BoE left with a tricky balancing act

The Bank of England (BoE) is now painting a comparatively sanguine picture for short-term economic growth prospects in the UK. Stronger than expected global growth, lower energy prices and new fiscal measures at the Spring Budget have led the central bank to move from predicting a protracted recession just three months ago to now expecting the UK economy effectively to flatline this year. It is also notable that the IMF has recently upgraded its UK 2023 growth forecast from negative into positive territory.

These upgrades are no doubt encouraging and based on robust assumptions, but it is important to note that these growth forecasts remain subdued by historical standards. And, of course, downside risks to the outlook remain, both from geopolitical developments and other factors affecting financial markets. The BoE is currently of the view that recent global banking sector developments will only have a small impact on GDP, yet signs of tightening credit conditions in the United States will need to be monitored carefully over the coming months given the potential impact on the global economy.

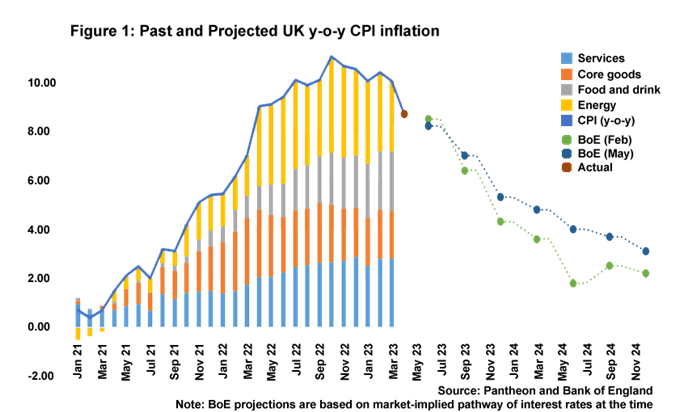

While the growth outlook has improved for the UK economy, the same cannot be said for the inflation outlook. The BoE is clear: inflation is now expected to be higher for longer. CPI y-o-y inflation is expected to end the year at just over 5%, rather than just over 4%, and from this point onwards prices are expected to be sticky and not reach the 2% target by the end of 2024 (see Figure 1).

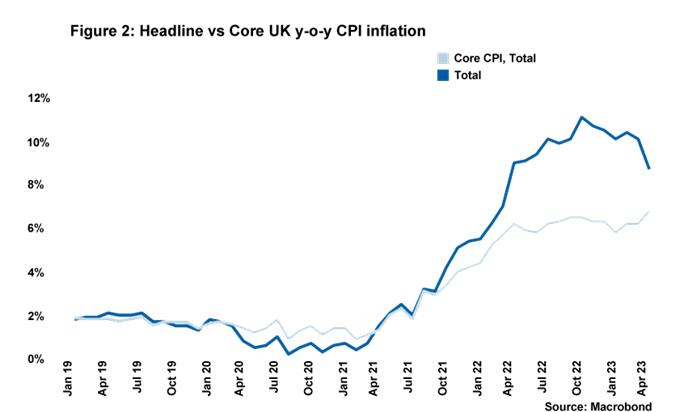

We have now, of course, had April’s y-o-y CPI figure which showed a drop from 10.1% to 8.7%. The drop in headline rate is accounted for by base effects in the electricity and gas component of inflation (see here Opens in a new window for further details) and, rather worryingly, the print was substantially higher than market expectations of 8.2%. It is especially concerning that the core rate of inflation (which excludes energy and food,) saw a significant increase from 6.2% to 6.8% and reinforces our view that prices in the services sector, which are highly influenced by wage costs, are likely to be stubborn.

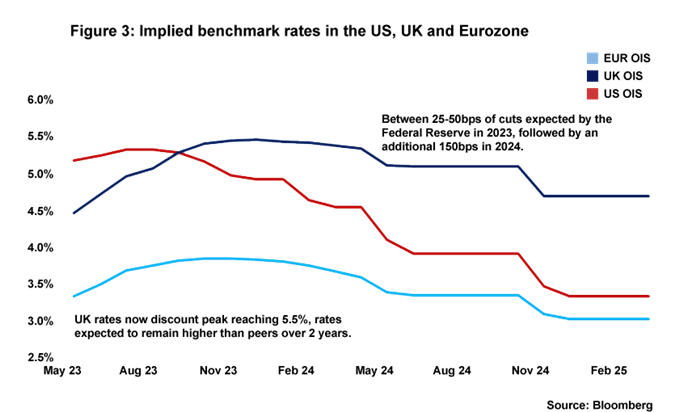

Inflation has now run hotter than expected for three consecutive months and this obviously has implications for the pathway that interest rates will follow. As of the time of writing (26 May), markets are now expecting a further 100bp of interest rate increases this year, which would take rates up to 5.5%. There will be inevitable pressure on the BoE to continue its rate hiking cycle, but it will be a difficult balancing act for rate setters given that much of the impact of previous rate rises is still due to transmit into the economy – especially as well over 80% of UK mortgages are fixed-rate. The BoE is currently conducting further work on the monetary policy transmission mechanism and is expected to publish its findings over the next year.

A 25bp increase in June is now a near certainty, although there is considerable uncertainty about where exactly rates will peak in this cycle.

Daniel Mahoney, UK Economist