So the seemingly inevitable has now happened. Following Andy Burnham’s convincing win at the Makerfield by-election, Sir Keir Starmer has announced a timetable for his exit as prime minster and leader of the Labour Party, and it is now increasingly likely that the former Greater Manchester Mayor is set to become the UK’s next prime minister. The financial market reaction to the latest news has been sanguine, as the additional risk premium associated with a change in Number 10 Downing Street has already been priced into UK government bonds, not least due to some outsized movements in gilt yields following the local elections.

Burnham has committed himself to the government’s current fiscal rules and is set to have heavyweight economic advisors including former Conservative minister Sir Jim O’Neil and Andy Haldane, former chief economist of the Bank of England, which will no doubt somewhat reassure markets, but they will reserve their final judgement until the next budget takes place, likely in autumn.

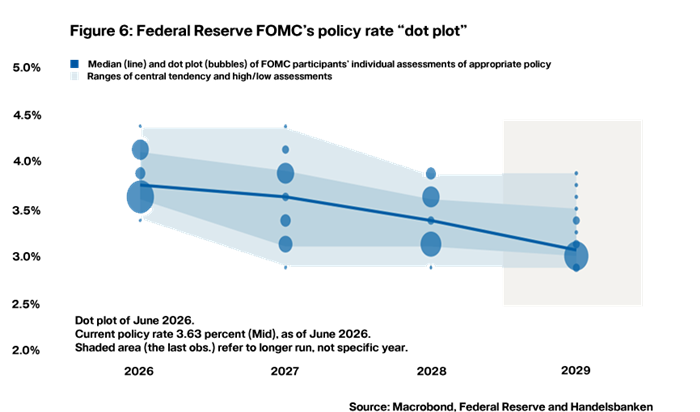

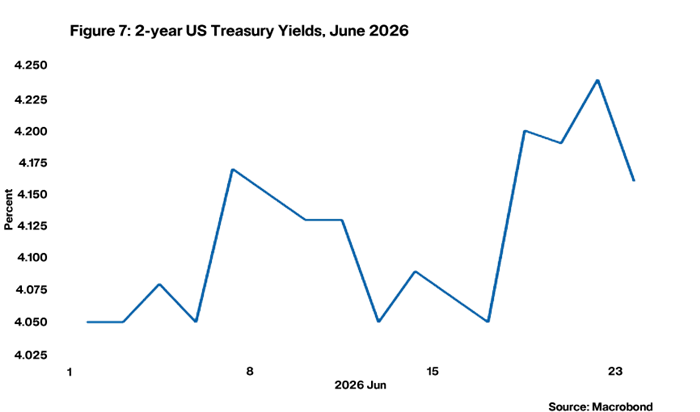

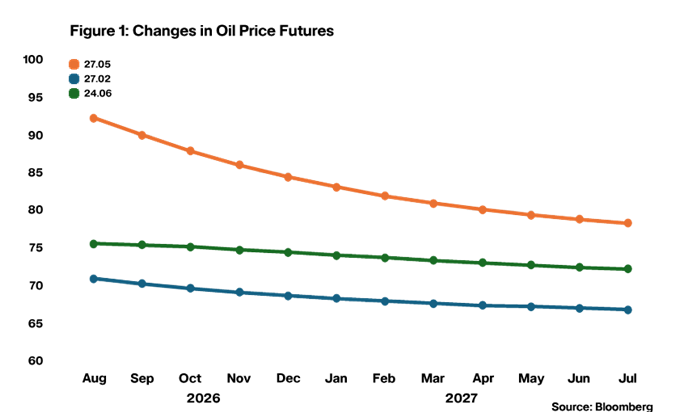

Elsewhere, it is important to emphasise, once again, that geopolitical developments in the Middle East have been the key driver of negative movements in UK financial markets. The news on this front from a macro perspective has been much more positive recently, with oil price futures dropping markedly on news of the provisional agreement between the US and Iran. Oil prices now sit only marginally higher across the curve compared to the situation pre-Iran war, a significant improvement from just a few weeks ago. The domestic data rolling in on inflation has also been better than expected, the backdrop of which has allowed the Bank of England to continue its “wait and see approach” by holding base rate at the current level of 3.75% in June.

