War and inflation keep everyone guessing

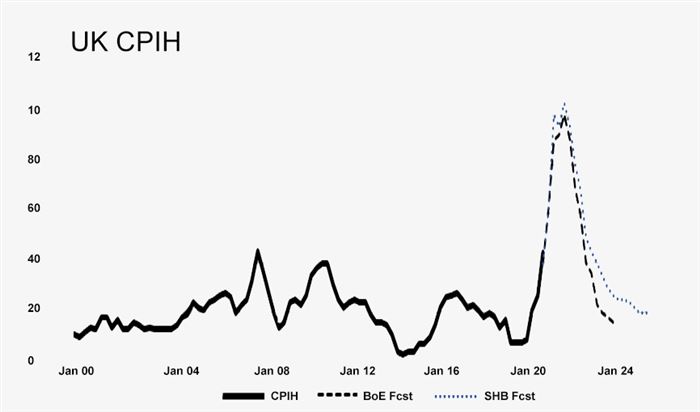

A year ago, the Bank of England’s forecast anticipated that inflation would be at around 2.5% at this point and fall back to its 2% target by the end of 2022. But a combination of tax increases, including the return of VAT rates to pre-pandemic norms, energy price hikes, and supply chain difficulties, dramatically altered expectations. We now expect inflation to peak at 10% percent in the fourth quarter of this year. Further increases in the cost of domestic energy are already set for October, the result of which means that we forecast inflation to only fall to 8% by year-end.

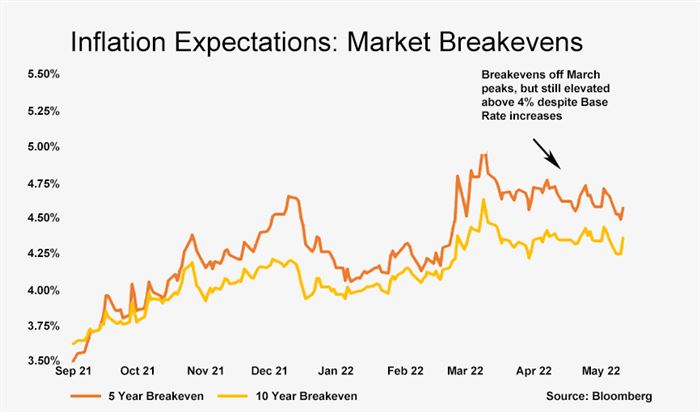

Looking beyond 2022, we see cause for caution about the prospects for inflation, but not cause for despondency – caution because core inflation is now registering at 5.7%. At the same time, much of UK inflation in 2022 will be tied to energy prices, and even if energy prices do not revert to levels seen in 2019, further dramatic rises are unlikely, and thus, due to the base effect alone, we should see inflationary pressure begin to subside in 2023. Moreover, wage increases, while high in nominal terms, are 1% below inflation, according to latest ONS figures. A tight labour market, evidenced by an unemployment rate of just 3.8%, is naturally contributing to wage pressure, but there should be some upcoming relief for the labour market, as around 500,000 workers who have remained inactive since the onset of the pandemic can be expected to re-enter it over the course of 2022. Overall, we expect unemployment to rise modestly in the coming two years, peaking at 5.5% towards the end of 2023.

Action on Inflation

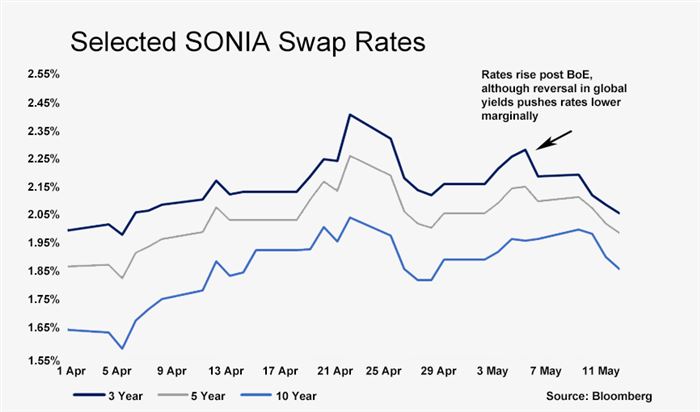

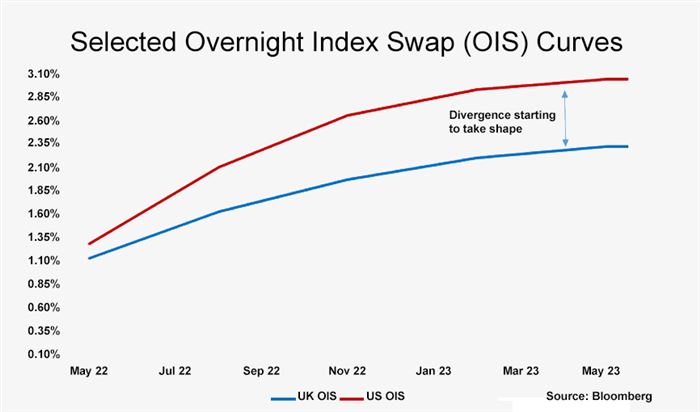

That said, the Bank of England clearly has to act, and financial markets now expect base interest rates to be above 2% within the next year. This would put interest rates close to what is thought by academics to be their “neutral” level, a rate that is sufficiently high to counter inflation, but not so low as to encourage asset bubbles or mal-investment. While such a move would meet the Bank of England’s mandate to counter inflation, we believe such a rapid move to these levels would likely trigger a recession. Therefore, we forecast that the Bank of England will be more cautious and raise rates to 1.5% in two more 25bp steps in August and December. Thereafter, maintaining interest rates at that level would be consistent with a ‘soft landing’.

Raising interest rates to a level below ‘neutral’ does not mean there will not be a further tightening of monetary policy, and our forecast is that the Bank of England’s preferred path will be to cautiously continue with Quantitative Tightening (QT). This will be achieved primarily by not reinvesting the proceeds of the Asset Purchase Programme (APP) stock of debt as it matures (a process already started in March, as interest rates rose above 0.5%). Simply not reinvesting the proceeds of the APP gilts as they mature would result in a reduction of 20 percent of the APP stock of holdings by mid-2025 and 50% by 2030, although the final holdings would not mature until 2070. If necessary, the Bank of England has indicated it may speed up the process by additional targeted sales of its stock of assets (active QT), now that interest rates are above 1%. Given the limited global experience with any form of QT, let alone active QT, the Bank of England will no doubt be proceeding cautiously.

James Sproule, Chief Economist