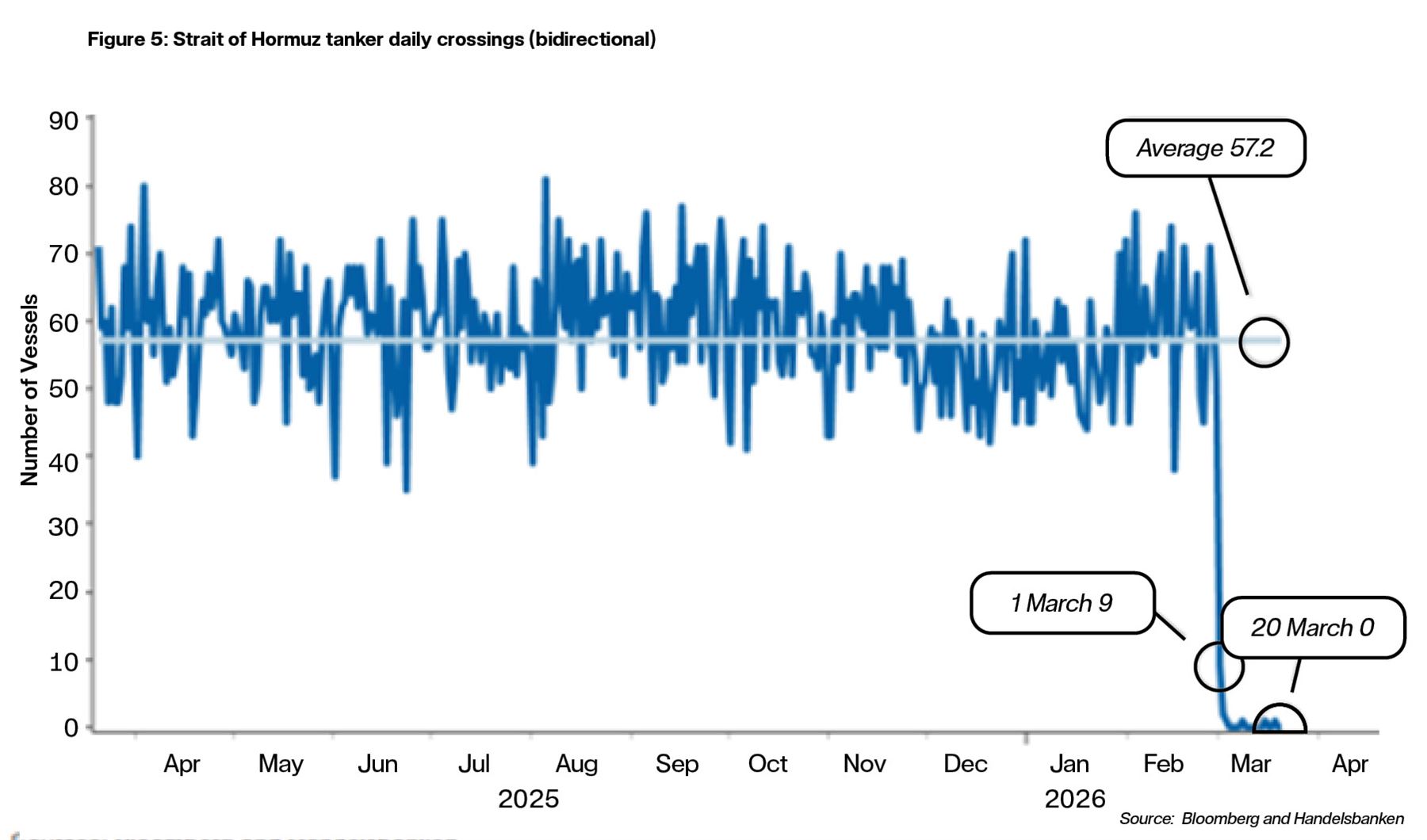

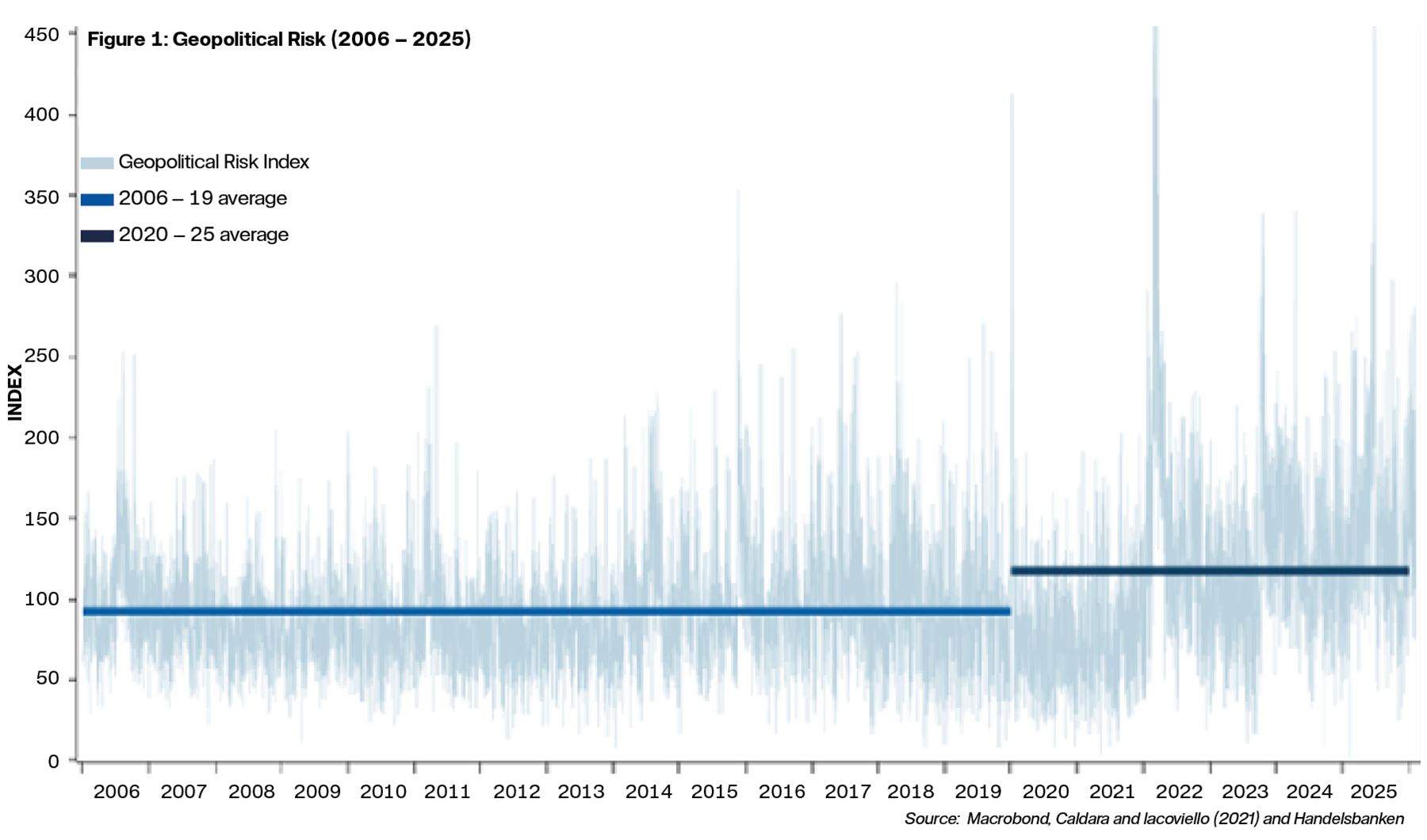

It is difficult to remember now, but only a few weeks ago it was widely anticipated that there would be some further loosening of monetary policy in the UK. The labour market remained relatively weak, wage growth was showing some continued signs of easing and growth prospects were modest – all of which pointed to a few rate cuts this year. We were, however, warning clients Opens in a new window that the UK’s domestic political situation as well as an increase in geopolitical risk meant there was a chance interest rates could rise. Trends in geopolitical risk have for some time indicated that we should expect more numerous and severe supply shocks in future (see Figure 1), and events in March have seen the upside risks to interest rates materialise.

