Autumn Statement won’t materially affect interest rate decisions

At its November meeting, the Bank of England’s (BoE) Monetary Policy Committee (MPC) decided to hold rates at 5.25% although the decision was split six to three. The three dissenting members backed an increase in rates by 25bps but the other six members voted for a freeze. The majority cited two key reasons for their decision: first, that the labour market has seen sufficient loosening and second, that the acceleration in the Office for National Statistics’ average weekly earnings is not being reflected in a broader range of wage growth measures. As we have highlighted before, private sector wage growth is one of the key metrics the MPC is currently tracking. While the ONS’s measure of private sector pay for September is running at an uncomfortably high 7.8%, other measures such as the PAYE data and the Indeed wage tracker suggest that nominal pay levels are somewhat lower.

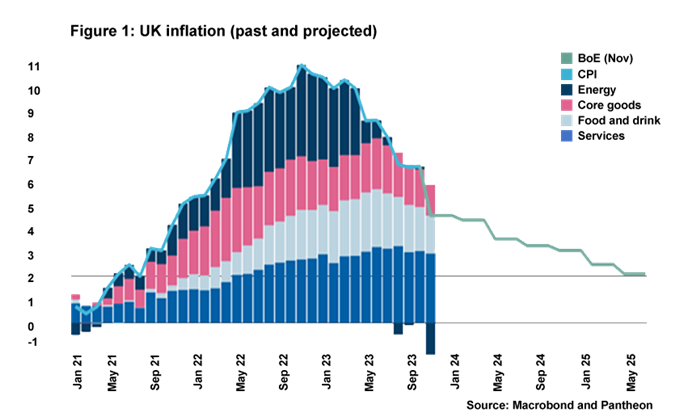

Since the November MPC meeting, nothing has happened to materially increase the likelihood of the Bank of England hiking again in this cycle. Indeed, the CPI inflation print for October will have been particularly reassuring to MPC members. The headline y-o-y rate fell to well below 5% (6.7% in September to 4.6% in October) and the core rate also saw some easing. Services inflation, another metric being tracked closely by the MPC, cooling from 6.9% to 6.6% will be especially reassuring for those MPC members remaining concerned about domestically-led inflationary pressures. Of course, the situation in the Middle East does present an upside risk to the inflation outlook but, for now at least, the conflict appears to be contained and the reaction from energy markets has been fairly muted.

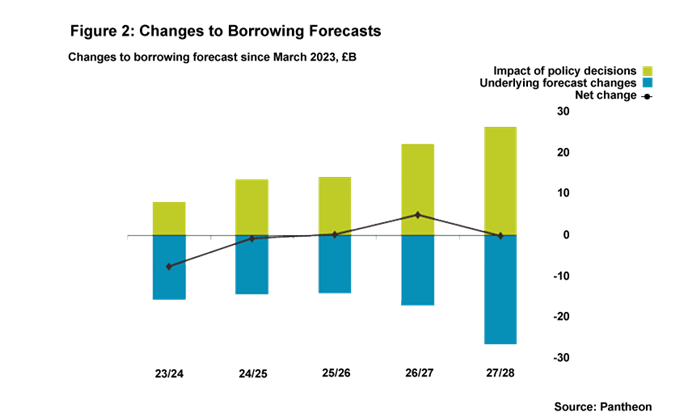

Changes to fiscal policy do, of course, have the potential to alter the pathway of monetary policy. All other things equal, a loosening of fiscal policy could prompt a tightening of monetary policy. At the Autumn Statement, Chancellor Jeremy Hunt loosened the purse strings to the effect of £21bn per year by 2027-28, announcing measures on the eve of a general election including a cut of 2 percentage points in employee National Insurance contributions and the introduction of permanent full expensing for businesses. However, market expectations for interest rates moved only very slightly following the Autumn Statement due to the loosening of fiscal policy coinciding with an improved fiscal outlook (in fact, there seemed to be at least as much movement in financial markets arising from the Business PMI (Purchasing Managers Index) numbers published the following day). UK public finances will benefit from the impact of inflation and fiscal drag moving more people into higher rate tax bands, and the growth in tax receipts arising from this will more than offset higher debt interest payments arising from the growth in interest rate expectations since the Office for Budget Responsibility’s March outlook.

Table 1: Impact of policy announcements at the Autumn Statement*

|

-

|

23-24

|

24-25

|

25-26

|

26-27

|

27-28

|

28-29

|

|

Policy decisions

|

-6.7

|

-14.2

|

-12.4

|

-18.1

|

-21.0

|

-21.1

|

|

Spending decisions

|

-4.8

|

-2.9

|

-2.7

|

-1.9

|

-1.2

|

-0.8

|

|

Tax decisions

|

-1.9

|

-11.4

|

-9.8

|

-16.2

|

-19.8

|

-20.3

|

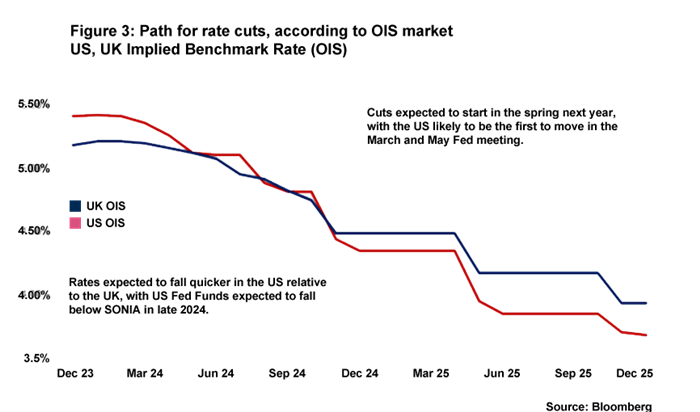

At the time of writing, financial markets are pricing in a mere 4% chance of a rate hike at the December meeting and a less than one in five chance that there will be another increase in this cycle at all. While another increase in rates is unlikely, monetary policy continues to be slowly tightened through the process of QT and if statements by the BoE are anything to go by, rates are likely to be held at 5.25% well into next year. In its latest inflation outlook, the BoE states that "monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term" and that "second-round effects in domestic prices and wages are expected to take longer to unwind than they did to emerge".

Significant progress has been made in the fight against inflation, but the road to 2% inflation remains a serious challenge. Interest rates are likely to remain at levels restrictive for economic growth for quite some time. At this stage, we do not expect base rate to start falling until around summer 2024.

Daniel Mahoney, UK Economist