All change once again

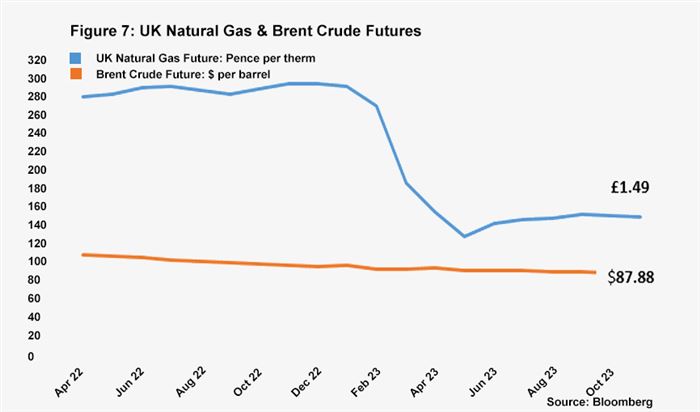

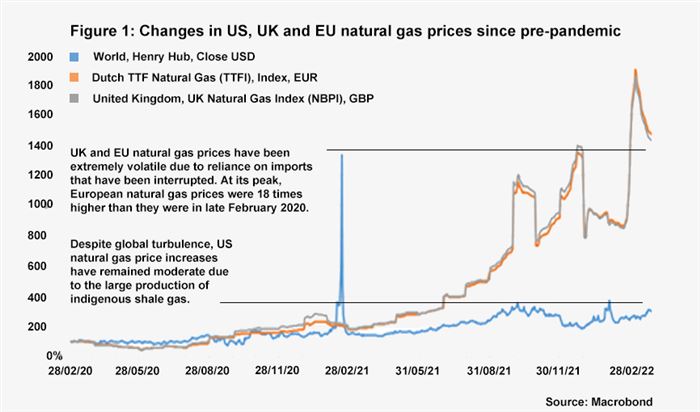

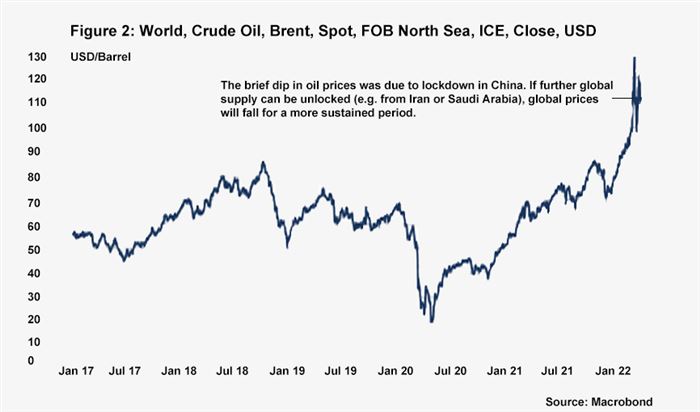

There has been a good deal of commentary that the Russian economy (GDP = $1.5 trillion, before they invaded the Ukraine according to the IMF) being only slightly smaller than that of Italy ($1.9 trillion) but larger than that of Spain’s ($1.3 trillion). The implication being that the Russian economy is not of sufficient size to really be of long lasting concern to the rest of the world. However, that doesn’t take into account how Russia dominates a few narrow but critical supply categories, most notably in energy (12 percent of global oil and 40 percent of gas to Europe). Breaking that market down, Russia produces both significant amounts of oil (for which there are a host of alternative global suppliers), and gas (a more regional market where finding alternative supplies is far more difficult). In practice this means energy price rises across Europe are likely to be far more lasting than anticipated, with electricity prices in particular, likely to remain higher, for longer than petrol prices.

Are interest rates going to break the housing markets?

