What is the MPC considering when judging where rates should peak?

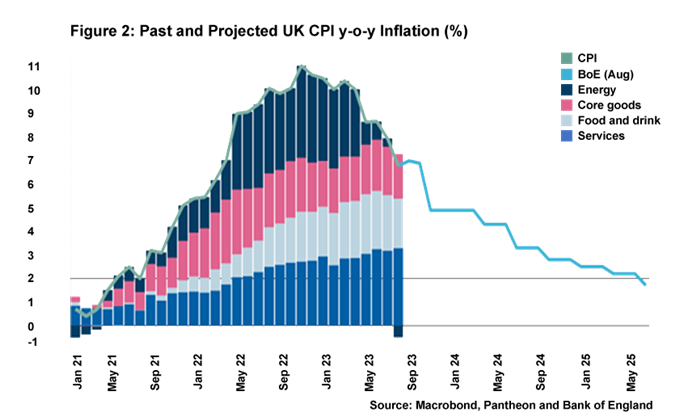

The August Monetary Policy Committee (MPC) meeting led to interest rates rising by 0.25pp up to 5.25%, as widely expected, and the economic outlook presented in the quarterly inflation report was not too dissimilar from that published in May. The UK is expected to avoid a technical recession, but continue to grow slowly in the near term, while inflation is set to remain above target until Q2 2025 (we are currently projecting that it will take even longer than this to hit 2% inflation).

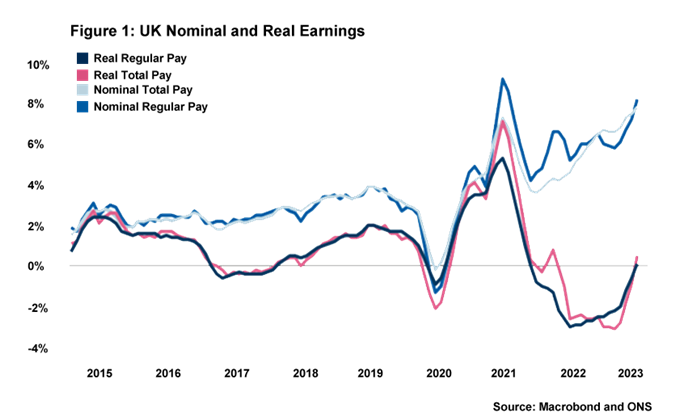

The last two months of data (June and July) have seen significant drops in UK CPI. Y-o-y CPI rate fell from 8.7% to 7.9% in June and down again to 6.8% in July, owing mostly to a combination of absolute falls in energy prices and prices being compared to very high figures from last year (the base effect). The fall in inflation has been significant enough for real wages to edge into positive territory for the first time since late 2021. This should help prop up disposable incomes at a time of stretched household finances, and might even eventually boost consumer confidence that has been weak for some time now. These weak consumer confidence levels have spilled over into the PMI numbers, which have fallen to the point where a majority of businesses are expecting a recession in the coming 12 months.

Dynamics behind the current process of falling inflation are now becoming clear. Energy (inc. motor fuel, electricity and gas prices) is now contributing negatively to y-o-y CPI, while goods inflation is starting to show promising signs of disinflation as lower shipping costs and supply chain distribution start feeding into prices. On the other hand, the services component of y-o-y CPI, where labour costs are key, continues to creep up and will almost certainly be the reason why inflation remains sticky once headline rate gets to between 4 and 5%.

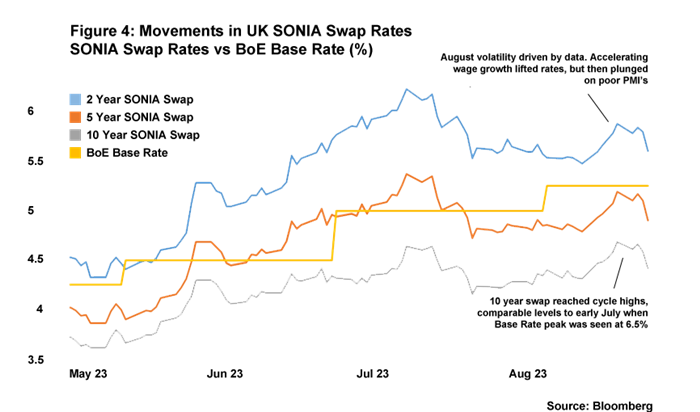

A quick couple of interesting points made by MPC members at the Bank of England (BoE) press conference following the August decision. First, Ben Broadbent remarked that the impact of rate increases on the mortgage market accounts for “barely a quarter” of the monetary policy transmission mechanism. He emphasised that this was a rough estimate, but his comment would appear to suggest that the MPC is relatively unconcerned about the growth of fixed-rate mortgages leading to major disruption in monetary policy transmission into the economy.

Second, Dave Ramsden commented on the key metrics that the bank is looking at when making interest rate decisions. He cited three key measures: services inflation, private sector wage growth and labour market tightness. As previously mentioned, services inflation remains stubborn – in large part due to nominal wage growth being very high and not consistent with the bank’s inflation target (average private sector pay is north of 8% in the latest labour market release) – which will of course maintain pressure on the MPC to act. Yet rate setters will also have to take into consideration strong signs of the labour market loosening. For example, unemployment has now risen more than expected in two consecutive months and inactivity levels have been on a downward trajectory since mid-2022.

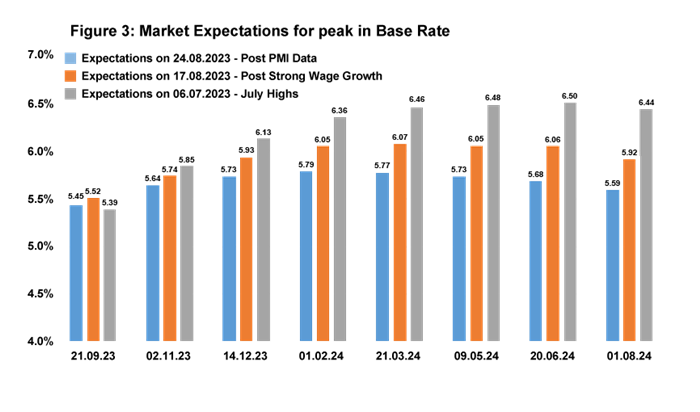

August’s and September’s y-o-y CPI figures are likely to show little change, so it will be especially important to scrutinise these metrics in upcoming labour market and inflation releases to gain an understanding of what the MPC may decide to do with interest rates over the remainder of this year. There are, of course, lots of moving parts internationally – not least in China’s banking and property sectors – that have the potential to change the outlook for rates. But for now our forecast is for a further 25bp hike in BoE rates in September. While we note that financial market investors continue to expect the peak to be somewhat higher, we also note that they have been moving steadily closer to our forecast over the course of the summer.

Daniel Mahoney, UK Economist