The rates market had a lot to digest this December before winding down for the Christmas holidays, not only did we have key data health checks in both the UK and US (data from the latter resuming after the government shutdown), but also central bank meetings from both the Bank of England and Federal Reserve. Whilst there have not been any major shifts in swap rates across the curve this month, we have a few interesting talking points to take into 2026.

BoE decide on a cautious cut

As expected, with 98% probability before the decision, the Monetary Policy Committee voted to reduce bank rate from 4.00% to 3.75%. Debate emerged beforehand on whether five or six members would vote for a cut, especially after the miss in inflation the day before which saw annual headline inflation drop unexpectedly from 3.6% to 3.2%. In the end it was a close call, a 5-4 split in favour of cutting rates – meaning Governor Andrew Bailey was the deciding voter.

Markets, and ourselves, expected Mr Bailey to favour a cut this time around, as it seemed a close call in the November meeting. Since then, data has arguably been on the weaker side – note the above inflation print, monthly falls in payrolls and consecutive monthly declines in GDP across September and October. The rates market however has interpreted the decision as a ‘hawkish cut’, noting changes in the language including a comment that future decisions will be a “closer call”, as well as remarks from Mr Bailey himself stating that whilst he sees scope for rates coming down further, bank rate is not on a pre-set path and he acknowledges there is “limited space” to cut the rate before it reaches neutral territory.

Overall, caution remains surrounding the outlook for wages and inflation, and while highlighting a benign/weaker labour market, the statement suggests the committee needs more convincing evidence of a genuine slowdown.

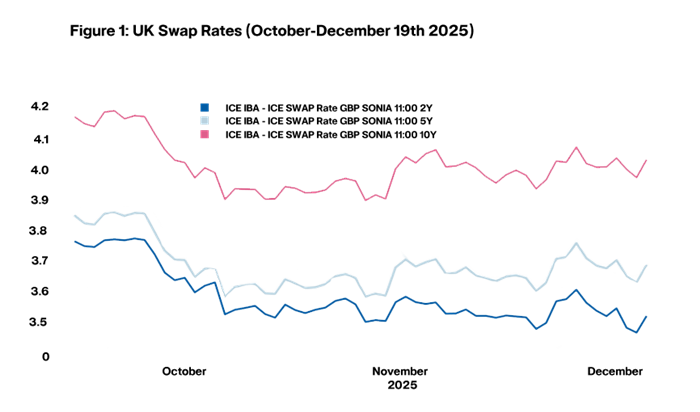

Looking into 2026, reaction in the short end of the swap market was rather minimal, pricing still suggests at least one more cut (at the April meeting) but the outlook thereafter is clouded even further. Markets are now a touch less convinced on a further cut later in 2026 - currently price in a 50% chance of a further cut in the autumn.

An upward shift in longer-term rates has also been observed, but only to the highs of recent ranges and remains off the early October highs. A 5-year interbank swap rate around c 3.65% evidences that markets feel a bottom in rates is approaching, and debate grows as to whether the pre-budget levels in longer end swap rates seen in November will mark the cycle low.

Hawkish impulses all around

Upward pressure on yields globally has been a theme in December, as many central banks reach the end of their rate cutting cycle, and focus turns to the timeframe for an interest rate hike. This has been a hot topic for the Eurozone, ignited by ECB board member Isabel Schnabel who said that she sees the next ECB move being a hike (albeit not for a while), which was a catalyst for a selloff in yields across developed nations earlier in the month. Ms Schnabel’s comments, coupled with better data and rosier GDP forecasts led to markets briefly pricing in a chance of a hike late in 2026. These calls were tamed by President Lagarde at the December ECB meeting, who noted risks to the economic outlook, whilst also reiterating the importance of optionality. Markets do however see no more cuts from officials in Frankfurt.

The hawkish impulses extend beyond the ECB though, the Bank of Japan increased rates by 0.25% to a three decade high of 0.75% - with more to come, whilst rate cutting cycles have been completed in Sweden, Switzerland, Canada and New Zealand. In Australia, the rate cutting cycle has seemingly ended prematurely, with a strong chance of a hike before the summer of 2026.

The Fed’s strange position

It is hard for us and the market to interpret US data and Federal Reserve commentary currently, mainly because question marks remain on the quality of data post-shutdown, and markets cannot ignore the possible shift in dynamics at the Fed next year when Jay Powell is replaced as chair.

The (lack of) market reaction to November’s CPI print is evidence of caution in interpreting the official data being released, with annual headline and core inflation dropping considerably to 2.7% and 2.6% respectively – way below consensus. The BLS could not collect data for October due to the shutdown, and some note this may have impacted the November figures too, given the data was collected later in the month.

The Federal Reserve (also facing the difficulty of data quality) decided to follow October’s cut with another reduction in December, as expected, taking the lower bound to 3.5%. Like the BoE, there seems to be a growing divide within the committee with two voting to keep rates on hold. The Fed’s median estimate points to one more cut next year, whilst markets currently see two more quarter point cuts. There is an acknowledgement of a weaker jobs market, as evidenced in the most recent jobs report, but GDP growth for Q4 was revised upwards. The Fed also announced purchases of Treasuries of up to $40bn a month in order to support liquidity and keep reserves ample, with commentators suggesting this isn’t far from restarting QE.

For now, markets may have reservations about the current stance of the Fed with the view that Chair Jay Powell will be replaced by a more dovish leaning chairman, with the nailed on favourite being Kevin Hassett. Concerns around the politicisation of the Fed have been in the media for a while, and whether that means a more aggressive cutting cycle in the latter half of next year. It’s all speculation, but markets are likely placing slightly less weight on current signals from the Fed with the makeup shifting next year.

Lastly, from everyone on the Rate Wrap team, we wish you all a very Happy New Year!

Cameron Willard, Capital Markets