UK growth risks to the downside and inflation risk to the upside as we go into 2025

The UK goes into 2025 with a relatively difficult macroeconomic backdrop, which we set out in detail in the latest Macro Comment State of the UK economy: Mixed outlook for 2025.

In summary:

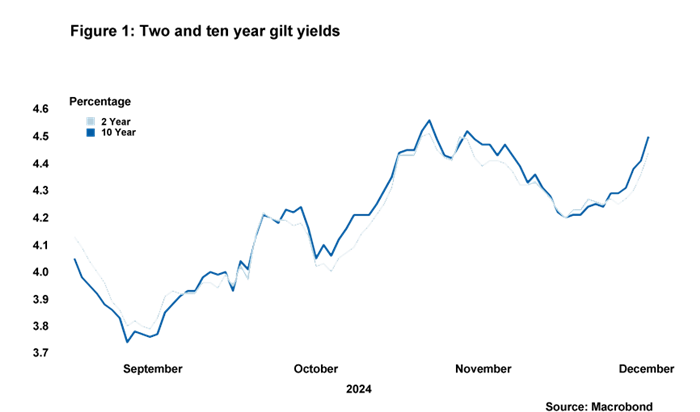

- The UK’s fiscal targets appear to be at risk. Even at the time of the Budget, the Office for Budget Responsibility (OBR) predicted that Chancellor Rachel Reeves only had a 54% chance of meeting them. And since then, developments suggest this likelihood has decreased, with borrowing costs now well above those assumed by the OBR, business sentiment souring following the Budget and the prospect of increased global tariffs.

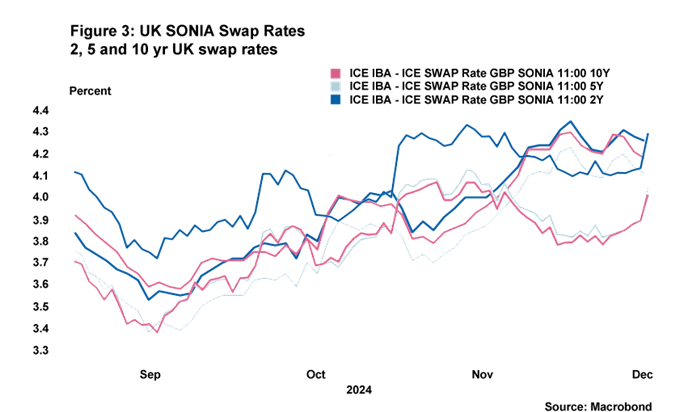

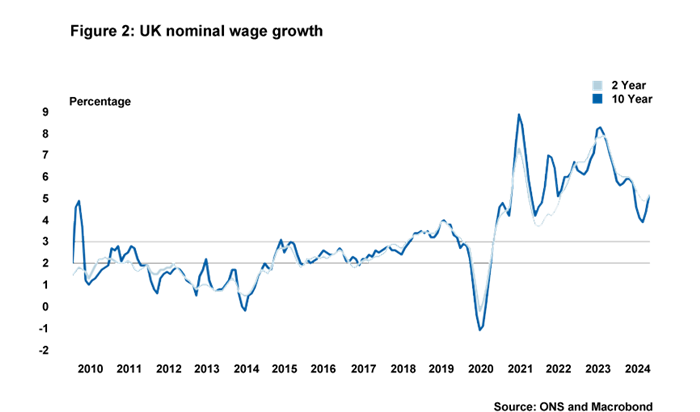

- The Bank of England’s (BoE’s) less sanguine scenarios for inflation – namely that some degree of slack in the economy is required to get inflation down to 2% in the medium term or that structural changes in the UK economy mean inflation will persist for longer and require fewer interest rate cuts – currently appear to be the most likely to play out. Wages and services inflation continue to run hot while the UK’s fiscal policy and potential inflationary spillovers from the US are likely to add inflationary impulses.

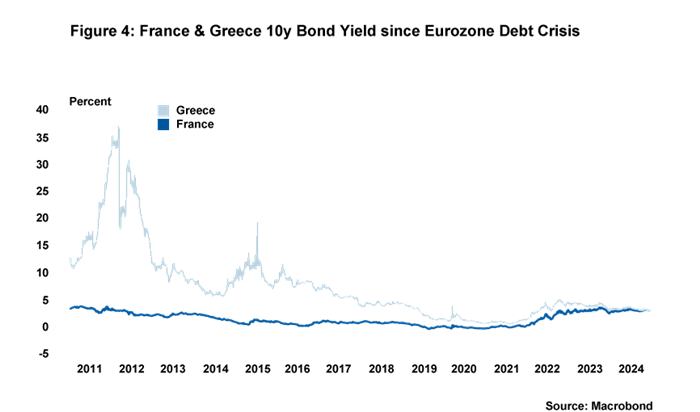

Our relative economic position compares quite favourably to other major European economies, not least due to the relative political stability in the UK, but we judge that UK growth risks are to the downside and inflation risks are to the upside. This is a tricky context for the BoE to be operating in. Worries concerning inflation persistence meant the Monetary Policy Committee held rates in December and, while we should still see the rate cutting cycle continue to proceed in 2025, it will in all likelihood occur at a very cautious pace.

Our full economic and financial forecasts will be published in the next Global Macro Forecast on January 22 2025. Until then, wishing all Rate Wrap readers a Merry Christmas and Happy New Year.

Daniel Mahoney, UK Economist