Geopolitical risk remains the key driver of movements in UK financial markets and, even before the local elections, UK gilts were showing more signs of volatility compared to other G7 sovereign debt markets. However, domestic political risk will likely exacerbate some of the challenges arising from the energy price shock.

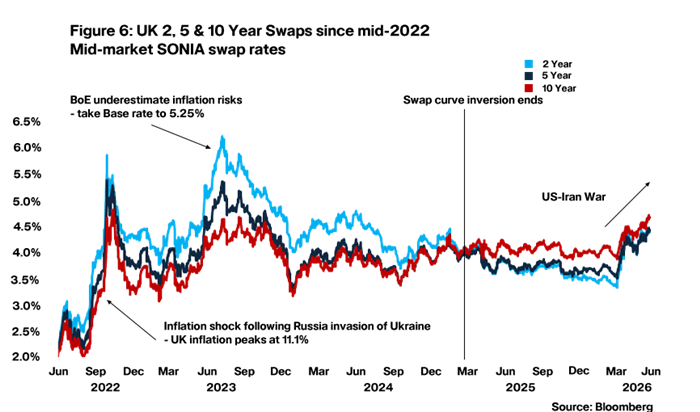

Things are febrile. Since the last Rate Wrap, we have hit an unwelcome milestone of the 30-year gilt yield reaching highs last seen in 1998, while 10-year yields have breached 5% at intermittent points. As news bulletins have been dominated by turmoil in the UK government, a natural question to ask is ‘How much of this can be attributed to domestic political risk?’. The short answer is that, while political turbulence is certainly very unnerving for investors, geopolitical factors continue to be the main story in town.

It is notable that equity markets have been fairly resilient in the face of the Iran war, in large part due to bullish sentiment towards AI-linked stocks, and it is too soon to discern the impact on the UK property market (our recently published Property Investor Report Opens in a new window gives more colour on this). However, concerns related to the energy price shock have led to enormous pressure on government bond markets and, even prior to the local elections, we have seen UK gilts being especially volatile.

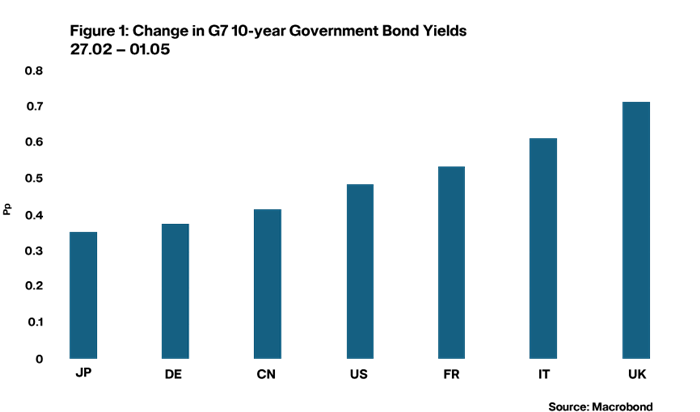

From the end of February to the beginning of May, UK base rate expectations for this calendar year shifted from two cuts to between two and three hikes. Moreover, UK 10-year gilt yields rose more than any other G7 country over this period (see Figure 1). Volatility in UK sovereign debt markets has been influenced by a variety of factors, including inflation risk and the UK’s over-reliance on overseas investors to service its debt obligations.

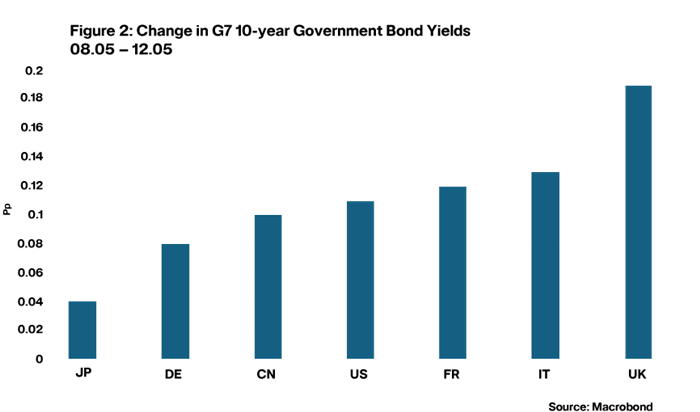

Fast forward to the local elections which took place on 7 May and the UK’s gilt market again witnessed greater volatility in comparison to G7 sovereign debt markets. And this time around, of course, the critical factor appeared to be UK political risk associated with the fallout from the government’s disastrous performance at the polls. After the results flowed in, outsized movements in UK gilts were observed almost immediately as speculation about the prime minister’s future gathered pace. Moreover, a similar situation occurred when it was announced that Andy Burnham, currently Mayor of Greater Manchester, was likely to stand in a by-election to enter parliament and challenge Sir Keir Starmer for the leadership.

