July saw a spotlight on the fiscal sustainability of government debt. We project that term premia associated with UK gilts are likely to be sustained, or could even grow, as this decade progresses. And while a base rate cut seems likely in August, expect only a modest and cautious continuation of the cutting cycle following this point.

This month’s Rate Wrap will focus on two themes: first, an examination of how financial markets are pricing risk associated with sovereign debt markets; second, the latest short-term outlook for base rate pathway in the UK.

Concerns relating to fiscal sustainability of UK government debt came to the fore in early July when speculation gathered that Rachel Reeves’ position as Chancellor of the Exchequer could be at risk. This speculation was, of course, triggered by a perception at Prime Minister’s Questions that Keir Starmer may not have been fully behind his chancellor. Markets took fright at this prospect due to the interpretation that this may mean the UK’s fiscal rules could be on the chopping block: it is notable that the 30-year gilt yield jumped by 20 basis points at one point on 2 July.

The gilt market did eventually settle when Keir Starmer gave overt backing to his chancellor, although the long end remains under significant pressure. And, while the certainty associated with Ms Reeves staying in place has certainly been welcomed, it is important to stress that financial markets have been increasingly expressing concerns about fiscal sustainability of government debt in the UK and across the western world for some time now. Since 2023, for example, there has been growing “term premia” for sovereign debt markets – in essence, an increasing premium associated with the risks of lending long versus short. The term premium is not directly observable, but a decent proxy for this is comparing 30-year government bond yields to 10-year government bond yields. As you can see from Figure 1, this proxy for term premia has been on an upward trajectory right across G7 economies over the past two and a half years.

In our recent Macro Comment Are financial markets fully pricing in fiscal sustainability? Opens in a new window, we make a call that the current term premia on UK gilts will be sustained, or could even increase, as the decade progresses. This is because the new political context in the UK – exemplified by the recent climbdown on welfare reform and the government’s poor opinion poll ratings – will make it difficult for policymakers to implement measures that alter the long-term trajectory of sovereign debt onto a more sustainable basis. The next pinch-point with respect to this will be the autumn budget, where it is estimated that Chancellor Reeves will need to find between £15–25bn to continue meeting her fiscal targets.

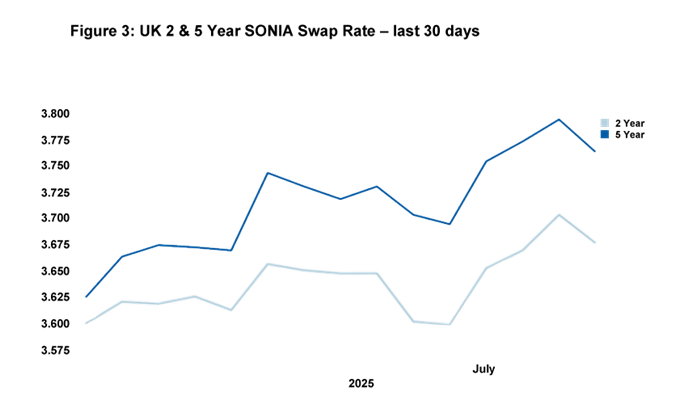

Turning to shorter-term macroeconomic matters, the next Monetary Policy Committee decision on base rate will take place on 7 August. Continuing signs of a loosening labour market certainly point in a dovish direction for this meeting: for example, the unemployment rate ticked up to 4.7% in May and the number of people in payrolled employment fell by 41,000 in June. Payrolled employment has been on a downward trajectory since October 2024, coinciding with the announcement of increases to employers’ National Insurance Contributions. However, despite this, inflation persistence continues in the background of the UK economy: the latest print for headline inflation registered 0.2pp above expectations at 3.6%; services inflation remains elevated at 4.7%; and, as highlighted in the previous Rate Wrap, y-o-y CPI is expected to be north of 3% until at least April 2026, which ostensibly sets the scene for a difficult environment to cut rates.

The clear signs of further loosening in the labour market and cooling pay growth lead financial markets, as of 22.07, to price a roughly 90% chance that a majority of MPC members will end up backing a rate cut in August. We would agree that an August rate cut remains a likely outcome, especially since base rate will still be in restrictive territory even if it dropped from 4.25% to 4%. However, from August onwards we continue to expect only a modest and cautious continuation of the rate cutting cycle given that inflation persistence remains a serious concern for policymakers.

Daniel Mahoney, UK Economist