The Bank of England’s Monetary Policy Committee (MPC) cut base rate in August but the vote was more hawkish than expected as the bank raises its near-term inflation forecast. Given supply side improvements could be some way off, this points to upside risks on inflation and bank rate pathway.

In advance of August’s MPC meeting, it had been thought that a rate cut was “a dead-cert”. Markets had expected a two (0.5pp cut) – five (0.25pp cut) – two (freeze) vote split, yet while base rate did come down from 4.25% to 4%, the vote breakdown was on a knife-edge. Four members voted to hold rates while five argued for a 0.25pp fall in rates (with one member Alan Taylor initially calling for a 0.5pp cut).

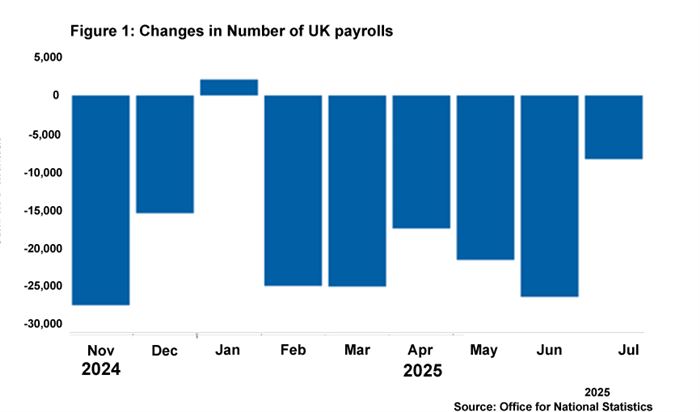

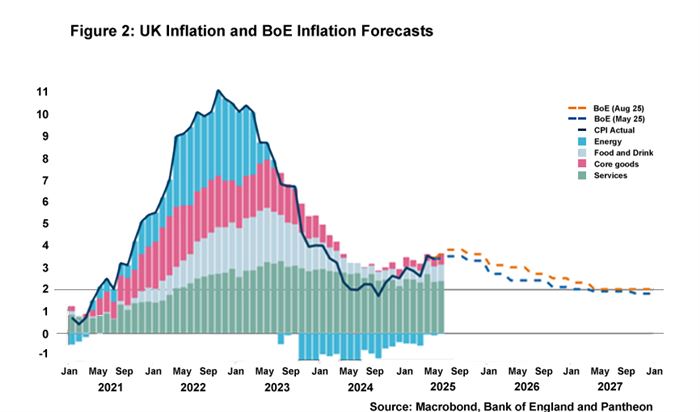

This signifies a notable hawkish pivot on the MPC. The narrow majority of members backing a rate cut used continuing evidence of labour market weakening to justify their votes, although there remains a difference of opinion among these members about how fast this will be reflected in disinflation of services inflation and wage growth. However, as previously stated, four MPC members felt unable to ease the restrictiveness of monetary policy at this meeting. These members are placing much more emphasis on the risk of second round effects arising from the elevated headline rate. Even before this meeting, UK inflation was expected to be north of 3% until at least April and the Bank of England has now somewhat revised up its inflation forecast. In particular, the near-term forecast has risen, meaning there is now likely to be a peak in y-o-y CPI of 4% later this year, and this is being accompanied by signs of consumer inflation expectations becoming unanchored.

Since the MPC vote, we have had Q2’s GDP print which registered at 0.3%. Even though this was better than markets had expected, it does not seem to be anything to shout about given that the upside surprise appears, at least in part, to be driven by higher-than-expected government spending. All signs continue to point to a year of below-trend growth, and there continues to be disagreement about whether demand or supply factors are driving these growth dynamics.

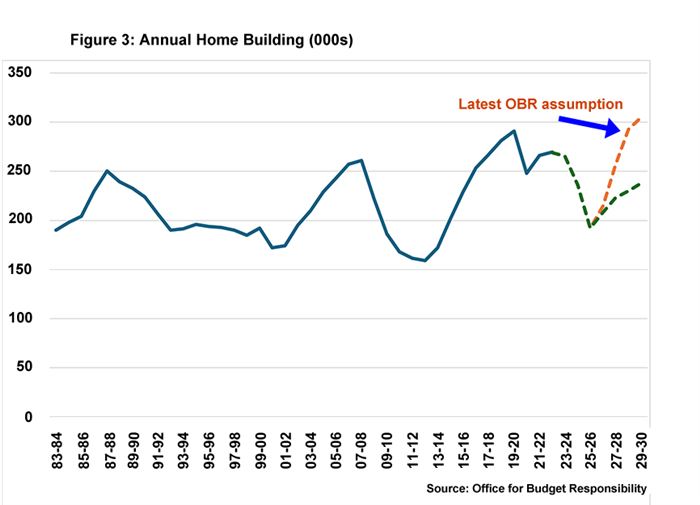

In terms of improving future growth prospects, two factors are often cited as sources of a potential boost to the productive potential of the UK economy: planning reform and the adoption of artificial intelligence (AI). It would seem advisable to exercise a degree of caution regarding the short-term impact on the supply side from either of these factors. First, there definitely appears to be some over-optimism about improvements. For example, the Office for Budget Responsibility’s current forecast of planning reforms helping to boost house-building to 300,000 new homes a year by the end of the decade seems a stretch. Moreover, any improvements that do take place will have a reasonably long lead time. It is notable that a recent study from the OECD suggests that only 2 – 6% of businesses in the G7 have adopted high-intensity use of AI, highlighting that its benefits are currently confined to a small number of sectors.

The MPC’s latest hawkish pivot coupled with the fact that any supply side improvements will take time to filter through into the economy suggests upside risks to both inflation and the path of interest rates in the UK in the shorter term. Prior to the August rate decision, markets had fully priced in another rate cut this calendar year but, as of 29.08, the chances of this happening have fallen to below 50%. Look out for Handelsbanken’s latest economic forecasts for the UK and global markets which will be published on 10 September.

Daniel Mahoney, UK Economist