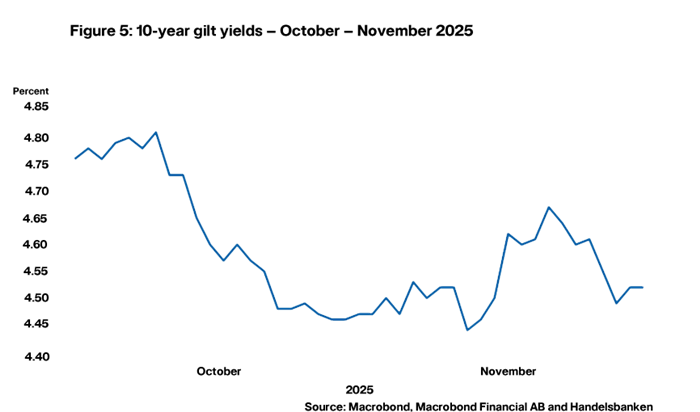

It was some time ago now but let’s firstly reflect on November’s MPC decision. The vote was split down the middle with Governor Bailey tipping the balance in favour of holding rates rather than the committee voting to cut rates by 0.25pp. The committee is clearly beginning to move in a more dovish direction; for example, the guidance of, “a gradual and careful approach to further withdrawal of monetary policy remains appropriate” has been replaced by, “if disinflation continues, the bank rate is likely to continue on a gradual downward path”. But why was the committee not able to agree on a cut to interest rates?

Inflation expectations were cited by a majority of the MPC members who voted to hold rates. As discussed in the previous Rate Wrap, the base-case view of financial markets (the inflation swaps market) is sanguine with respect to longer-term inflation in the UK, but this is not the whole story. Inflation risk has been contributing to the term premia in the longer end of the gilt market and UK consumer inflation expectations appear to be high at the moment. Longer-term consumer inflation expectations are, of course, more influenced by temporary short-term spikes in inflation and by high food prices. Yet, regardless of what drives consumer expectations, they matter given 60% of UK GDP is made up of household spending decisions.

There are also three key reasons why there is a higher risk of raised expectations leading to higher realised inflation in the post-pandemic era:

- There has been a very significant spike in inflation in recent times, which may serve to make anchoring longer-term consumer expectations more difficult now and in the future;

- UK inflation is currently sitting above the level at which the correlation between expectations and realised inflation strengthens;

- The service sector’s dominance of the UK economy may render it more prone to second-round effects compared to economies with less of a concentration of services such as the eurozone.

If you’re interested, you can read more on this topic in our recently published paper How concerned should we be about elevated consumer inflation expectations? Opens in a new window.

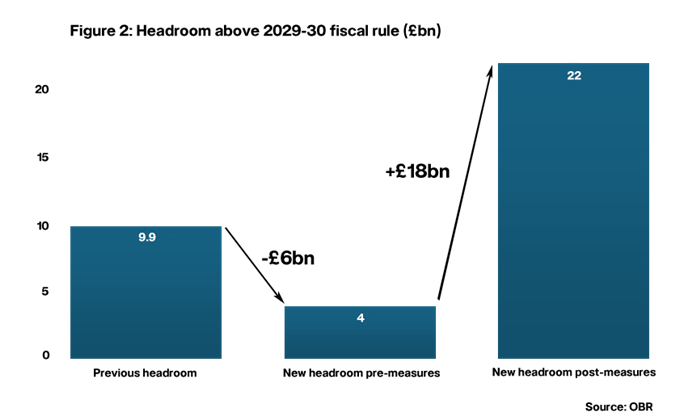

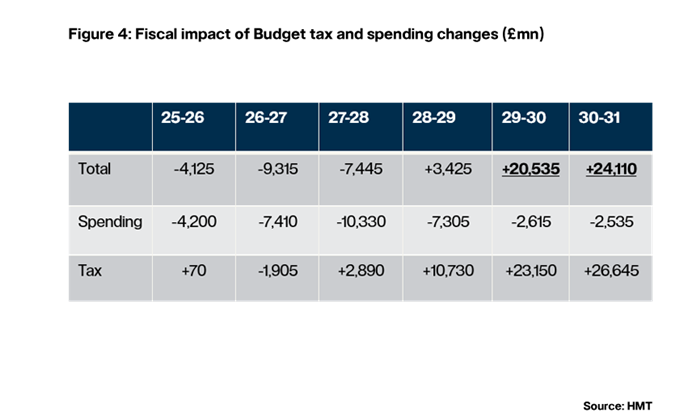

Turning to the budget, we were keeping our eyes on three broad macro indicators. First, how much headroom would there be above Chancellor Rachel Reeves’ fiscal target; second, would fiscal consolidation be front-loaded or backloaded; and third, would there be any measures for growth?

On the first, the OBR was unexpectedly kind to the chancellor. While it downgraded future annual productivity growth forecasts from an average of 1.3% to 1%, the future fiscal impact of this was largely offset by an increase in expected tax revenues arising from earnings growth forecasts being revised up. Pre-measures, Reeves was left with £4bn of headroom to which she added £18bn of measures in the budget.

On the second and third metrics, the news was far less market-friendly: the budget increases spending over the next three financial years and backloads tax increases to the end of the decade. And there was very little in the budget to promote growth. It is notable that the OBR has downgraded its growth forecasts for 2026 onwards. Despite this, financial markets reacted relatively well to the budget, perhaps taking comfort from the OBR’s better-than-expected forecast for government finances and the improved headroom above Rachel Reeves’ fiscal target. But fiscal sustainability worries will no doubt linger: the budget raises borrowing over the next few years, fiscal consolidation somewhat lacks credibility due to it being backloaded, and inflation persistence remains a concern.

In terms of what the budget means for the rate pathway, the truth is — not a huge amount. Yes, a December rate cut is now almost a dead cert, particularly as the measures on energy costs will lower inflation next year, but it is notable that an overall fiscal loosening over the next three financial years and a backloading of fiscal consolidation will do nothing to help the Bank of England cut rates further. After a cut in December, the Bank of England will be very cautious with respect to continuing the rate cutting cycle.

Daniel Mahoney, UK Economist