2023 still looking like a tough year for the UK economy

Monthly GDP figures for November were unexpectedly in positive territory, leading to a strong possibility that the UK narrowly avoided recession at the end of 2022. However, while such an eventuality may lead to some temporarily positive news headlines, it would only show the UK economy flatlining, and fundamentals arising from the high inflation and rising interest rate environment mean the central case for 2023 remains for the UK to enter into a period of economic contraction, albeit a shallow one.

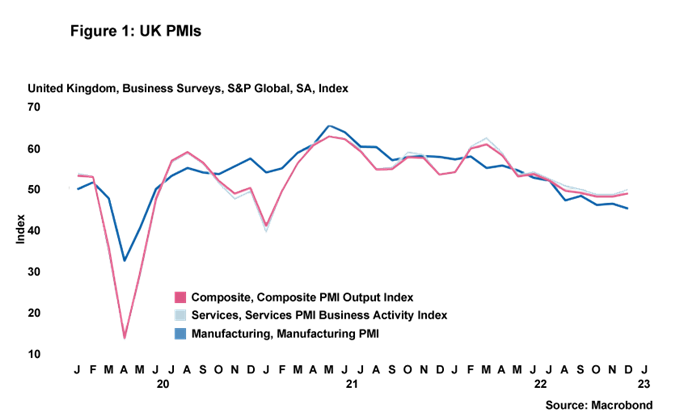

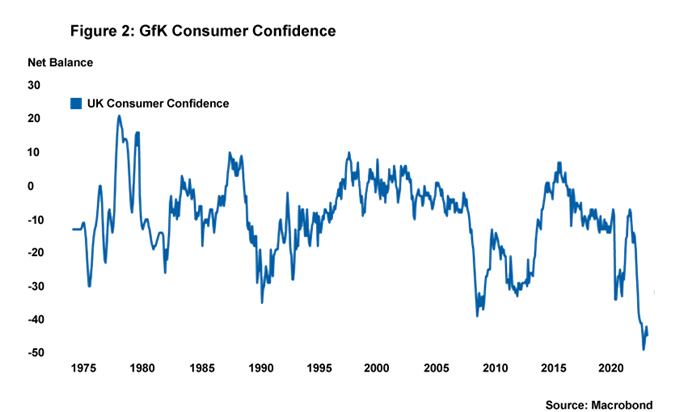

UK households have been much less willing to use the excess savings accumulated during the pandemic compared to households in many other developed economies, and there is every reason to suggest that UK consumers will remain cautious over 2023. Over 1.4 million households’ fixed-rate mortgages will end this year, leading to a huge squeeze on the disposable income of those affected, while recent readings for consumer confidence and retail sales by volume have registered well below expectations. Many businesses may start tapping into their savings but this will often be simply to cope with higher interest payments: around three quarters of business loans are floating rate, making it pressing for many corporations to prioritise debt repayment. This, of course, does not bode well for any prospects of a resurgence in business investment in 2023, especially as the composite PMI is already registering below 50 (which indicates contraction). It is notable that both household and business indicators continue to suggest the economic outlook for this year remains very challenging (see Figures 1 and 2) .

The Bank of England’s (BoE’s) Monetary Policy Committee (MPC) will meet for the first time this year on 2 February. Rate-setters will be pleased to see that y-o-y headline CPI inflation has now fallen in two consecutive months, dropping from its peak of 11.1% in October to 10.5% in December. However, the core inflation print – which remained at 6.3% in December – will maintain pressure on the MPC to act, especially as nominal wages continue to register high readings despite there being tentative signs of labour market loosening. Annual average pay awards for September to November 2022 came in at 6.4%, up 0.2pp from the previous month, with more timely PAYE data suggesting the figure is above 7%. While still representing significant falls in real terms, these levels of nominal pay would not be consistent with the BoE meeting its 2% inflation target. There also remains a major discrepancy between yearly pay increases of the private and public sector, which have risen by 7.2% and 3.3% respectively for September to November. Public sector pay awards are likely to increase further, and continuing strong growth in broader nominal wages means that core inflation, especially the services component of it, will probably remain stubborn over the course of 2023. In light of this backdrop, we maintain our view that the MPC will likely increase interest rates by 50bp to 4% in February in order to address potential domestically-led inflationary pressures.

Source: Macrobond

Daniel Mahoney, UK Economist