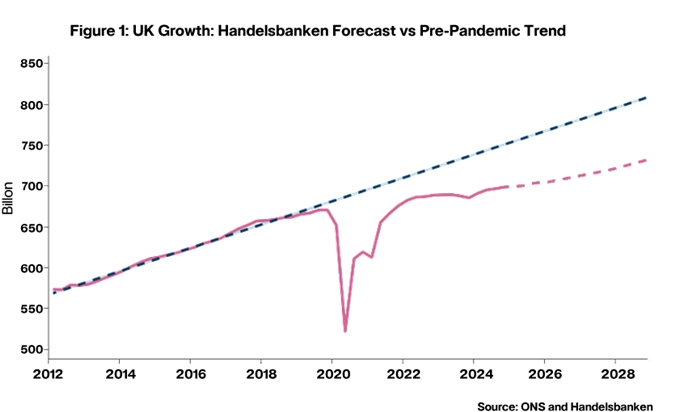

We kicked off the year at Handelsbanken with the publication of our latest Global Macro Forecast Opens in a new window. From a global perspective, there are some cautious signs of optimism that there could be steadier growth in 2026, although the UK macro outlook is one of fairly subdued growth over the next three years. There are some potential tailwinds to UK growth, including a possible fall in the household savings rate, improved relations with the European Union, and planning reforms. However, various structural problems such as high industrial electricity prices and issues with the UK labour market are likely to stymie growth. It is also notable that UK political risk is rising up the agenda with the governing Labour Party facing a tough by election later this month and a challenging set of local elections in May.

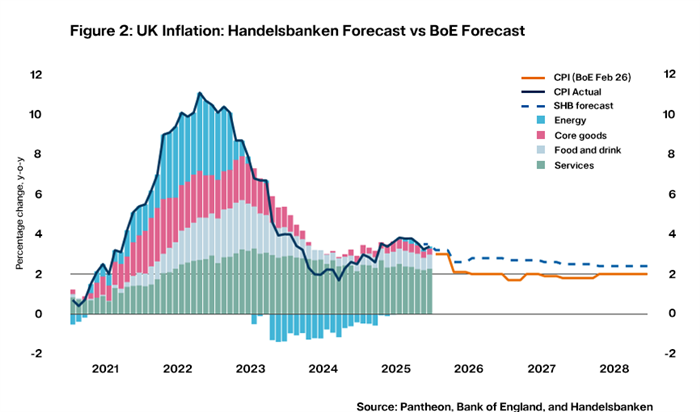

Our forecast is for inflation to be more stubborn than the Bank of England’s latest forecast currently predicts. We will see inflation drop dramatically from its current level of 3.4% down to near the Bank of England’s target in April, in large part due to the government moving levies on energy bills onto taxpayers. Yet services inflation and wage growth remain above levels compatible with the Bank of England’s target and headline inflation is likely to rise again by year end. We have talked in previous Rate Wraps about the risks around high consumer inflation expectations in the UK, but it is also worth bearing in mind that the UK’s inflation rate has historically been notably higher than the Eurozone’s by around 0.75pp since 2005. This trend could be due to the fact that the UK economy is more services-orientated than the Eurozone’s, which in turn means that it can take longer for headline rates of inflation to fall. Taking all of this into consideration, we have pencilled in two further rate cuts this year – which is broadly aligned with market expectations, but the inflation persistence concern means we currently do not envisage any further interest rate cuts in the forecast period to 2028.

Pivoting onto a global macro issue, we have a theme article in the Global Macro Forecast which looks at the potential longer-term economic impact arising from trends in artificial intelligence (AI). So let’s briefly reflect on our thinking about how AI affects the longer-term macro outlook.

We start by examining the adoption of AI by commerce. Adoption seems to be happening at a faster pace in the United States compared to Europe, but it still remains in its infancy across the western world. For example, just 7% of businesses using AI in the US have fully deployed it across their organisations, and it is notable that there are multiple barriers to adoption that continue to slow the rate of growth in AI use by commerce. Data centres are enormously energy-intensive — which of course puts Europe and the UK at a particular disadvantage given their industrial electricity costs are 2–4x those of the United States, and there are numerous barriers within firms that slow down adoption of AI, not least the issue of fragmented databases across organisations.

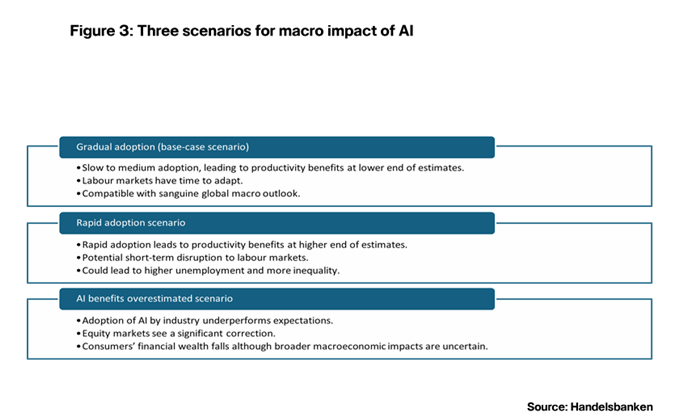

This leads us to a base case view of “gradual adoption” of AI. Our colleagues in Stockholm estimate that this could still increase productivity growth by 0.7pp per year on an annual basis over a ten-year period in Sweden. The benefits could even be slightly higher in the UK given the economy is especially strong in sectors that are AI-exposed. This is not quite the sort of productivity gains we saw in the IT revolution during the 2000s, but it would still alone be larger than the productivity increases we’ve seen in the UK since the Global Financial Crisis. And the base case scenario has two key further advantages. First, gradual adoption of AI would potentially allow labour markets to adapt and promote a trend of the technology complementing labour rather than replacing it and second, our view is that it would not necessarily lead to an equity market correction.

We do, however, flag two very plausible alternative scenarios. The first is a more rapid adoption of AI, which leads to truly transformational impacts on growth prospects of economies but would have the key short-term disadvantage of likely prompting major labour market dislocation, higher unemployment and higher inequality. The second is a scenario where AI is not adopted by commerce at scale and the productivity benefits fall short of expectations, which would of course point to an equity market correction. So, while the base case scenario is compatible with a sanguine outlook, there remains a huge deal of uncertainty as to the macro impact of AI.

Daniel Mahoney, UK Economist