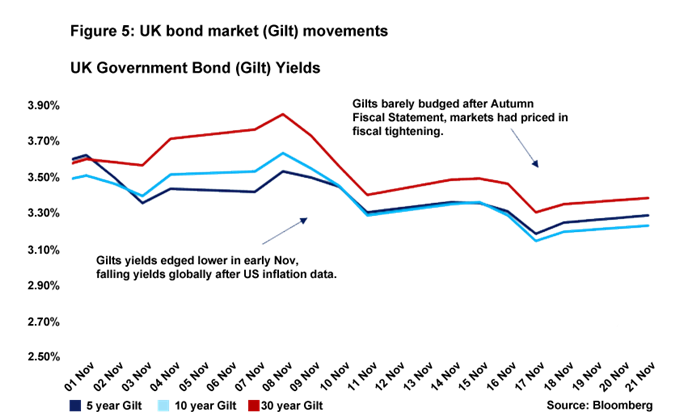

After the turbulence following the so-called “mini-Budget” in September and the subsequent downfall of the former Prime Minister Liz Truss, the reaction of financial markets to the Autumn Statement on 17 November will have been at the forefront of government ministers’ minds. The government will have felt a sense of relief on this front: market expectations for interest rates and yields on gilts barely moved following the statement. But while achieving short-term financial market stability was a critically important objective, the overall package of measures remains controversial. The £55bn of fiscal tightening has been announced just as the economy is moving into recession.

This fiscal consolidation is somewhat different to that pursued in the early 2010s. The scale of the tightening is not as large and the composition is different with tax rises doing more of the tightening this time around. And of the spending restraint that was announced, a large chunk has been postponed until after the next general election – for example, lowering the growth of departmental spending across Whitehall will only start to kick- in from 2025-26.

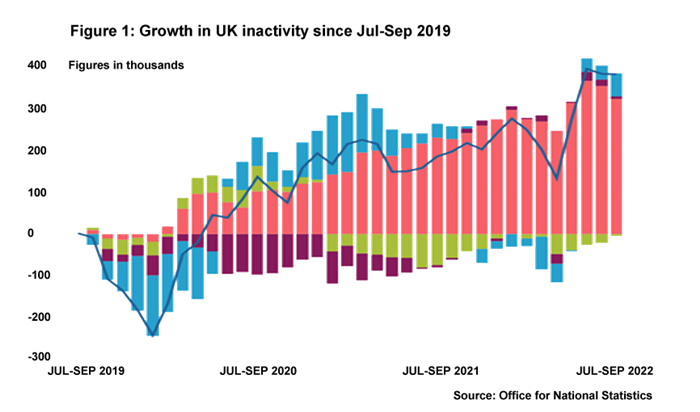

The economic backdrop to this Budget was gloomy, with the UK facing the dual problem of high inflation and a slowing economy. In the UK, multiple indicators were already flashing red with consumer confidence registering at record lows and business PMIs indicating contraction of both the services and manufacturing sectors. You would see a similar picture in many other Western economies although the UK faces its own unique challenges, not least with its labour market. The growth in inactivity rates is an especially concerning problem given that this has been observed much more strongly in the UK compared to many of its G7 counterparts. The UK has also, of course, suffered from a slowdown in trade due to bureaucratic burdens associated with Brexit.

While some of the constraint on spending has been deferred, the fiscal statement imposes some short-term measures that will affect consumer spending during the impending downturn. Alongside tax policies that will eat into pay packets – such as the freezing of various tax thresholds – the government is committed to a much less generous energy price guarantee from April 2023, with a the energy cap due to be lifted by 20% along with the removal of £400 support for households. This could mean that the UK ends up facing a deeper recession than many of its counterparts: it is notable that other major western economies are yet to announce a withdrawal of energy price support so soon.

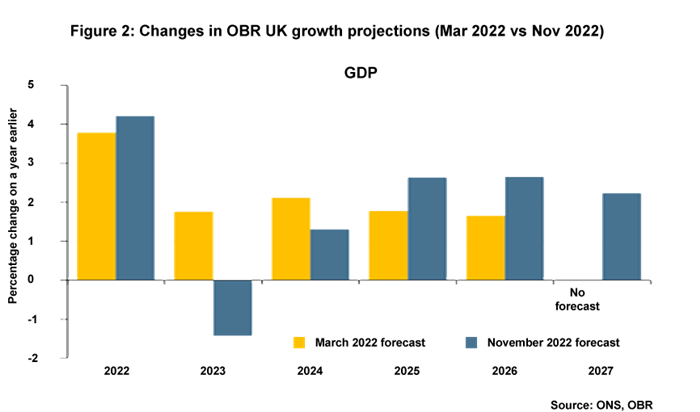

Without the benefit of a positive external shock – for example, a cessation of the war in Ukraine – the UK economy is in for a difficult twelve to eighteen months. Some of the projections from the Office for Budget Responsibility are really quite striking. For example, real household disposable income is due to fall 4.3% in 2022-23, which would be the biggest drop on record.

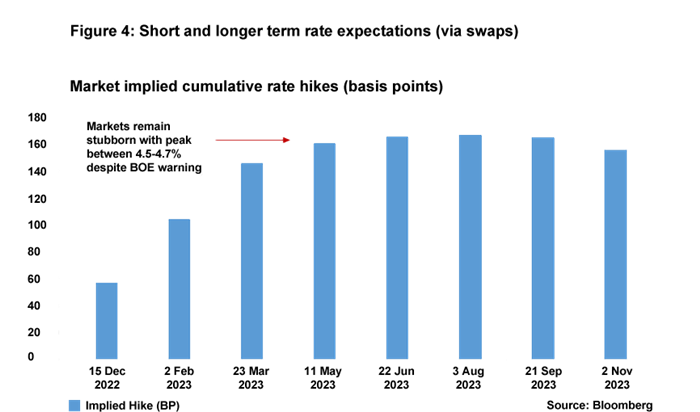

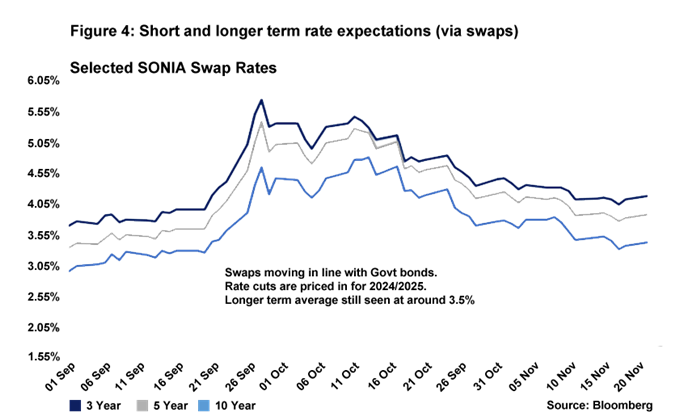

The Bank of England now has a tricky balancing act between suppressing any signs of domestically-led inflationary pressures and ensuring that the downturn is not unnecessarily protracted, while also of course being on guard for any financial stability risks that could come about from the upcoming correction in the property market. At the time of writing, market expectations are for interest rates to peak at around 4.5%; we remain of the view that rates will peak somewhat below this at around 4% as the Bank of England weighs up all of the considerations.

Daniel Mahoney, UK Economist