In one respect, the September Monetary Policy Committee (MPC) meeting was pretty uninteresting. The key language relating to the future of UK base rates remains in place (a “gradual and careful approach to further withdrawal of monetary policy restraint remains appropriate”); the vote to hold rates at 4% by a seven-to-two vote was broadly expected by markets, and inflation risks continue to be on the upside. In essence, the MPC’s positioning was roughly the same as it was in August, which is set out in more detail in last month’s Rate Wrap.

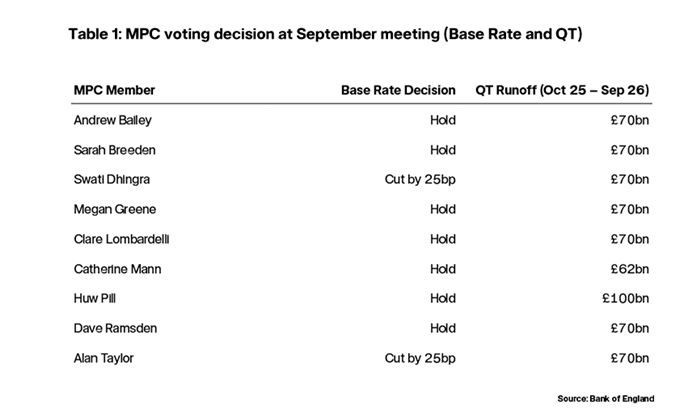

However, all eyes were, of course, on the decision made in relation to quantitative tightening (QT), something that began back in 2022. To date, this process of shifting government bonds from the BoE’s balance sheet back to the private sector has been running at a pace of £100bn per year, and this is something that has previously been unanimously agreed by all members of the MPC. Not this time, however. Every September, the MPC has to vote on the level of QT over the following 12-month period and, on this occasion, a majority of members voted to slow the pace of QT to £70bn, with just one member arguing that it would be appropriate to keep the QT pace at £100bn per year (see Table 1).

The BoE has stated three clear principles with respect to its QT programme: first, that base rate is the primary tool of monetary policy; second, that the process should be smooth and predictable and, third, that financial market functioning is maintained. In light of its most recent vote, the MPC is indicating that at least one of these principles would not be maintained without reducing the pace of QT.

Prior to the meeting, MPC member Catherine Mann had expressed her concern about monetary policy pushing in different directions on the gilt yield curve. In summary, while base rate falls have been pushing down yields at the short (ie, 2 or 5-year gilts) end, the QT programme has effectively had the opposite effect at the long end (eg 30-year) of the gilt market, which is acting to steepen the yield curve. As I set out in my Decision Time interview with CNBC Opens in a new window, the MPC’s recent decision to slow the pace of QT is effectively an acceptance of this argument.

The MPC’s decision in September attempts to reduce the impact that QT will have at the long end of the gilt market via two key channels. First, over the next 12 months, the BoE will only sell £22bn of its government bonds to the private sector before they mature (a process described as “active” selling) rather than £52bn of active sales that would have to take place if QT were sustained at its previous run-off rate of £100bn a year. Second, the BoE has been clear that the majority of active sales that do occur over the next year will not be at longer-dated maturities of gilts.

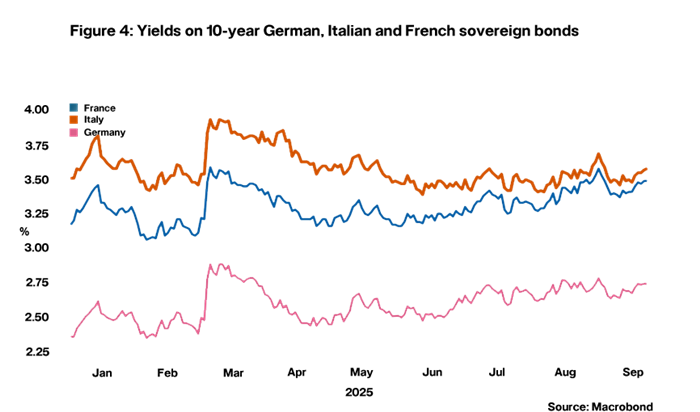

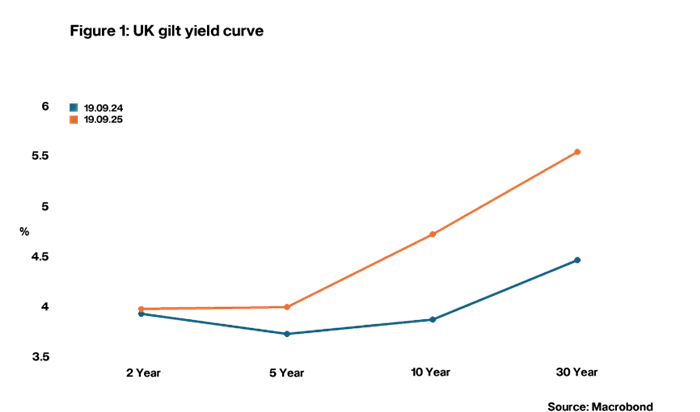

The long end of the gilt market has seen rapid increases in yield recently, with the 30-year jumping by over a full 100 basis points over the past 12 months (see Figure 1). This has been the source of much commentary in recent weeks. It’s important to stress that this dramatic movement in the 30-year gilt yield has mostly related to factors such as fiscal sustainability concerns, inflation risks and a drop in demand for long-dated gilts from pension fund buyers. However, QT may have been somewhat exacerbating the problem, leading the BoE to reduce the level of QT going forward in order to try and minimise its future impact on the gilt market.

Daniel Mahoney, UK Economist