On Tuesday, July 19, Bank of England (BoE) Governor Andrew Bailey addressed guests at London’s Mansion House with a speech entitled, “Bringing inflation back to the 2% target, no ifs no buts”. The message was clear: he stressed that the BoE now sees “the balance of risks to inflation as on the upside,” and that any signs of greater persistence of inflation would lead the Bank to act forcefully. Crucially, he explicitly stated that a 50bps increase in interest rates will be among the options for the Monetary Policy Committee (MPC) at its next meeting in August.

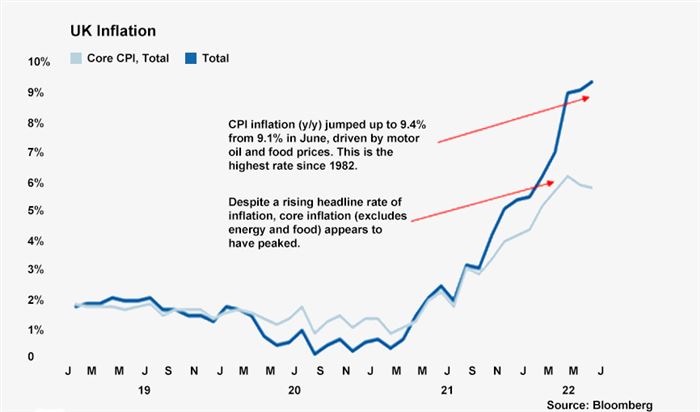

Handelsbanken UK Economics were initially expecting a further two 25bps hikes from the BoE this year. However, we have revised our forecast upwards. Many other central banks are increasing the size of interest rate hikes. For example, at their last meetings the Federal Reserve, and Bank of Canada raised rates by 75bps and 100bps respectively. Moreover, the European Central Bank (ECB) unexpectedly hiked rates by 50bps at its latest meeting. The BoE will be very conscious of the impact this will have on Sterling’s exchange rate, especially at a time when the trade deficit is so high. June’s CPI inflation print of 9.4% – up 0.3pp from May and slightly higher than market expectations – will also no doubt weigh on the minds of MPC members. We therefore now believe that the BoE will increase interest rates by 50bps up to 1.75% in August. This would be a very significant move by the MPC: the BoE has never increased rates by 50bps since it became independent in 1997. We still expect a further 25bps rise later in the year, which would leave bank rate at 2% year end.

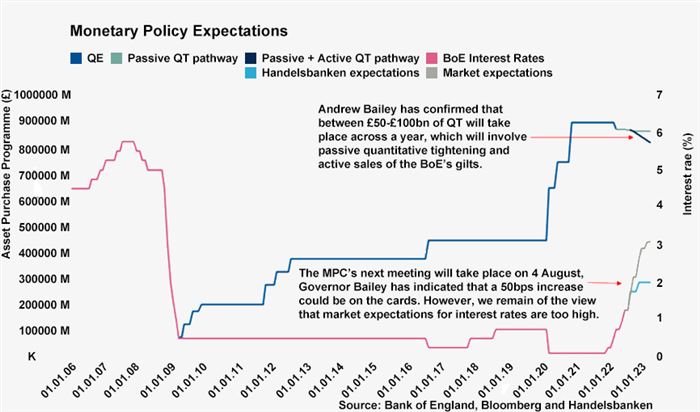

Market expectations continue to price in additional aggressive hikes in BoE interest rates over the course of this year, predicting that bank rate will settle at around 3% by the start of 2023. We continue to feel that market expectations are too high. Governor Andrew Bailey has now confirmed that between £50–100bn of quantitative tightening will be pursued over the first year, which will require active sales of gilts in the BoE’s Asset Purchase Programme. This will act as a deflationary force and there are also some optimistic signs that other factors will bear down on inflationary pressures over the short to medium term: the global supply chain index is down 45% between December 2021 and June 2022; shipping rates have fallen around 30% since the start of this year, according to the Drewry World Container index; commodity prices have seen a dip in recent weeks; and inactivity levels are showing a welcome downward trend, which will help to alleviate labour market pressures. And despite an unexpected 50bps rate hike in July, the ECB’s constrained ability to raise interest rates due to concerns around peripheral Euro economy debt markets will also ease pressure on the BoE to increase rates aggressively following the August meeting.