June’s CPI print provides welcome relief to the MPC

As 2023 progressed, a certain level of doom-loop psychology had begun to take hold in the minds of many market participants when it came to judging the UK economy. The UK’s y-o-y CPI inflation rate overshot market expectations in every month from February to May, leading to interest rate expectations creeping up and up: on 1 March, expectations were for rates to peak at 4.75% but four months later this had jumped to well over 6% as concerns grew over inflationary pressures. The MPC was sufficiently concerned about UK CPI and other data that it unexpectedly increased rates by 50bp up to 5% at its June meeting.

July needed to bring some good economic data for the Bank of England (BoE) to ease its interest rate hiking cycle. Labour market figures published on 11 July brought mixed news for the MPC. Annualised figures for nominal wage growth showed earnings of nearly 7%, both above expectations and at levels not compatible with a 2% inflation target, but the release did bring some encouraging signs of the labour market loosening. For example, both vacancies and inactivity levels saw a drop and the unemployment rate ticked up to 4%, which indicated that domestically-generated inflation from wage growth could begin to ease in the coming months.

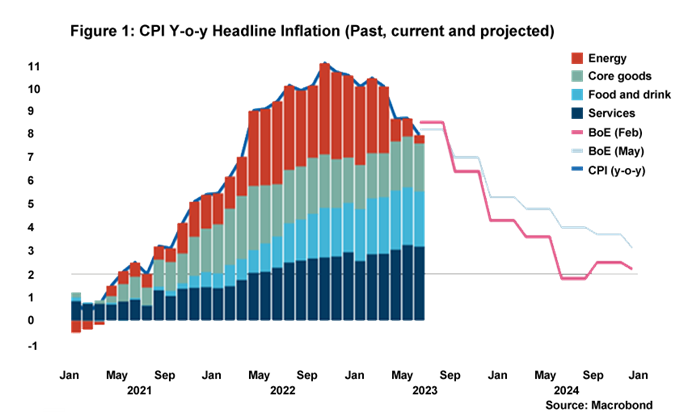

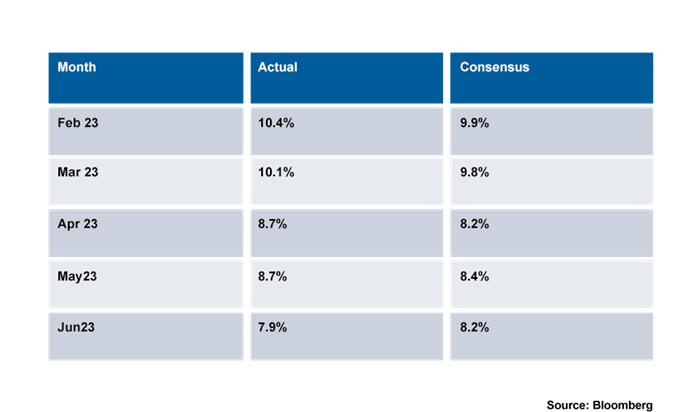

However, June’s CPI print, published on 19 July, was unequivocally good news for rate setters. June's y-o-y CPI reading registered at 7.9%, a marked drop from May's equivalent reading of 8.7% and significantly below market expectations of 8.2%. Granted, a fall in motor fuel prices led to the largest downward contribution to the drop in CPI but it is particularly encouraging that core CPI is showing signs of easing, too. Core CPI rose by 6.9% in the 12 months to June, down from 7.1% in May. The annual rates of both goods and services slowed.

What’s more is that UK inflation will see another significant drop in July as the 17% fall in household unit energy prices shows up in the figures, which will leave y-o-y CPI inflation sub-7%. Other factors such as the fall in shipping costs and supply chain disruption should naturally help push headline rate to between 4 and 5% by year end although prices in the services sector, which are highly influenced by wage costs, could make returning to the 2% inflation target in the medium term challenging.

The big controversy, of course, is all of the questions around the speed at which monetary policy is transmitting into the economy, and how this should affect interest rate decisions for the remainder of 2023. We are often reminded that monetary policy works with “long and variable lags” and those lags are likely to be both longer and, potentially, more variable than in the past given the growth of fixed-rate mortgages over the previous decade. The BoE will be publishing work on monetary policy transmission in due course.

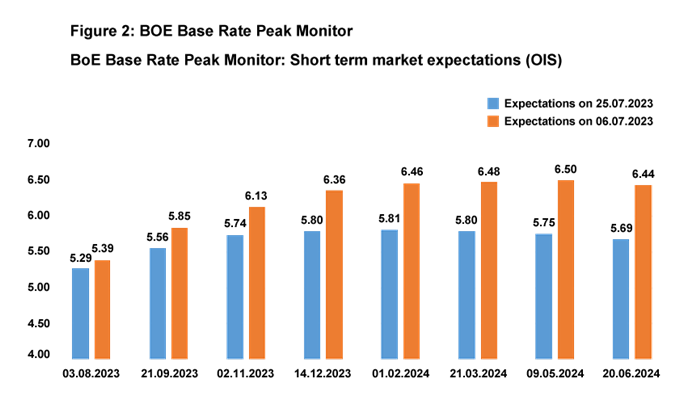

For now, it is clear that June’s inflation print gives the MPC a clear green light to slow its hiking cycle. A 25bp hike at the August meeting is now likely, followed by a further 25bp at the September meeting. We think the BoE will cease its hiking cycle at that point while markets continue to price in one further increase up to 5.75%.

Source: Macrobond

Note: Data comes from Pantheon and the Bank of England

Daniel Mahoney, UK Economist