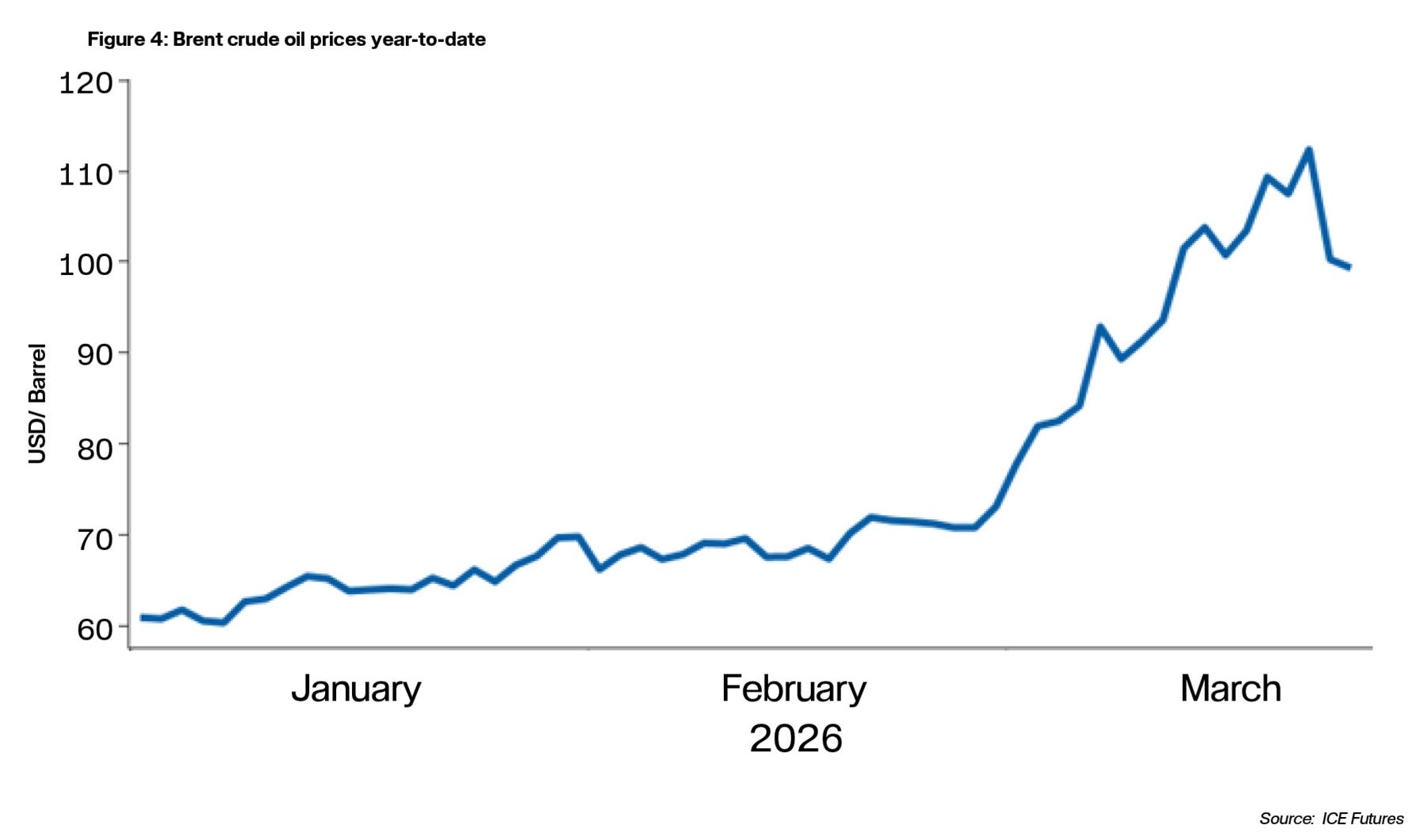

We can already observe from March’s UK PMI reading that the energy supply shock arising from the war in Iran will have a significant stagflationary impact on the UK economy. The OECD has also projected that UK inflation will now be double the Bank of England's target this year at 4%. However, the exact magnitude of the shock is still very difficult to say at this stage given all the uncertainties.

