced by a number of regional US banks and Credit Suisse. This turbulence not only precipitated a major correction in equity markets, but also led to future interest rate expectations falling as concerns around financial stability rose up the agenda. Then, the day before the decision on UK interest rates, the inflation print threw another curveball into the mix. It showed, against expectations, both headline and core UK CPI rising, leading to concerns over whether inflation is sufficiently under control. This, of course, led to a difficult backdrop for the Monetary Policy Committee (MPC) who had to weigh up carefully both price and financial stability considerations.

The MPC decided to increase rates by 25bp up to 4.25% on a vote of seven to two, with the dissenters backing no change. Continuing tightness in the labour market and inflation surprising markets on the upside will have weighed on the minds of rate setters when making this decision. It is also notable that the MPC was briefed by the Bank of England’s (BoE’s) Financial Policy Committee that the UK banking system remains resilient: indeed, the UK banking system is now far better capitalised compared to the Global Financial Crisis and is subjected to stringent stress tests on a regular basis. This briefing will no doubt have offered reassurance to MPC members who may have otherwise been wavering in their decision.

Returning to the surprise on CPI, February’s unexpected jump in inflation is probably simply a blip. Various factors continue to weigh down on future expectations of inflation: spot and futures energy prices have dropped dramatically; world food prices have come off the boil since last year; shipping rates tumbled last year; and supply chain disruption has seen significant fall. These factors should help by year end to all but eliminate the three quarters of CPI inflation that is currently accounted for by energy, food and goods prices. Significant progress in reducing inflation should be seen in April’s figures when base effects start showing up strongly (that is, last year’s irregularly high figure due to the Ukraine invasion is the comparison point for this year’s numbers so the drop will look more remarkable) .

Services inflation, currently making up just over a quarter of CPI inflation, will be much stickier due to the influence that wage costs have in setting prices for that sector. The UK’s labour market remains tight, which will continue to put pressure on nominal wages, but the BoE’s latest analysis suggests wage growth will fall back faster than it was predicting in its February report.