Are rate cuts around the corner?

The Bank of England (BoE) signalled a slight dovish pivot at the Monetary Policy Committee’s (MPC’s) February meeting. While the previous meeting stressed that further tightening in monetary policy might be required if inflationary pressures persisted, the February 2024 inflation report made no such reference and added that “the [monetary policy] committee will keep under review for how long Bank Rate should be maintained at its current level”. Despite this, there are clearly major disagreements within the bank about what the future pathway of monetary policy should look like: the MPC was split three ways on its interest rate decision in February with six members backing a freeze in rates, two arguing for an increase and one for a cut.

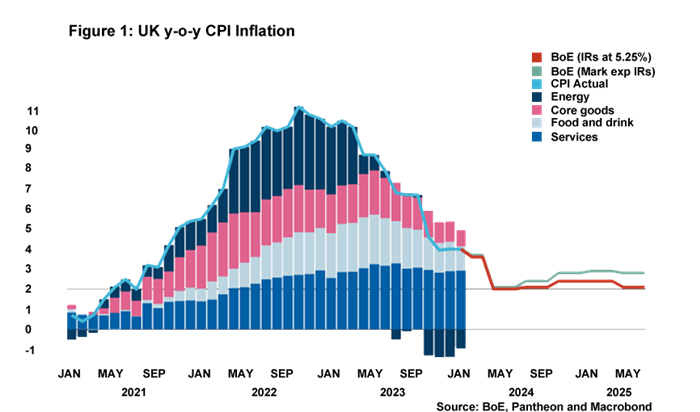

Short-term projections for the inflation outlook have certainly improved quite considerably. Indeed, it is expected that UK CPI inflation will hit 2%, the BoE’s target, in just a few months’ time. However, the medium-term outlook continues to pose a problem for rate-setters: a combination of base effects in the energy component of CPI inflation along with projected sticky services inflation mean that CPI will very likely be above target again by year end. Moreover, UK services inflation and, for that matter, nominal wage growth continues to track above counterparts in the Euro Area.

This of course begs the question as to when we should expect rate cuts to come? Nothing in the current growth figures is expected to have a huge influence. There was a minor technical recession in H2 2023 but positive, albeit muted, growth is to be expected in 2024. Other indicators, including those that the BoE is monitoring especially closely (services inflation, private sector wages and labour market tightness), will be far more consequential to decisions made by members of the MPC this year.

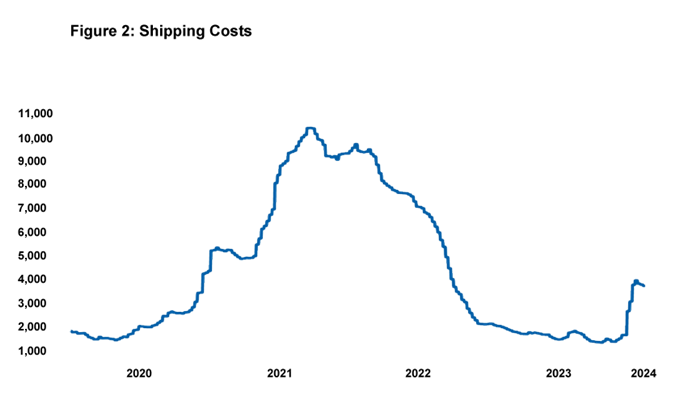

These indicators continue to be giving mixed signals. January’s headline CPI and services inflation print undershot expectations and suggest the disinflation process continues to tick along nicely. Moreover, the inflationary impact arising from conflict in the Middle East remains muted. Shipping costs did see a spike earlier this year but prices have now begun to stabilise and the energy market remains sanguine. However, upside risks to the inflation outlook remain should there be an escalation of conflict and some indicators of domestic inflation remain a worry, not least UK wage numbers that are elevated, exceeded market expectations at the last print, and remain well above levels consistent with meeting 2% inflation in the medium term.

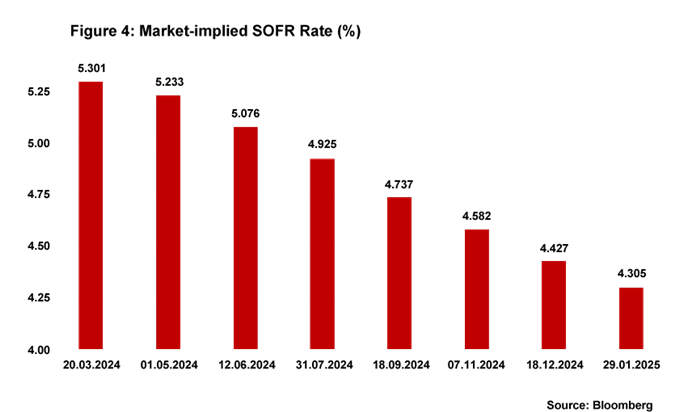

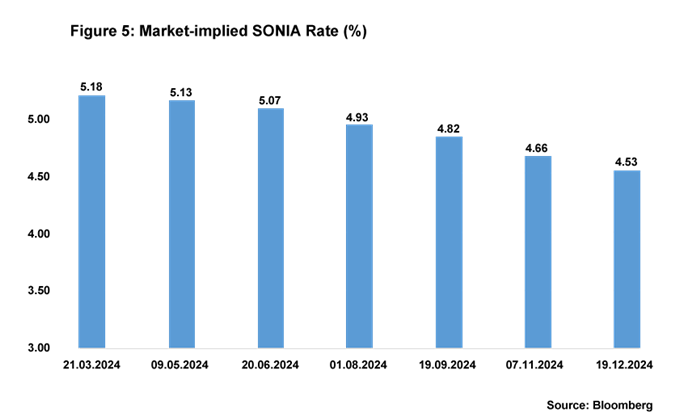

At the beginning of the year, markets priced in a fairly aggressive loosening of monetary policy with predictions of six to seven rate cuts this year. In light of continuing signs of domestically-driven inflationary pressures, we always thought that this was too optimistic and markets have since slashed the number of expected rate cuts. Our view remains that the first rate cut will take place in June this year and that there will be a total of three rates cuts across 2024, in line with current market expectations (as of 16.02).

Daniel Mahoney, UK Economist