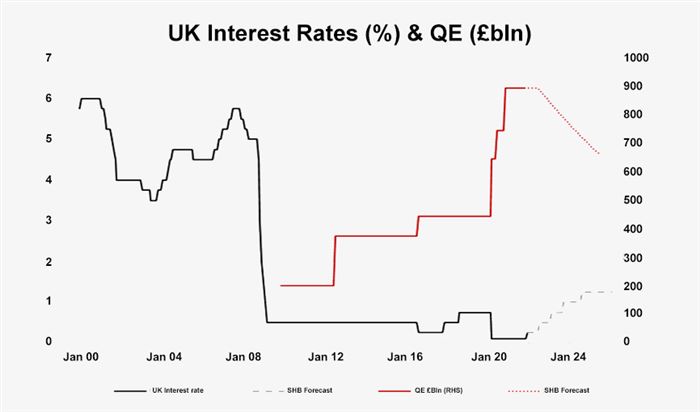

MPC surprises markets with rate rise to signal new path

The Monetary Policy Committee (MPC) of the Bank of England once again has surprised markets with its decision to raise interest rates to 0.25%. What sort of an impact this will have on inflation remains unclear, but it is useful in signalling which way policy is going to be moving over the course of 2022, as well as the importance that the Bank attaches to countering inflation. The big question is of course the potential impact of Omicron which has further dampened the economic outlook. While there is currently not an official lockdown, people are reportedly staying away from the office and social gatherings, which amongst other things has impacted the Flash Purchasing Managers Index for December, which plunged from 57.6 to 53.2.

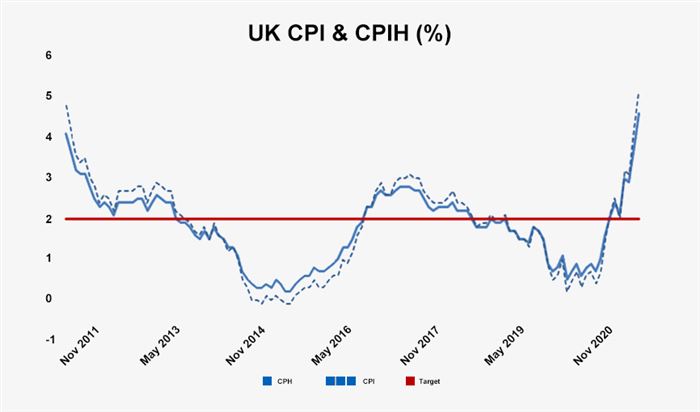

Inflation has become the overriding concern

The interest rate decision has been driven by two factors. Firstly, the inflation data for November saw inflation at 5.1%, a level that the MPC had not expected would be reached until next Spring when tax hikes set for April kick in (April inflation is now expected to be 6%). There remains the expectation that much of the inflation we are experiencing at the moment is transitory (even if that word is used less frequently), and it is true that a good deal of today’s inflation is due to energy prices, which are expected to slowly fade from next summer onwards. That said, there are also growing concerns that inflation is being incorporated into pay settlements more generally and that expectations for a rapid reversion to mean for energy prices is far from certain. Our view is that inflation will fade from May 2022 onwards, but is going to remain above the 2% target throughout the year. The second issue is the broader international monetary policy set by the Fed and the European Central Bank. While we are not looking for a rapid rate rise by the ECB, the Fed has become more hawkish (or less Dovish) and the MPC has clearly felt the need to act, even if its actions are unlikely to be as dramatic as those in the USA. The US Federal Reserve indicated that they looked for interest rates to eventually move towards 2.5%. Given the differing demographics and productivity levels in the UK, our long-term neutral interest rate is almost certainly lower, we expect a further rate rise next summer to 0.5%, any further rates rises beyond 2022 will be slow and gradual.

QE programme is now officially reached its target

The one element of monetary policy tightening that has not been focused upon as closely is the BoE’s Quantitative Easing (QE) programme, which as of December reached its goal of GBP 895bn in assets (GBP 875bn in Gilts, GBP 20bn in corporate bonds). QE’s objective has been to keep longer-term bond prices up and hence yields down. In 2022 the absence of a buyer of last resort is going to tell us just how much actual investor appetite there is for Gilts. For a Government which has shown a marked proclivity for spending, being forced to justify the effectiveness of that spending might come as something of a shock.