March’s inflation print is one of the first bits of hard data to highlight the UK macro impact of the Iran war. Y-o-y UK CPI rose from 3% in February to 3.3% in March, and inflation is now on course to peak at around 4% later this year. This is, of course, in marked contrast to the Bank of England’s February forecast of inflation falling to near target level in April and then staying at around 2% for the remainder of the year.

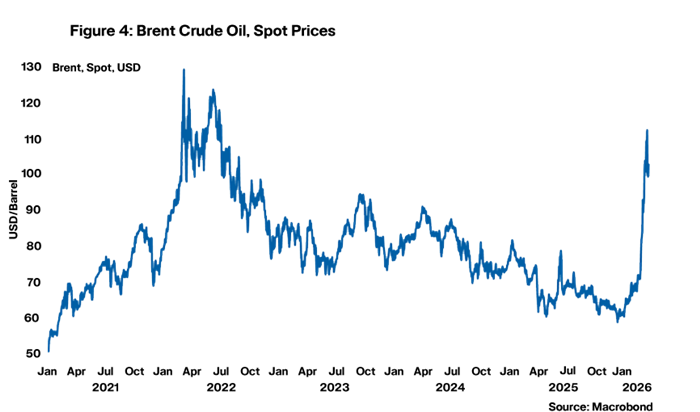

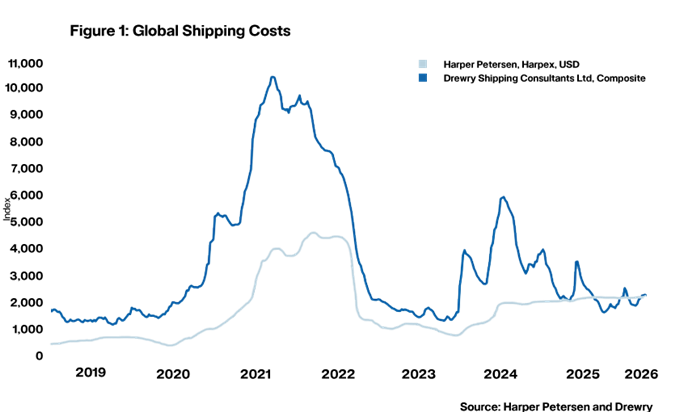

A large degree of uncertainty remains about how severe the energy price shock from the Iran War will be, although we know for sure that there will be an impact, as multiple energy infrastructure sites in the Middle East have been destroyed or damaged. But it is important to stress once again that there’s unlikely to be a repeat of what happened in 2022 when Russia invaded Ukraine. Monetary policy was loose in the run up to the invasion, whereas we come into this energy price shock with interest rates at levels that are likely to be restrictive to economic activity. Moreover, the broad-based supply disruptions arising from Covid are not present this time around (see, for example, what happened with shipping costs in Figure 1 below).

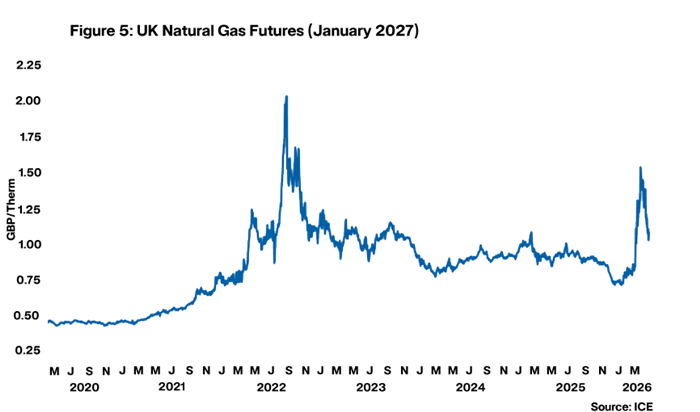

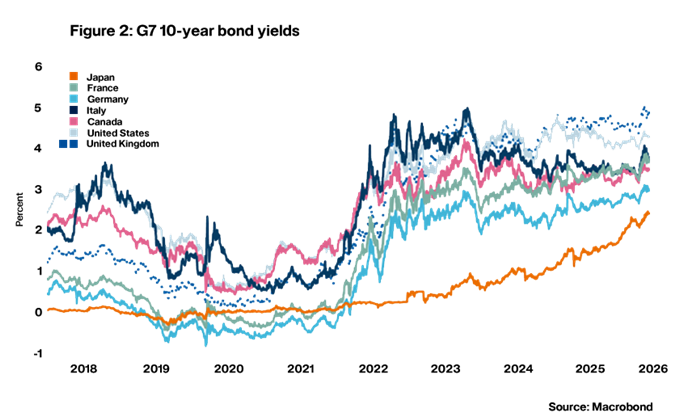

However, there is no doubt that the current crisis has exposed some of the UK’s structural vulnerabilities. For example, compared to other developed economies the UK is very reliant on gas for its energy mix, and of course a large amount of this is imported. And at various points over the past couple of months, the gilt market has seen higher levels of volatility compared to other G7 debt markets. A big reason for this is that the UK’s gilt market is disproportionately reliant on overseas investors who are typically more mobile than, say, domestic pension fund investors. This is, of course, not to mention that yields on gilts have for some time now been notably higher than those of G7 counterparts (see Figure 2), in no small part due to perceived inflation risks in the UK.

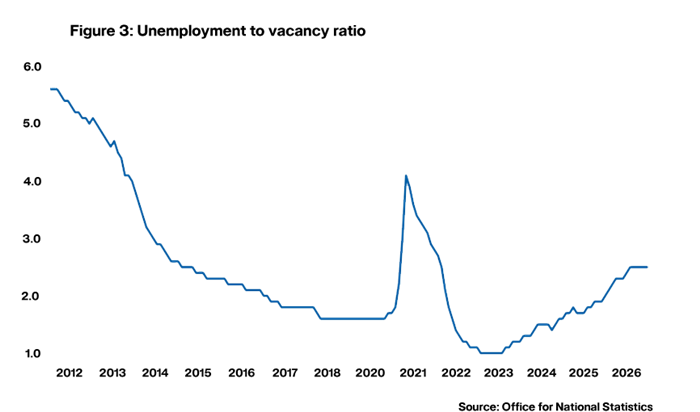

Looking ahead, how will the Bank of England react to the upcoming increase in short-term inflation? As highlighted in the previous Rate Wrap, the jump up in consumer inflation expectations will clearly be a concern, especially since the public is now more attentive to inflation. Apart from a brief period in 2024, the UK has not met its inflation target for nearly five years now. However, as the labour market has somewhat loosened over the past two years or so (see Figure 3), consumers may not be in a position to demand large increases in wages in the way they did following the 2022 inflation spike. This could help quash any unwelcome wage-price dynamics playing out.

Nonetheless, our base case view is that the Bank of England will need to respond to the risk of second-round effects from the short-term inflation spike, potentially leading to one rate hike this year, a change from the pre-Iran war prediction of two rate cuts. But there is a huge level of uncertainty. If the geopolitical situation sees a rapid de-escalation, it is plausible that we end up seeing a couple of rate cuts later this year whereas in an escalatory scenario we could see several rate hikes. The situation will almost certainly be clearer by the time of the next Rate Wrap, although more column inches may end up being dedicated to UK political risk given current instability in the government and the upcoming May local elections.

Daniel Mahoney, UK Economist