Note: This period captures the immediate aftermath of the UK’s local elections

Many will welcome that for a few short weeks UK political risk is now likely to take somewhat of a back-seat as we await the outcome of the Makerfield by-election. However, whatever the result, instability in the government will likely follow. And if Andy Burnham were to become prime minister, an outcome which is highly likely if he wins the by-election, his previous comments about not wanting to be in hock to the bond market will naturally make investors nervous. They may end up being reflected in UK borrowing costs, at least initially, even though he has since tried to row back on this view. Some commentators estimate that this outcome could end up adding another 30 – 40bp to 10-year gilt yields.

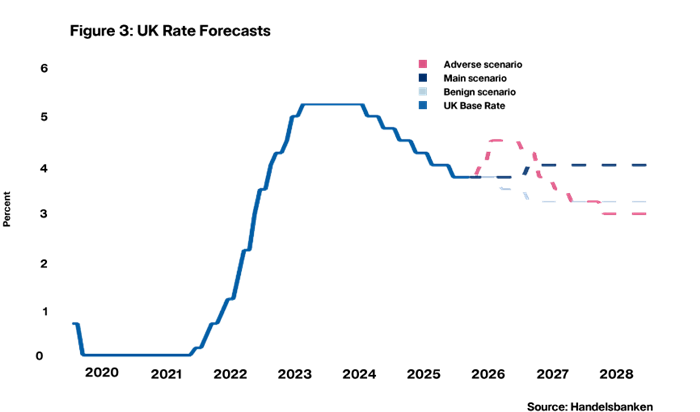

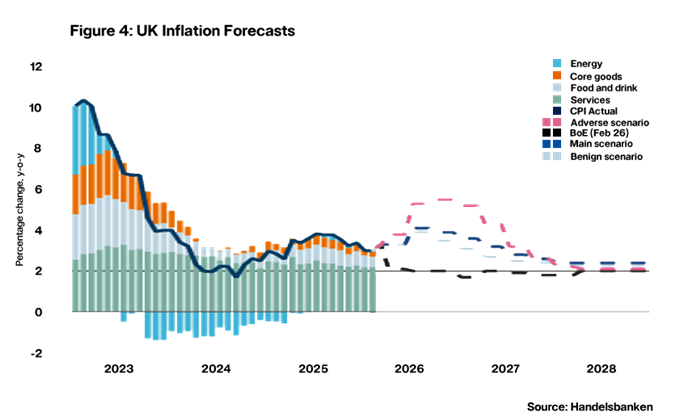

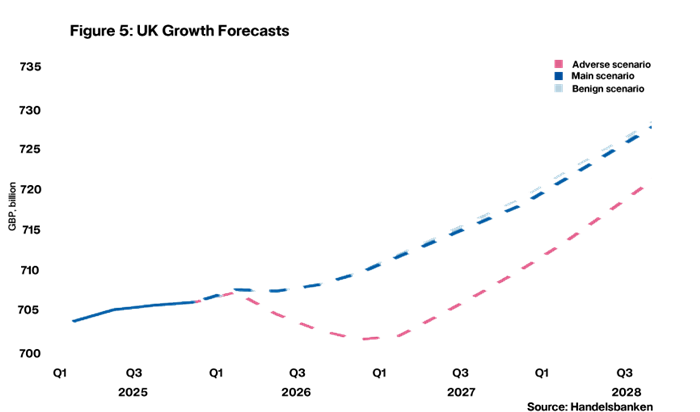

In summary, the energy price shock arising from geopolitical instability is the key driver of negative movements in UK financial markets and the macro outlook, but UK political domestic risk is exacerbating these challenges. In our latest Global Macro Forecast Opens in a new window, we have set out three scenarios for how this backdrop could play out for the UK economy: a benign scenario, a base case (central view) and an adverse scenario. Oil price futures would suggest the current situation (as of 20.05) is slightly worse than our base case scenario, which points to a UK inflation peak of over 4% and the next move in interest rates being upwards.

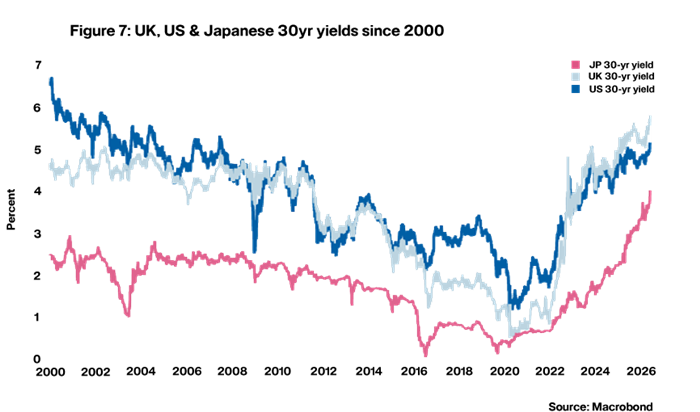

We are currently on course to avoid recession this year, although the collapse in May's business PMI reading shows that private sector activity is taking a major hit. And should an adverse scenario end up playing out, our judgement on this would change due to the government lacking any material fiscal tools to respond. The UK, after all, is currently paying the highest level of interest on its newly issued debt within the G7, a situation that has been present since the beginning of 2025.

Daniel Mahoney, Senior Economist, UK