All eyes on inflation again

Financial stability concerns that arose after March’s market turmoil have now mostly subsided. This can clearly be observed in the credit default swaps market (effectively a market that insures against default) for major banks, which has calmed significantly over the past couple of weeks. So, the focus now is very much back on the fight against inflation, and the week commencing 17 April produced a series of data releases that significantly changed the outlook. Employment and earnings data on Tuesday showed some tentative signs of labour market loosening, but nominal wages registered at much higher levels than expected with average pay including bonuses coming in at 5.9% for December 2022 to February 2023 versus consensus of just 5.1%. On the following day, the y-o-y CPI inflation figure for March was released which, while down from the previous month, came in higher than expectations at 10.1%. This of course followed February’s inflation print significantly overshooting expectations, too. In summary, inflation is running hotter than previously anticipated.

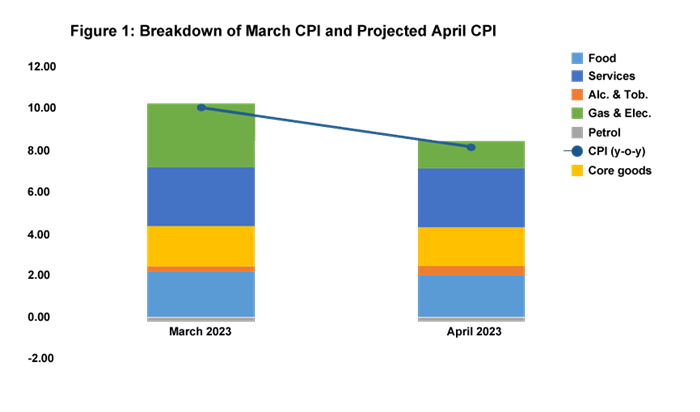

April’s y-o-y CPI figure will see a notable drop compared to March, potentially by nearly two percentage points, but note that this will mostly be due to base effects playing out with the gas and electricity component of inflation. While energy prices faced by households will be the same in March and April, the nature of Ofgem’s price cap means they will be compared to different data points for the purposes of calculating CPI inflation and this alone will lead to a significant drop in April’s y-o-y CPI. Other base effects throughout the year and factors pushing down on inflation in absolute terms, such as collapsing shipping costs, should mean that y-o-y CPI inflation falls to around 4% by year end. However, CPI inflation from this point onwards is likely to be driven by services inflation that could be more sticky given the influence that wage costs play in setting prices within that sector.

Markets are now fully pricing in a 25bp increase in interest rates at the Monetary Policy Committee’s May meeting, and we share this view in light of the most recent labour market and inflation prints. This would take rates up to 4.5%. The pace of interest rate increases has been very rapid so it is important to emphasise that the full effects of monetary policy typically take around six quarters to be fully transmitted into the wider economy. As a result, we believe that MPC members will take the view that an increase in May will be the last hike in this cycle. We do, however, expect rates to remain elevated at 4.5% from May until the end of this calendar year given the likely stickiness of services inflation.