Concerns about persistent inflation pushing back interest rate cut expectations

On 13 April, we learned of the news that Iran had launched hundreds of drones and missiles at Israel in what briefly seemed like the potential start of major regional conflict across the Middle East. The lack of damage caused by the attack and the limited military response from the Israelis meant that the conflict was de-escalated. Markets breathed a collective sigh of relief. Global oil and European gas markets remained sanguine, although the latest tit-for-tat brought to the fore just how disruptive any regional conflict would be. Disruption to shipping in the Strait of Hormuz, for example, would have a huge destablising impact across global markets: 30% of the world’s oil trade and 20% of global LNG trade passes through this area alone.

There is another point worth making, which is that supply shocks arising from geopolitical risk and other factors could occur more frequently and with greater severity over the next twenty years compared to the previous twenty years. Historically policymakers setting monetary policy would “look through” supply shocks when determining interest rates. However, a potential increase in supply shocks could end up having a more material impact on demand-side inflation, which could force central banks into more hawkish positions.

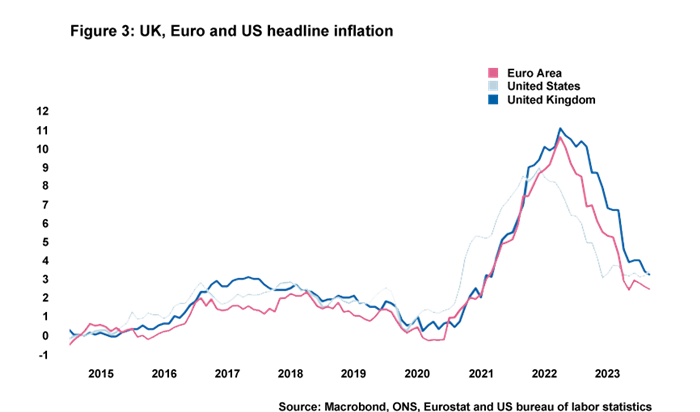

That said, the aversion of broader regional conflict in the Middle East, for now at least, means that markets are primarily focused on what recent data prints are indicating about the stickiness of inflation. UK CPI y-o-y is down to 3.2% in March and due to base effects will likely hover at around the 2% inflation target for a few months from April. Yet there is still no certainty that inflation will stay at this level in the medium term, not least because the National Living Wage has increased by a near 10%. April’s PMI numbers highlight that this is causing many businesses to see significant pressures on labour costs, and the majority of MPC members will likely want to observe how this ends up affecting wage growth numbers across the economy before backing interest rate cuts.

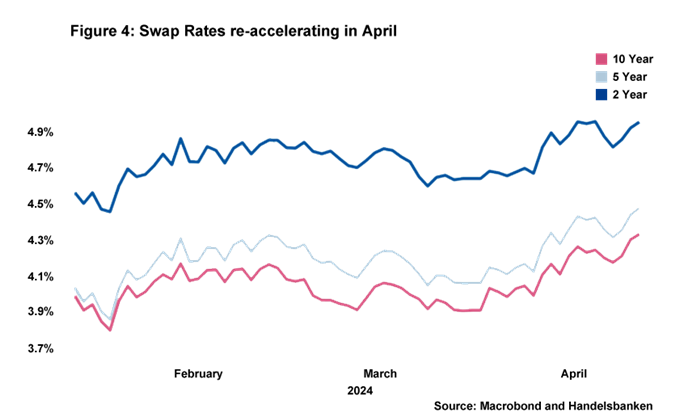

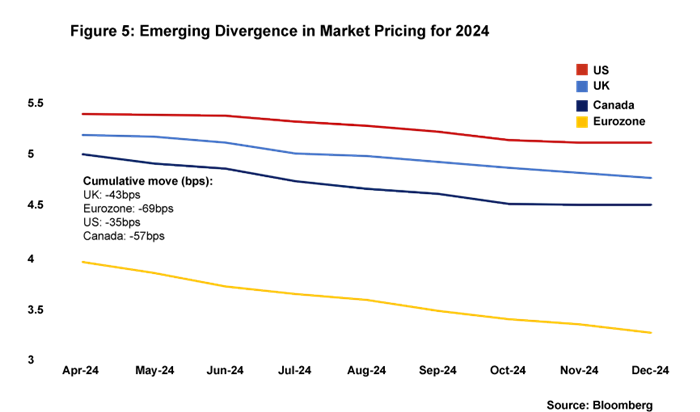

Across the Atlantic, data releases are beginning to make markets worry a little about US inflation. US CPI inflation has now overshot market expectations for three months running. This has served to dial back expectations of rate cuts not only in the US but also in the UK and the Euro area. Moreover, the previous narrative that the Federal Reserve would likely be the first of the three central banks to cut rates is not looking by any means certain. US headline inflation is now higher than the UK’s and the gap is due to widen over the next couple of months, leading Governor of the Bank of England Andrew Bailey to indicate the BoE may end up moving earlier than the Fed.

We think there remains sufficient concern about persistent inflation for there certainly to be no moves in UK interest rates at the next two MPC meetings (May and June). We are currently tilted towards the first cut happening in September, with a reasonable chance of it coming earlier in August if the data outperforms market expectations.

Daniel Mahoney, UK Economist