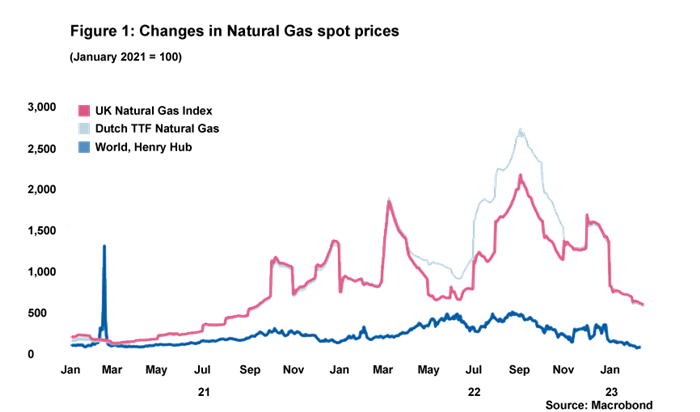

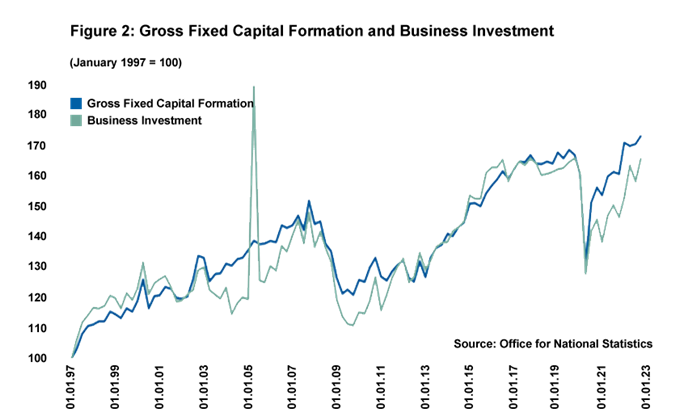

It seems rare these days to read any good economic news, so let us start with some positive developments since the last Handelsbanken Rate Wrap. The Bank of England (BoE) published its latest inflation report earlier in February and the outlook for the UK economy has seen a notable improvement, in large part owing to spot and future energy prices moderating (See Figure 1). Inflation projections are looking far more sanguine with the BoE’s Monetary Policy Committee (MPC) now predicting CPI inflation will be down to just 4% by year end. While a recession remains the base case scenario in 2023, it is expected to be shorter and shallower than previously expected. There was also an unexpected bright spot towards the end of 2022 with business investment seeing strong growth of 4.8% in Q4 (see Figure 2), which helped the UK to avoid a technical recession last year. And the composite PMI index (which measures purchasing managers’ views of business conditions) for February dramatically exceeded expectations by registering well above 50. This indicates economic expansion and could suggest that forecasters are being too downbeat on short-term growth prospects for the UK economy.

Despite some reasons for cautious optimism, the UK economy remains the only G7 nation not to return to its pre-pandemic GDP level and its prospects for 2023 continue to be held back by specific factors, including impacts on trade arising from Brexit, tight fiscal and monetary policy as well as a growth in inactivity levels following covid. Furthermore, it is notable that the strong PMI figures do not account for the retail and construction sectors – which are likely to face strong headwinds – and questions also remain about how sustainable the recent boost to business investment will be. The super-deduction, allowing businesses to cut their tax bill when investing in qualifying new plant and machinery, is due to come to an end in March, while around four fifths of business loans are on floating rate, meaning monetary policy tightening is passing through to companies especially quickly and hitting profitability. Chancellor Jeremy Hunt will have an opportunity to incentivise momentum in business investment at the Budget on 15 March – and he has, indeed, indicated that he will prioritise alleviating tax burdens on businesses – but we have to be mindful that any changes announced are likely to be small in fiscal terms.

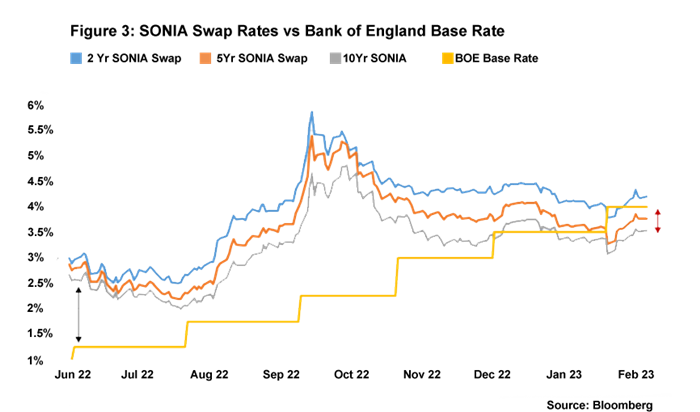

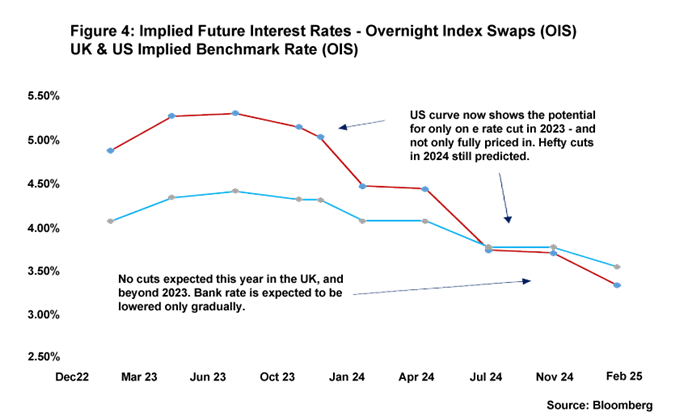

After the Budget, attention will naturally turn to the March MPC meeting the following week. We are clearly coming to the end of the BoE’s interest rate hiking cycle but there remains some uncertainty about where rates will peak. UK inflation is finally firmly on a downward trajectory with CPI falling to 10.1% y-o-y in January, below consensus and down from the previous month’s reading of 10.5%. The BoE will especially welcome this drop in headline rate given it was driven by a 0.5pp fall in the core rate of inflation. Yet at the same time, many MPC members will remain worried about the inflationary impact of nominal wage growth that remains very high in historic terms with, for example, regular pay climbing since early 2022 up to 6.7% y-o-y in the period October to December 2022. The latest unexpectedly robust PMI figures could also push MPC members in a more hawkish direction. The likelihood of rates being increased by 25bp at the March meeting, rather than being held at 4%, has certainly increased, but further data releases in the coming weeks will provide more certainty about whether we are already at peak rates.

Daniel Mahoney, UK Economist