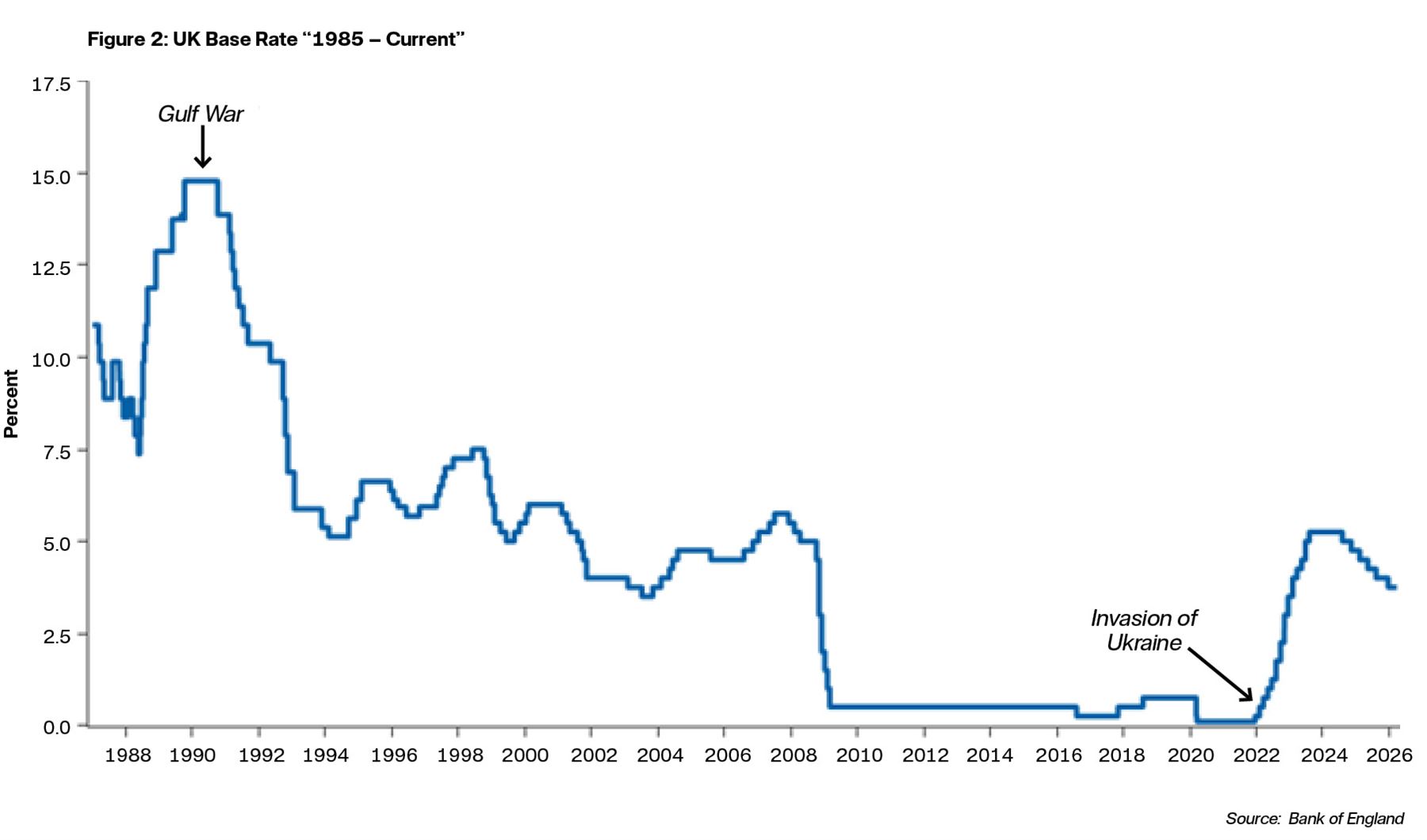

I am not an expert in geopolitics and there is already a lot of speculation about different scenarios – so instead let’s reflect on what we can learn from energy price shocks in financial history, in particular those during the Gulf War in the early 1990s and the more recent invasion of Ukraine in 2022.

When the Gulf War energy price shock hit the UK, interest rates had already previously risen dramatically in response to overheating domestic conditions during the so-called “Lawson Boom”, which is a period that I recently discussed at an event Opens in a new window with former Bank of England Governor Lord Mervyn King, and former Chief Advisor to the Treasury, Lord Terry Burns. Moreover, crucially the UK at the time was a net exporter of energy, so the increase in oil prices led to an improvement in the UK’s balance of payments and had the effect of prompting a deflationary strengthening of sterling. This backdrop allowed an interest rate cutting cycle to begin even during the spike in oil prices.

When looking at the invasion of Ukraine, the macro backdrop was almost the reverse of what preceded the Gulf War. The UK went into this energy price supply shock with ultra-low interest rates and a recently-concluded quantitative easing programme that contributed to excess demand in the economy. This compounded the inflation arising from the supply shocks due to Covid and Russia’s invasion of Ukraine which, of course, precipitated an aggressive increase in interest rates from the Bank of England and other central banks across the Western world.