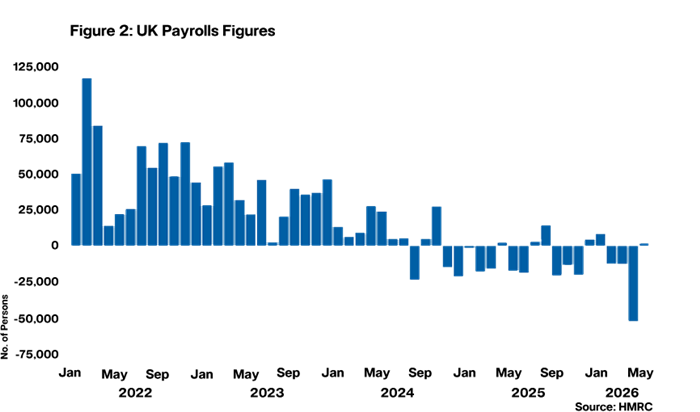

The vote was 7–2 in favour of holding rates, with MPC members Huw Pill and Megan Greene dissenting with a vote to increase interest rates. The majority advocating the “wait and see” approach emphasises the reduced upside inflation risks from geopolitical developments as well as signs that the labour market is loosening: it is notable that April’s revised payrolls figure came in at a surprisingly bad -52,000. The two hawks on the MPC worry about the increase in inflation expectations, especially among consumers, and cite evidence that it’s important to be more attentive on this front given the UK has recently experienced high levels of inflation.

So, what next? Of course, future developments in both the geopolitical and domestic political space have the potential to upset the apple cart. However, our base case view set out in May’s Global Macro Forecast Opens in a new window, which assumed a gradual re-opening of the Strait of Hormuz, is still on track. This implies that the base rate will be held for the rest of this year, but bear in mind that this would still be a response from the Bank of England to the energy price shock: prior to the Iran war, we were expecting two rate cuts in this calendar year.

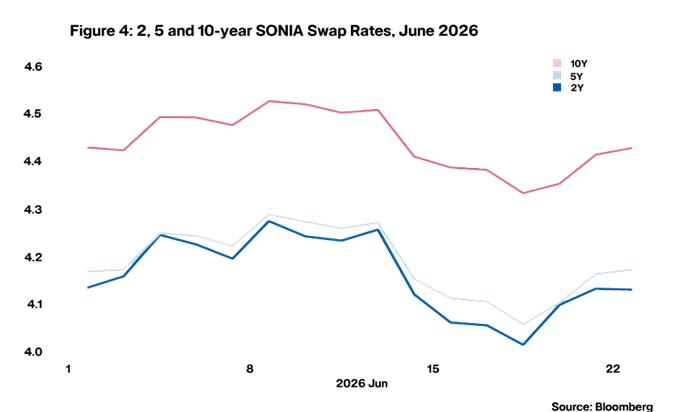

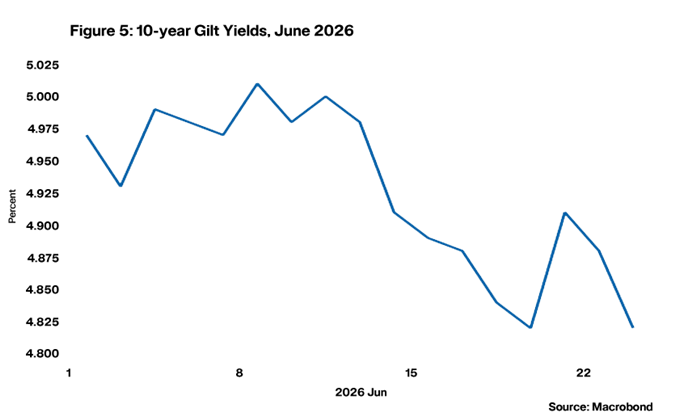

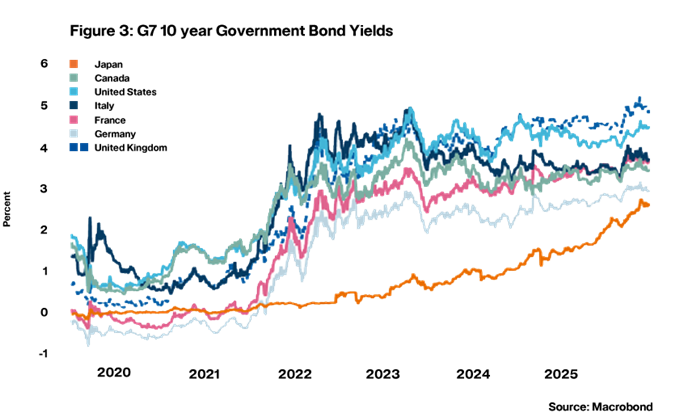

With respect to gilt yields – which were already the highest in G7 sovereign debt markets prior to the Iran war, we have recently published a macro comment with our latest view. Regrettably, gilt yields are likely to continue leading the G7 pack: the UK is very exposed to the trend of rising geopolitical risk. Domestic political risk is likely to remain priced into gilts, at least until the next budget and there is no obvious solution to the current over-reliance on overseas investors buying UK gilts. We do, however, believe that as traffic begins to increase in the Strait of Hormuz and political risk rises up the agenda in the continent next year, the spread between gilt yields and other G7 economies should narrow in the medium term. You can read the report here Opens in a new window.

Daniel Mahoney, Senior Economist, UK