No need to panic yet

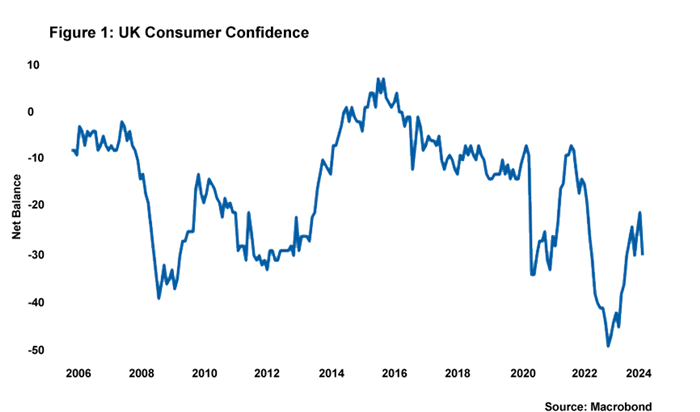

The outbreak of war in the Middle East (aside from the distressing human costs) will lead many to question what will be the impact economically both here in the UK and globally. Evidence suggests that UK consumers are expressing some concerns with respect to this: consumer confidence took an unexpected tumble in October, falling to -30 compared to market expectations of an increase to -20. Yet it would be ill-advised to read too much into this until it becomes clearer as to how the geopolitical situation develops in the Middle East.

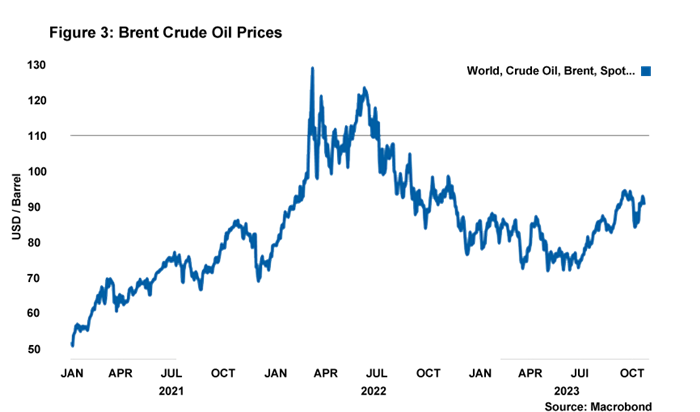

Initially, one of the key channels whereby the conflict could affect the UK economy would be via the energy market. There certainly have been some moves in global oil and European gas markets since Hamas’s attack on Israel. At the time of writing, UK gas spot prices are up 27% and global oil prices are sitting at roughly $90 a barrel. Context is important, however. UK gas spot prices remain well below levels reached in 2022, currently more than four times less than the previous peak. And, as discussed in the previous rate wrap, in the event that global oil prices continue on their upward trajectory, it is very unlikely that the impact would be anything like that which occurred from gas price spikes following Russia’s invasion of Ukraine. A $110 oil price would only increase UK inflation by 0.5pp at peak impact, according to Bloomberg’s SHOK model.

For now, providing there is not a significant escalation of the Middle East conflict, the UK economic outlook seems to be much the same as it was at the time of the last wrap, with growth set to be sluggish in the short term. The UK’s PMI composite index for October registered at 48.6 for October. This, of course, indicates that the private sector is contracting given the figure is below 50 but it is hardly a catastrophe. The figure would imply that quarterly growth will decline by just 0.1%.

Things could be a lot worse. It is striking just how much help the UK economy has received from a better than expected energy market. We estimate over the course of 12 months from July 2023 that the observed and expected pathway of household energy bills compared to a cap of £2,500 for typical use will in aggregate inject nearly £15bn into consumers’ pockets.

Moreover, there was some good news in the latest PMI release on the inflation front, with evidence of significant easing of cost pressures for businesses. And there will undoubtedly be further good news when October’s inflation print is published next month. UK CPI y-o-y inflation is expected to drop like a stone, down from September’s print of 6.7% to a level below 5%, bringing it more into line with European counterparts and no doubt helping improve people’s perception of the UK economy. This fall will be driven mostly by the base effect in energy prices (discussed in previous rate wraps), but we should also see both food and goods inflation easing in October’s y-o-y print.

Has anything changed with respect to interest rate expectations? Not especially. Cost pressures are easing, inflation is still set to fall below 5% and labour market indicators continue to somewhat loosen. While wage growth remains above what the MPC will be comfortable with (7.8% without bonuses, according to the ONS’s key measure), more timely PAYE data suggests pay awards are easing. This should be enough to stop the MPC from raising rates at the November meeting. Indeed, markets now think it is very unlikely that we will see a further increase in rates at the November meeting, and now believe there is more than a 50% chance that a 5.25% base rate is the peak for this cycle. This is a view that we share.

Daniel Mahoney, UK Economist