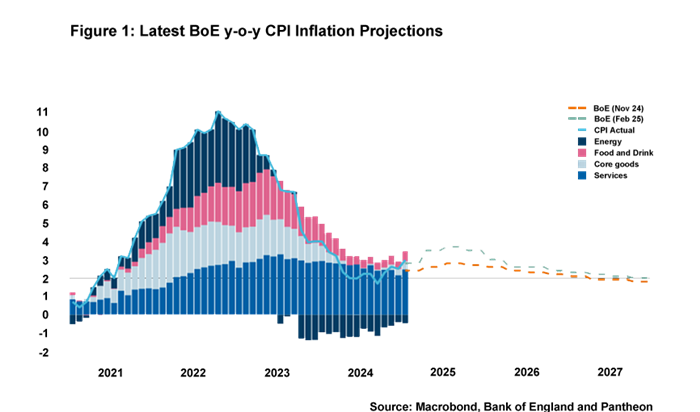

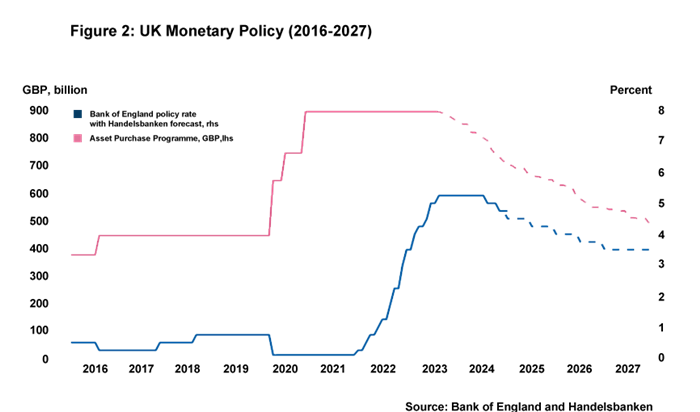

In January’s Rate Wrap, we highlighted the dual prospective challenges of below-trend growth and above-target inflation for the UK economy over the course of 2025. Developments since then very much re-enforce this projection. As widely expected, the Monetary Policy Committee (MPC) cut rates by 0.25pp in February (although Catherine Mann, of course, surprised markets with her pivot from chief hawk to dove by being one of the two members that backed a 0.5pp fall in rates), but the real story from the Bank of England’s (BoE’s) latest Inflation Report is the updated forecasts for growth and inflation.

Starting with the inflation challenge, the BoE’s new forecast in its February report now shows, on the face of it rather surprisingly, that inflation is expected to peak at 3.7% in Q3 of this year, although there is no need to panic just yet. The projection, based on market expectations for interest rates, continues to show that inflation will still return to 2% in the medium term (end of 2027).

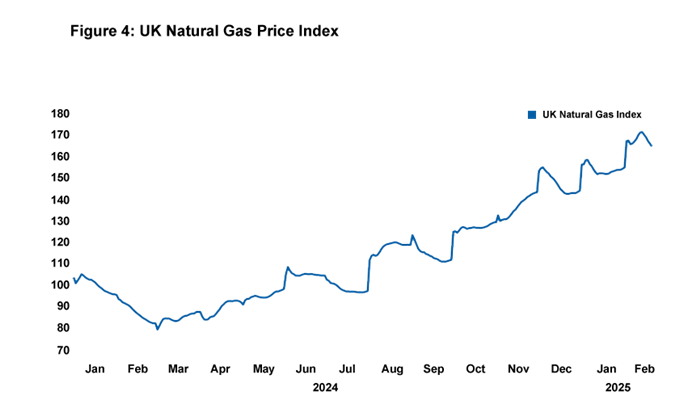

The key drivers of this upcoming spike in inflation will be higher energy prices as well as the growth in other regulated prices. MPC members are currently minded to “look through” this given it will be driven by one-off factors, in essence signalling that elevated headline inflation in the short term will in all likelihood not affect their decisions on interest rate policy. However, should any second-round effects emerge – such as a response in wage demands – this position could shift, especially since existing wage settlements and services inflation continue to be a source of concern.

While the increase in prices during 2025 will be far less severe than the those experienced in 2022, recent volatility in inflation means medium-term expectations of consumers may now be less “anchored” to the 2% inflation target than was the case in the two decades prior to the pandemic. Does this mean inflation persistence is more of a risk, especially if there is an additional supply shock this year from, say, escalatory tariffs? And, in general, are second-round effects now more likely to occur when one-off factors increase inflation? It is certainly plausible and something to keep an eye on (see our latest Macro Comment Opens in a new window).

Turning to the growth challenge, the recent souring of consumer and business sentiment is now being reflected in the BoE’s growth forecasts. Its forecast for 2025, for example, have been slashed in half from 1.5% to just 0.75%. The Office for Budget Responsibility (OBR) will no doubt follow suit and downgrade its near-term forecasts for the UK economy while raising its projections for government borrowing costs. A recent leak from the OBR to Bloomberg has confirmed what many of us have suspected for some time, which is that Chancellor Rachel Reeves’ fiscal target of achieving a current surplus within five years is now at risk and will probably mean that further fiscal consolidation is set to be announced at the March statement.

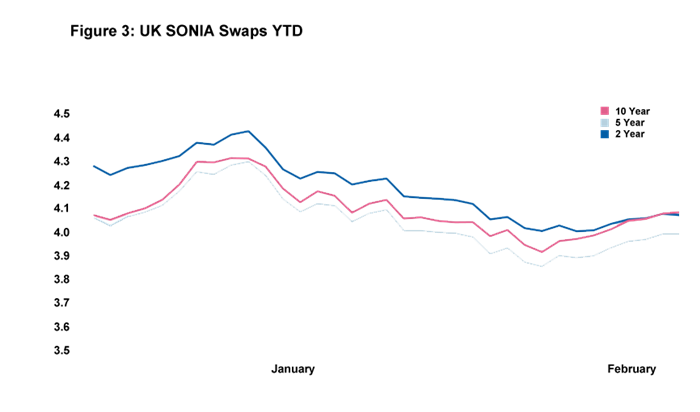

A key question with respect to the current weak growth that the UK is experiencing, is what exactly is driving it? Is it being driven by suppressed demand, which would allow for a reasonable loosening of monetary policy, or is it being prompted by constrained supply that requires interest rates to remain higher for longer? Minutes of the MPC meeting suggest that the seven members backing a 0.25pp cut to rates are split on this question. The reason why this is so important is that it highlights a large degree of uncertainty about the trajectory of base rate both this year and next year. However, while uncertainty about future interest rates is certainly material, our base case scenario remains for a gradual cutting cycle down to 3.5% in 2027 as the BoE balance indicators suggesting inflation persistence with weakness in growth that may suggest disinflationary forces are ahead.

Daniel Mahoney, UK Economist