BoE likely to remain cautious in February

Consumer UK retail spending was surprisingly depressed in December, down 2.4% on the year even though expectations were for a modest rise in sales. GDP growth in Q3 2023 registered at -0.1% and it was finely-balanced as to whether Q4 would post negative growth. December’s retail sales print would imply that Q4 may have seen a contraction, which would put the UK in a technical recession (two consecutive quarters of negative growth). While this would no doubt prompt headlines across the news bulletins, the recession would be very shallow and it is important to stress that economic activity is bound to pick up in 2024 as real wages continue to grow.

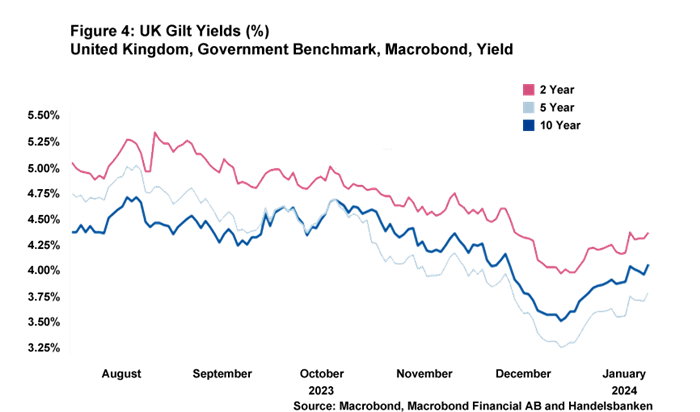

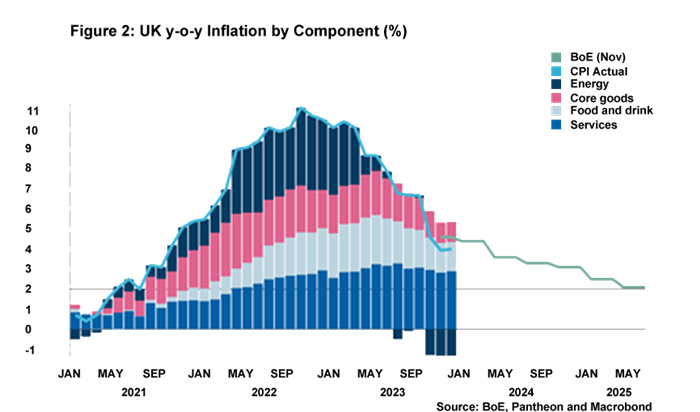

Looking ahead, the Bank of England Monetary Policy Committee (MPC) meeting on 1 February will, of course, be closely-watched by market participants keen to get a steer on the pathway of monetary policy in 2024. There is plenty of data for members of the committee to chew over, much of which will be welcomed by the BoE. For example, there seems to be a sustained cooling in nominal wages: regular pay has come down from 7.9% in August to 6.6% in November. It is notable that these earnings numbers are not affected by data quantity problems in the Labour Force Survey. Moreover, December’s inflation registered at 4%, which is quite some way below the BoE’s November forecast.

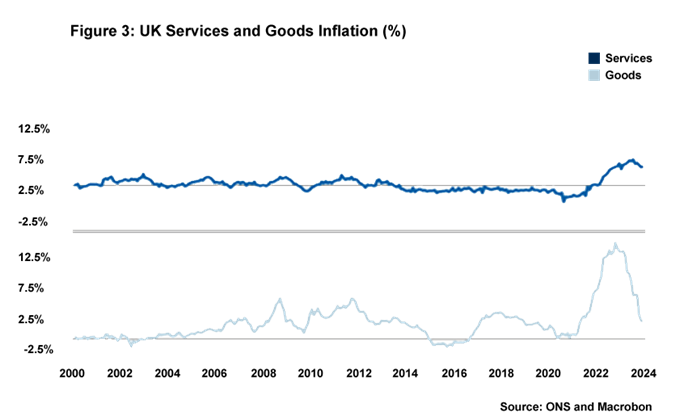

However, the financial market reaction to December’s inflation print highlights that a large level of uncertainty remains. A relatively minor overshooting of the print above market expectations led to traders slashing the number of predicted interest rate cuts in 2024 from five to four. Moreover, while indications suggest that inflation will continue to come down from its current level of 4%, getting to 2% inflation on a sustained basis remains a challenge. Catherine Mann, one of the more hawkish MPC members, notes that goods inflation needs to be -1% and services around 3% if the configuration between goods and services were to return to where it was in the last 20 years. Yet current goods inflation is circa 2% and services inflation is circa 6% (see Figure 3). And, of course, geopolitical turmoil also presents upside risks to the inflation outlook via channels including the energy market, shipping costs and supply chain disruption. All of this will serve to make the BoE cautious.

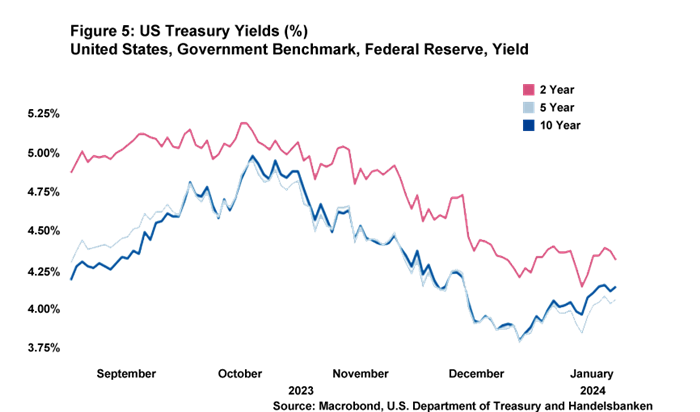

The US Federal Reserve has already explicitly set out its view that interest rate cuts are on the horizon yet there remains enough uncertainty to stop the BoE following suit at its February meeting. However, the downward trajectory of nominal wages and UK inflation registering below the BoE’s expectations could lead the MPC to moderate its hawkish language at the February meeting. Handelsbanken’s current house view is that rate cuts will begin in June, and that there will be a total of three 0.25pp rate cuts in 2024.

For more on Handelsbanken’s economic outlook for 2024, please see our latest Global Macro Forecast Opens in a new window.

Daniel Mahoney, UK Economist