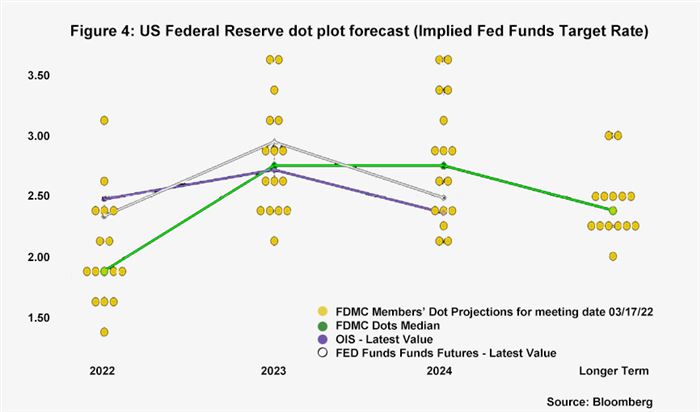

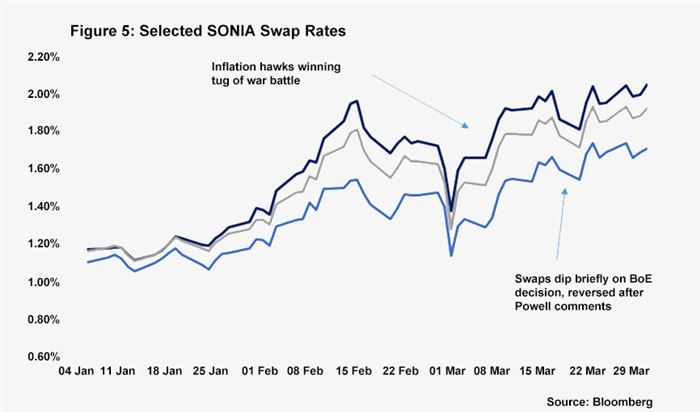

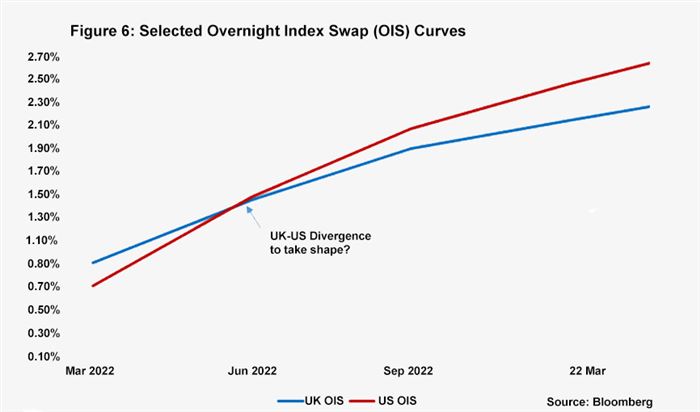

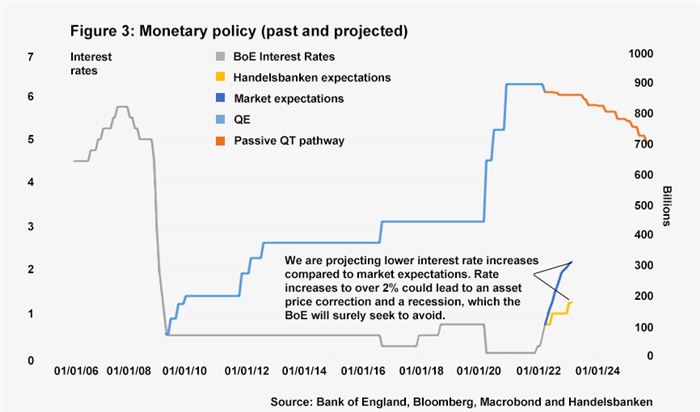

The higher levels of inflation resulting from these increases to the cost of energy, clearly require a response from central banks. Already the Bank of England, as well as the US Federal Reserve, are tightening monetary policy. If one simply looks at the path financial market investors expect interest rates to follow, you might conclude that rates were headed north of two percent within the next year. This would put interest rates close to, what is assumed by academics, would be their “neutral” level; sufficiently high to counter inflation, but not so low as to encourage asset bubbles or mal-investment. While such a move would meet central banks’ mandate to counter inflation, there could be a disproportionately hefty cost to pay as well. Our view is that the prolonged period of extraordinarily low interest rates, which has dominated monetary policy around the developed world since the Global Financial Crisis of 2008, has resulted in inflated asset prices. Moving to what might be considered more historically “normal” valuations, while desirable, has to be done carefully. A rapid asset price correction would likely trigger a recession of the sort experienced in 2008-09, particularly if it is centred on people’s biggest asset, housing. Because central banks have a mandate to counter inflation, but not a carte blanche to pursue this at any cost, we do not think such a path to 2.5 percent is likely. As the boss of US bond fund PIMCO, Bill Gross, commented to the FT in March, a rapid move towards theoretical neutral levels of 2.5 percent, would crash the overall housing market. He was looking at the US, but the same could be said of the UK housing market. Asset prices have taken a good deal of time to rise to present valuations, the best we can hope for is that we take our time reversing the situation.

James Sproule, Chief Economist