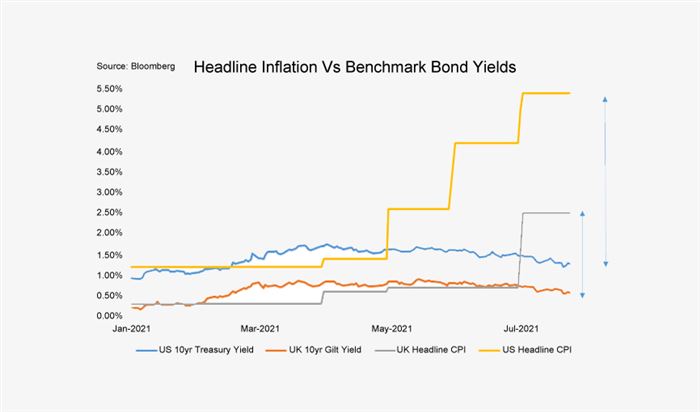

US headline and core inflation running at 5.4% and 4.5%, UK figures running at 2.5% and 2.3%, yet we have benchmark 10-year bond yields at 1.3% and 0.6% - make sense?

Technicalities aside, the rates market does seem out of line with the macro fundamentals of accelerating inflation, strong economic recoveries and increasing consumer confidence. Whilst data is not surprising to the upside as much, they remain at healthy levels, but the rates market is barely reacting. In fact a bout of souring risk appetite early last week on growing case numbers of the Delta variant sent the US 10-year yield to multi-month lows of 1.13% before reversing soon after. The theme for July’s Rate Wrap of “curve flattening” has continued, but rather than short-term rates rising, it’s been long-term rates falling relative to those of shorter tenors. This creates an interesting setting as we head into the autumn which may be a difficult one for the Federal Reserve to navigate.

No one can really pinpoint the dominant reason for the fall in yields we have seen over the summer. Some note buying from pension funds and foreign parties, others like JP Morgan point to a lack of liquidity as potentially the prime reason exacerbating the moves, whilst another key factor is a reversal in positioning: it is widely discussed that every man and their dog were selling bonds following the spike in yields in Q1, and many holding those positions would likely have accumulated losses as yields have fallen back, causing them to have to close out the position. How do you close a short bond position? You buy the bond, lowering yields – this can create a vicious cycle.

More recently though as alluded to above, we believe concerns around the Delta variant have grown which seemed to spook markets briefly last week, with equities, commodities and “risk” currencies selling off, whilst haven assets like US Treasuries rallied. Granted a valid concern, but the fact that the trend in hospitalisations/deaths to cases looks to have broken in developed nations where a significant proportion of the population is vaccinated (according to Our World in Data), this should not dampen the market’s mood for too long, in fact you can argue its already behind them.

From the Fed’s point of view, it’s arguably a market that seemingly does not believe in their mandate of average inflation targeting, which allows for periods of higher inflation to compensate for periods of below-target inflation. The hawkish commentary from the June meeting may have contributed to this lack of conviction as the Fed brought forward the timeframe for an increase in interest rates. If interest rates increase quicker than previously thought, then this could dampen longer-term inflation expectations and therefore interest rates. This may well throw a spanner in the works when it comes to the tapering of asset purchases with a formal announcement expected potentially as early as late August – I think the Fed would firstly like rates to be at a higher level, and would rather be seeing market rates rising gradually so their reduced purchases do not cause a fallout and a swift tightening of financial conditions, but rates are not moving!

Some big decisions need to be made by the voting members in the coming months, how transient is inflation? How can we avoid another bond market fallout like in 2013 that stalls growth prospects – oh to be a central banker eh?

Lower for longer in Frankfurt

A quick note on the latest decision from the European Central Bank too. Following the completion of its strategy review, the bank amended its inflation target from “below, but close to 2%” to a more symmetric 2% target. On its completion President Lagarde mentioned there would be a tweak to forward guidance in the central bank’s next statement at the July 22nd meeting. As we saw it, this created some noise around the meeting, such as whether any hints would be provided on future quantitative easing plans, stronger language in its commitment to the new target, and whether they might define what they see as the “end” of the coronavirus crisis, but ultimately nothing material changed. The new inflation target was incorporated into the statement and that was about it!

Asset purchases will continue to be front-loaded and the statement avoided all talk of plans regarding purchases heading into next year (the “emergency” PEPP programme is due to end in March 2022). The guidance around interest rates correlates more strongly to the inflation outlook, stating that rates will remain at lower levels until they see inflation reach 2% “well ahead” of their end projection rather than “within” their end projection – which basically means there is now a higher bar to raise rates.

The ECB remains one of the most dovish in the G10, and therefore we may see a growing divergence in rates between the bloc and that of the US and UK. Some in the market however clearly thought the statement wasn’t dovish enough as judged by rising eurozone yields post-announcement, albeit temporary.

