Monetary Policy Committee raised rates in line with expectations

The Bank of England’s Monetary Policy Committee (MPC) raised rates by 25bp to 1.25% on June 16, in line with economists' expectations but below what many market participants had been expecting. The vote was split 6-3, with Governor Andrew Bailey voting for a 25bp hike.

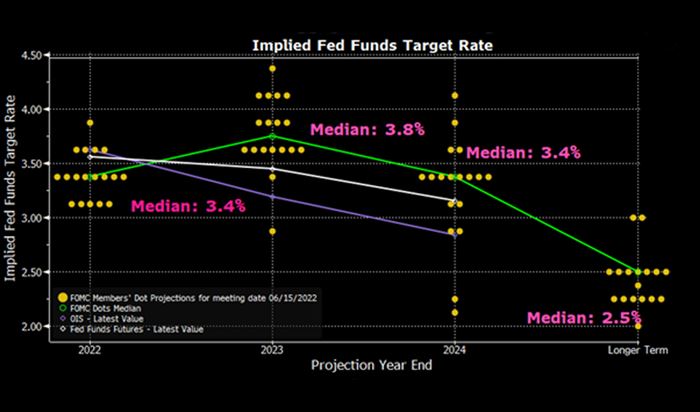

Looking forward, at Handelsbanken we have raised our forecast for the ultimate rate from 1.5% to 1.75%, and that at the peak the BoE will end its hiking cycle. Our forecast remains in the lower half of economists’ expectations, which range from between 0.75 and 3%. Economists’ expectations have been generally below market consensus of 2% or more, markets being focused on inflation continuing well above target, while economists focusing on that, plus the steadily worsening GDP outlook. The MPC appears to continue to believe that inflation pressures are to a significance degree transitory and it’s happy to see sterling taking much of the interim pain.

UK likely to avoid recession, but only just

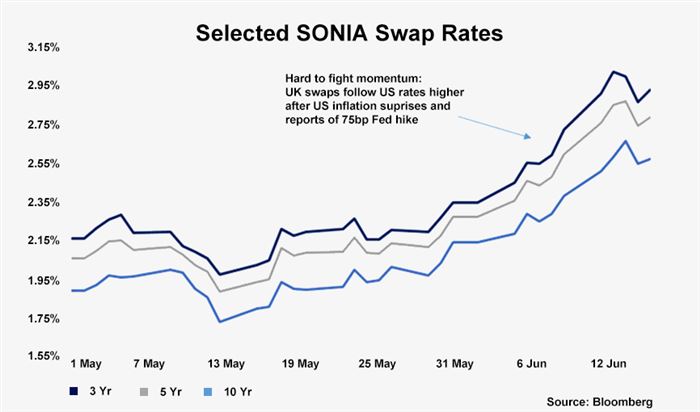

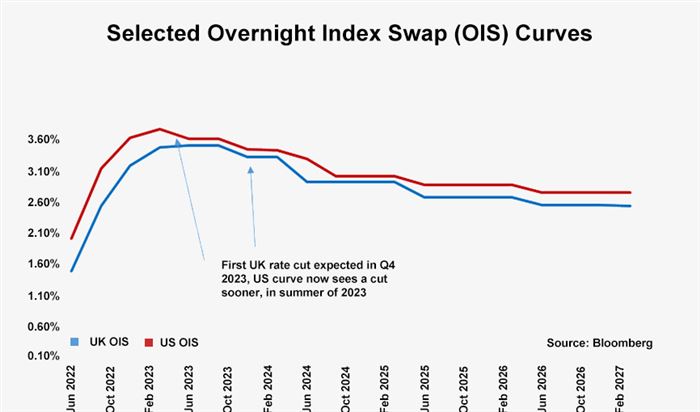

The Bank of England will as always be looking to implement what it sees as the optimum monetary policy for the UK, while being cognisant of the actions of other key central banks. The 75bp US Federal Reserve move on 15 June, and the implications from US Fed Governor Powell that more is on the way, have clearly set the pace. Meanwhile, the European Central Bank in its emergency meeting on June 15 was looking for ways to tighten monetary policy, both to increase rates as well as to begin a programme of Quantitative Tightening. It also has to provide necessary support to prevent undue “fragmentation”, that is undue market pressure on weaker economies which often are carrying high debt burdens. For the moment the ECB has said it plans to raise interest rates in July by 25bps, and again in September, by an amount determined by the medium-term inflation outlook. The need for new tools to carry out any “anti-fragmentation” policy does suggest that the pace of rate rises from the ECB will lag those of the Fed.

Looking to that UK economic forecast, we have been predicting a decline in UK GDP of 0.6% this quarter, and we were forecasting growth of 0.1% in Q3 and again in Q4, so a recession was technically avoided. The modest 25bp tightening means a recession is avoidable, but only just. Much depends on consumer confidence. To support consumer spending levels the Chancellor has announced a package of measures worth £15bn aimed at ameliorating the higher cost of energy, the question is whether this is enough? Our forecast depends on consumers being willing to lower their savings rate from just under 7% to less than 3%, with the money not saved being used to meet the higher cost of living. There is every reason to see this as a reasonable path, but the fact that consumer confidence is the lowest it’s been since 1974 does suggest that the negativity is more emotional than rational and thus harder to predict.

Implications for Quantitative Tightening

We believe that the MPC is looking for Quantitative Tightening (QT) to do much of the necessary monetary policy tightening. The Asset Purchase facility has already fallen from £895bn to £866bn, with a further fall of £3.2bn in July, and there is the possibility of an active selling programme coming after the QT report expected in August. One must remember that the QT path we are on remains an uncertain one and central banks are naturally cautious about how rapidly they run down their stock of assets and the broader impact on asset prices generally. On the present path of passive non-reinvestment of funds, 20% of the stock of assets at the bank will be run off by 2025 and 50% by 2030.

James Sproule, Chief Economist