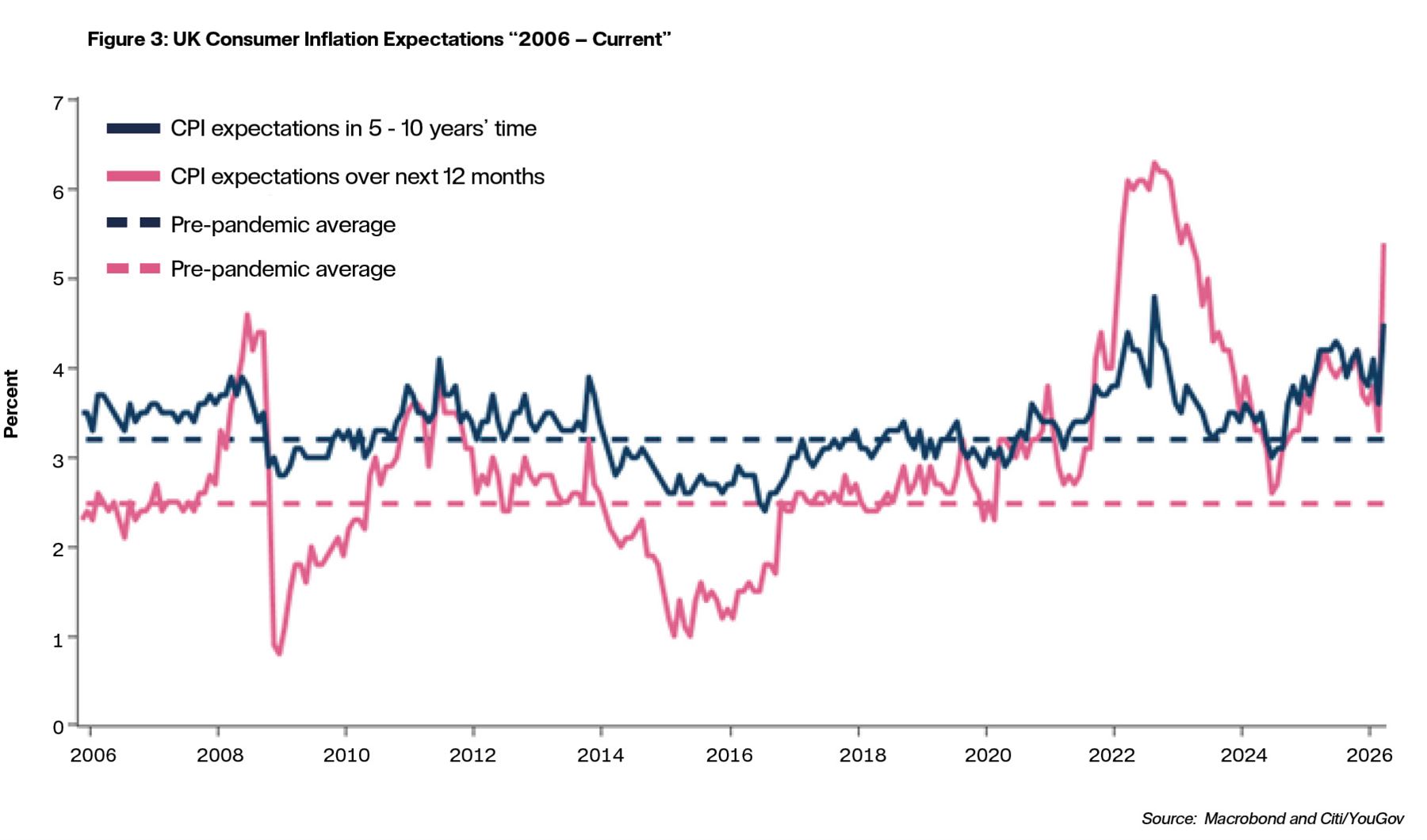

The current situation with respect to monetary policy is somewhere between these two case studies. Monetary policy has been loosened over the past 18 months or so, but we are likely entering into the current supply shock with interest rates that are somewhat higher than neutral levels. Will this allow the Bank of England to “look through” this shock? Most likely not. Even though we go into this period with a headline rate of inflation lower than what was the case during the Gulf War and the Ukraine invasion (3% vs 7% and 6%, respectively), CPI is still notably above the Bank of England’s target, and consumer inflation expectations, both short-term and long-term, have seen an enormous jump in March (see Figure 3).

The MPC’s latest unanimous decision to hold rates at 3.75% shows just how seriously rate-setters are taking this supply shock, and following the outbreak of war in Iran, financial markets have gone from pricing two rate cuts this year to several rate hikes. This new era of higher geopolitical risk may mean central banks’ traditional view of ‘looking through’ ie essentially overlooking, supply shocks, is a thing of the past. We continue to closely monitor the situation with a view to revising our forecasts over the coming weeks. Our next Global Macro Forecast report is out on 28 April.

Daniel Mahoney, UK Economist