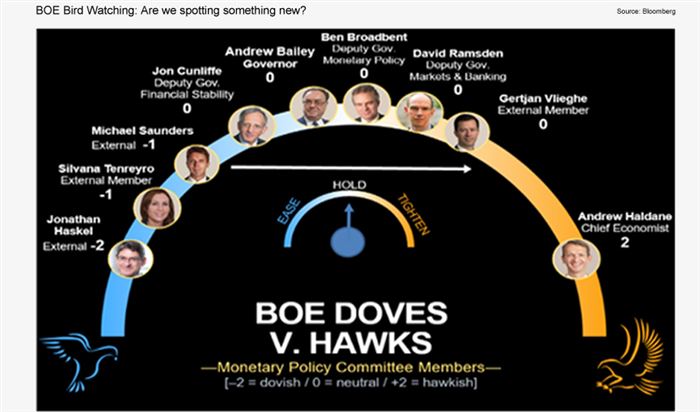

Central bank evolution: Doves to hawks

We have seen some more comments from members of the Bank of England Monetary Policy Committee on both ends of the spectrum in regards to views on the next policy move. It started with Dave Ramsden and Michael Saunders who both may have surprised markets with their more optimistic view on the UK recovery. The former noted that he could envisage the conditions for considering tightening being met “somewhat sooner than previously thought”, whilst the latter questioned whether asset purchases should be withdrawn “in the next month or two”. We believe the comments from Mr. Saunders are key given that he is normally considered a dove, and only a few months ago was open to the idea of negative rates in the UK whilst also dissenting in the early stages of the pandemic, calling for additional QE against the consensus.

He, along with outgoing member Gertjan Vlieghe, have seemingly evolved into the hawks of the committee, taking over the helm from former chief economist, Andy Haldane. This now makes the August meeting a rather interesting prospect. Whilst the view of Dr. Vlieghe carries less weight, a dissent from Mr. Saunders (perhaps voting to end the purchase of assets early by reducing the QE envelope by £50bn) would be an important development – many analysts have noted that Saunders has led shifts in stance of the committee before. Could we see a repeat in the coming months?

An imminent shift seems unlikely, with virus cases increasing at a decent pace and the so-called “pingdemic” causing 700,000 to self-isolate in just one week, according to the NHS App, the recovery is likely to slow throughout Q3. This should only be temporary, so will likely only delay any plans of policy tightening rather than derail them. Indeed, evidence of this was seen in the cautious words of dove Jonathan Haskel last week in a speech to Liverpool University where he stated that “tight policy is not the right policy” at this point in time. This was followed shortly after by comments from incoming MPC member Catherine Mann when testifying to the Treasury Select Committee where she warned against any premature tightening of policy.

All in all, given the presence of the Delta variant and continued confidence from the likes of Ms Mann, Ben Broadbent and Governor Bailey that inflation will not spiral in the coming months, we can probably expect a more balanced Bank of England in the coming meetings, which would perhaps prefer to sit on the side lines and wait on more data and on what the Federal Reserve decides to do with its own QE programme. I would expect the BoE to move at the same pace, rather than front run the Fed given the potentially similar nature of the respective recoveries. This differs from some G10 peers who are having to bite the bullet. House price inflation in New Zealand, Norway and Canada is forcing their central banks’ hands to tighten earlier (likely next month for the Reserve Bank of New Zealand) given that it plays a bigger role within their mandate. However the extent of such pressures are not as strong in the UK, and house price growth should moderate (not decline) come the end of the partial stamp duty holiday in the autumn.

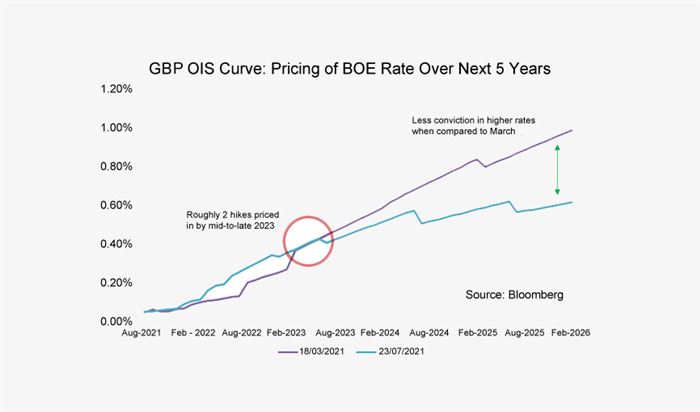

Markets have scaled back rate hike expectations in line with the risk-off tone and growing demand for bonds as a result. Expectations as evidenced by the OIS (Overnight Index Swap) curve show the market is positioned for still roughly two hikes by late 2023, although there is less conviction in rate hikes further down the line. The chart below shows the difference in the curve when compared to aftermath of the March BoE meeting.

Attractive environment persists

Hedging via fixed-rate loans or derivatives both look even more attractive than they did a month ago. Despite some whipsawing from the contrasting view of MPC members, they have recently mirrored the move lower in US rates. 10-year interbank base rate swaps trade at 0.61%, 5-years at 0.46% - roughly 20 and 10 basis points off year-to-date highs.

Despite the summer lull, interest in hedging remains strong with plenty of conversations ongoing with our customers, debating the market setting and outlining various scenarios that may arise. Each conversation is different and unique in circumstance, and the flexibility of our offering helps provide one or multiple options that can fit in with those individual strategies. Please get in touch with your local branch to find out more about what is available.

James will be back next month with his insights on the UK recovery and the August BoE meeting, whilst we will also cover what’s going on at the Fed in the build up to the highly anticipated Jackson Hole Symposium.

Cameron Willard, Capital Markets

All figures in this commentary, unless stated, are sourced from Bloomberg as of 29/07/2021