September’s UK inflation print brought a rare bit of good fiscal news for Chancellor Rachel Reeves. The expectation was that headline inflation would rise to 4% but in the event it stayed flat at 3.8%. In the run up to the budget, this helps the chancellor in two key ways: first, gilt yields dropped on the news and have now fallen during a time period that the OBR is likely to use in its forecasting assumptions. Second, the government’s welfare bill will rise by less than expected, given September’s CPI figure is used to index benefits. While this helps somewhat reduce the government’s fiscal black hole, November’s budget still presents major challenges for Rachel Reeves to meet her fiscal targets – something I will come back to later on.

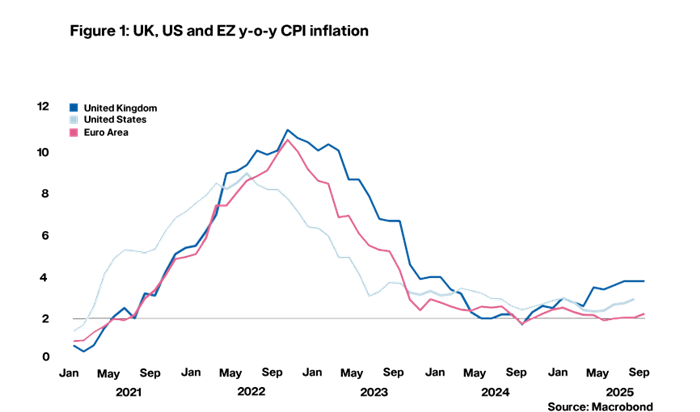

The undershoot in CPI is also, of course, a welcome bit of news in the UK’s fight to get back to 2% inflation in the medium term. However, UK inflation remains nearly twice the Bank of England’s target and continues to be an outlier when judged against comparators in the developed world (see Figure 1). This discrepancy is largely accounted for by significant increases in UK regulated prices that came into force in April this year, but inflation expectations in the UK are leading to worries about the potential for inflation persistence.

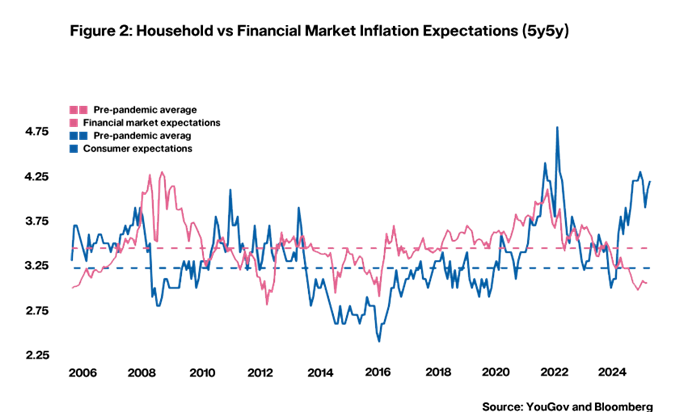

How worried should we be about inflation expectations? It depends who you ask. Consumers seem to be concerned: their expectations for inflation in the medium to long term are elevated at the moment, no doubt due to high food price inflation that is very visible to households on a day-to-day basis. Financial markets, on the other hand, disagree with households on this point: their current expectations for inflation in 5-10 years’ time are lower than the pre-pandemic period (see Figure 2). Who’s right remains an open question and it is a topic to which we will return to in future Rate Wraps.

Back to the upcoming November budget. Despite the good news coming from September’s inflation print, it would still seem reasonable to assume that Rachel Reeves will need to raise £25 – 30bn and that most of this will likely come from taxation. The fiscal gap will mostly be driven by a combination of downgrades to expected productivity growth as well as government U-turns on welfare reform. Moreover, in an attempt to sooth financial markets, the chancellor is also expected to try and leave a higher level of headroom for her fiscal targets compared to last year. Freezing of income tax thresholds as well as the introduction of some environmental and “sin taxes” seem almost certain to happen, but this will still leave a major funding gap and it remains to be seen what other measures will come forward. The sums of money involved mean Rachel Reeves may even have to breach the government’s manifesto commitment not to change income tax rates.

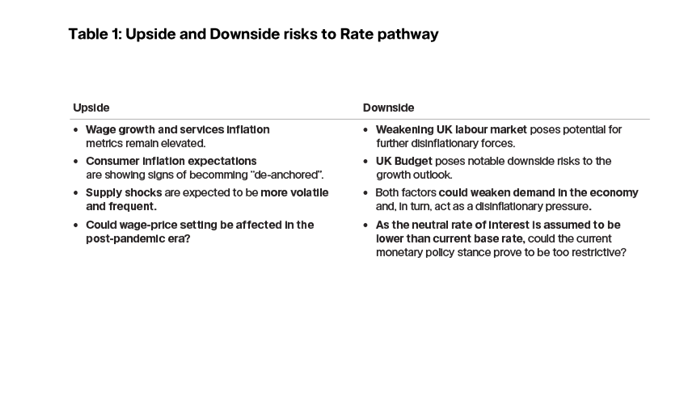

In terms of what this all means for forecasted rates, we continue to believe the evidence points to a cautious continuation of the rate cutting cycle. Our call at the moment is for there to be a further three rate cuts over an extended period of roughly 18 months as rate-setters continue to balance inflation persistence worries with signs of labour market weakening. There are, of course, a variety of upside and downside risks to this forecast for base rate pathway outlined in the table below, but I would say that these risks are now finely balanced.