Inflation overshoots expectations again

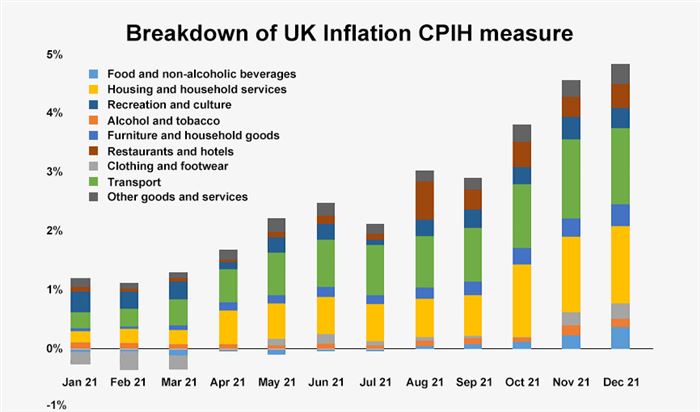

Prices continue to climb for British consumers with the headline inflation rate (CPI) hitting 5.4% for December 2021 – its highest level since March 1992. This came in above market expectations and well in excess of what the Bank of England (BoE) was projecting just a few months ago. For example, the August Monetary Policy report forecast a peak of around 4% this Spring. The measure of inflation which includes housing costs (CPIH), has also increased, now standing at 4.8% for December 2021 (year on year) compared to 4.6% for November 2021.

Meantime, energy prices continue to be a major driver of inflation – 12-month inflation rates in October 2021 were a whopping 18.8% for electricity and 28.1% for gas – but latest figures show other factors are also at play. Indeed, food inflation has shot up (4.2% from 2.5%), core goods inflation is on the rise (5.2% from 4.8%) and services inflation increased to 3.4%, which is its highest rate since June 2013. Inflation is proving to be much more stubborn than the BoE initially anticipated, and although there remains a consensus that recent price spikes are “transitory”, the increasingly broad drivers of inflation suggest that a rapid reversal to the target rate of 2% will be difficult, something which will no doubt be playing on the minds of policymakers.

Moderate tightening will continue

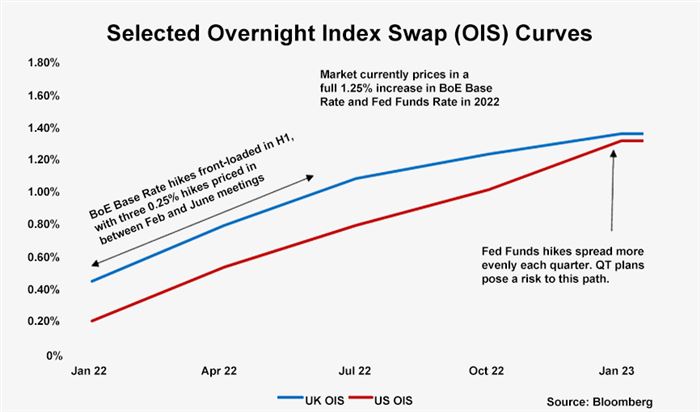

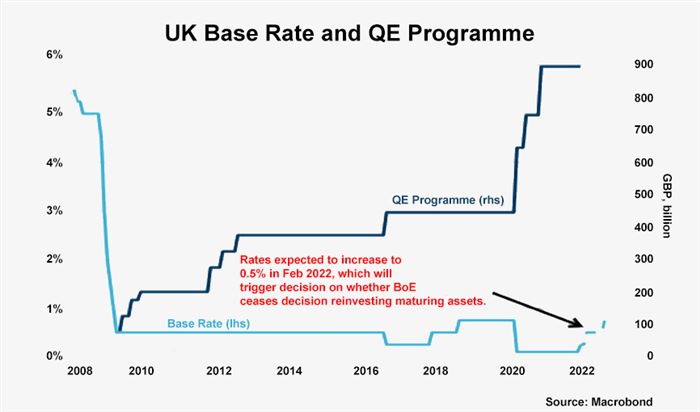

There is thankfully no evidence yet of a wage-price spiral (latest earnings data shows the rate of pay growth has fallen quite significantly), but the severity of current inflation will mean the BoE needs to act to reduce the likelihood of such a scenario. Monetary policy over the course of 2022 is likely therefore to continue tightening, albeit moderately. We are expecting earlier interest rate rises this year – one in February and one in August – that would take the base rate up to 0.75%. The quantitative easing (QE) programme reached its £895bn target level of purchases, at the end of last year, and we do not believe there is the prospect of further asset purchases. Indeed, the BoE’s current guidance suggests that it should begin to unwind QE, that is reduce its stock of asset purchases, by not reinvesting maturing assets once the Bank Rate hits 0.5%, which we expect to happen in February. This is not, of course, unconditional guidance – it will only happen “if appropriate given the economic circumstances”. Given the economic hit arising from the Omicron Covid variant, it seems likely that the BoE will proceed cautiously with any quantitative tightening in the near future.

The upcoming squeeze

GDP figures for November 2021 brought welcome news that the UK economy had passed its pre-pandemic level, and the government’s recent announcement that it will remove Plan B restrictions later in January bodes well for the economy overall. However, that is not to say that the coming months will be plain sailing. The latest GDP figures do not factor in the impact of Omicron and there is also an upcoming squeeze on living standards that will act as a brake on economic growth. Without any changes to government policy, consumers will be hit by a double whammy in April 2022: tax rises – including the increase in national insurance – will impact aggregate incomes by as much as £15bn per year, and the re-rating of the energy price cap for residential consumers could lift energy prices by around 40%. Markets are waiting to see whether the government makes any announcements in the coming weeks that might dampen some of these rises to the cost of living.

Daniel Mahoney, UK Economist