June MPC minutes suggest August rate cut remains in play

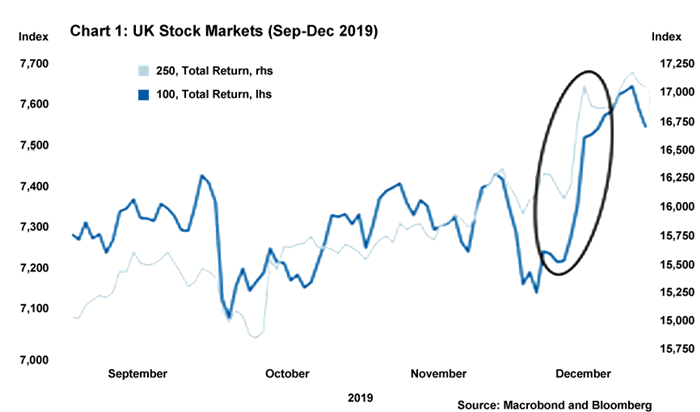

By the time of the next rate wrap, we will know the result of the UK 2024 General Election. It is notable that there have been many occasions in the past when political risk in the UK has been a major influence on the economic and market outlook. For example, when the exit poll for the 2019 general election was published and showed a comfortable Conservative majority, this was followed by firm approval in financial markets. There was a sharp appreciation in UK stock markets and sterling saw a jump against the dollar (see Chart 1). However, no such movements in financial markets are expected on polling day at this election given political risk is perceived to be low.

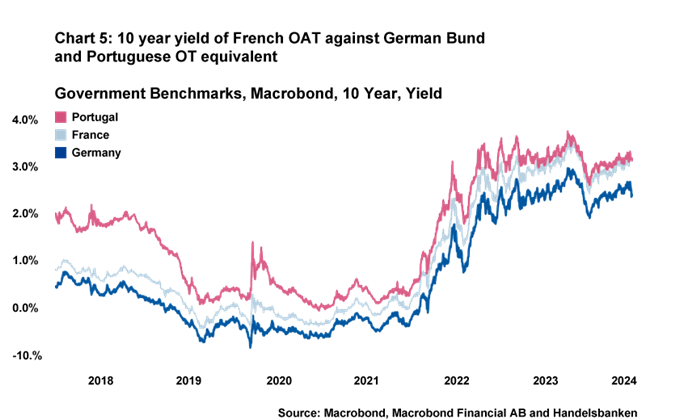

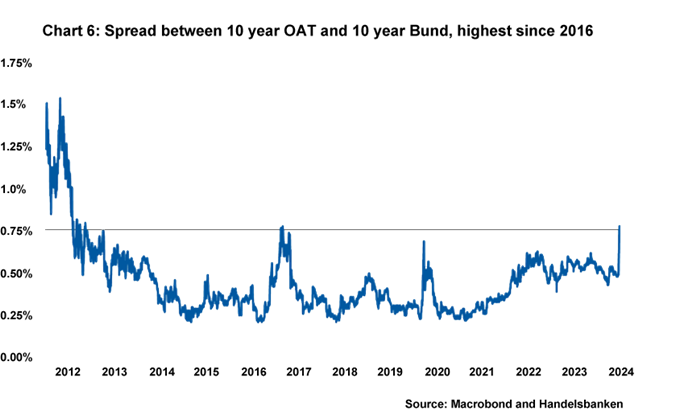

Markets have fully priced in a Labour government and are very comfortable with a prospective Starmer-Reeves administration. In fact, the main political risk to financial markets currently lies across the Channel in France, following President Macron’s surprise calling of a parliamentary election. The prospect of gains by Marine Le Pen’s National Rally party has put significant pressure on spreads between French and German government bonds, which Cam addresses in further detail in this month’s view from the Dealing Desk.

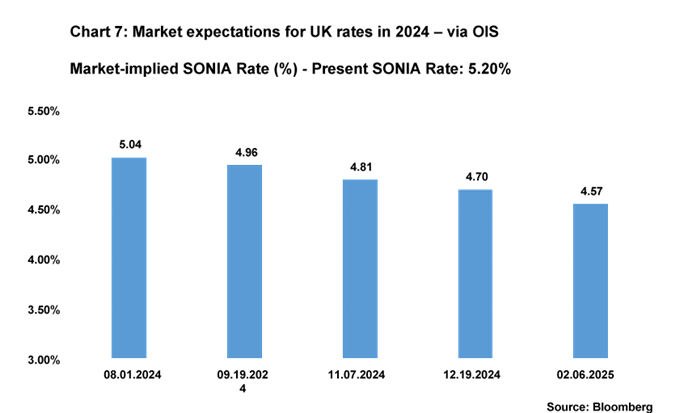

Turning back to UK domestic matters, the Monetary Policy Committee (MPC) announced its latest interest rate decision on 20 June. This, of course, took place in the midst of a General Election campaign, leading to some speculation that rate setters would not cut rates due to fears about being seen to interfere in the electoral process. While the Bank of England (BoE) did, of course, end up holding rates at this meeting, I do not subscribe to the view that politics would have played a role in this decision under current circumstances, or for that matter any other circumstances. The MPC has been at pains to stress that this and other interest rate decisions will be “data dependent”.

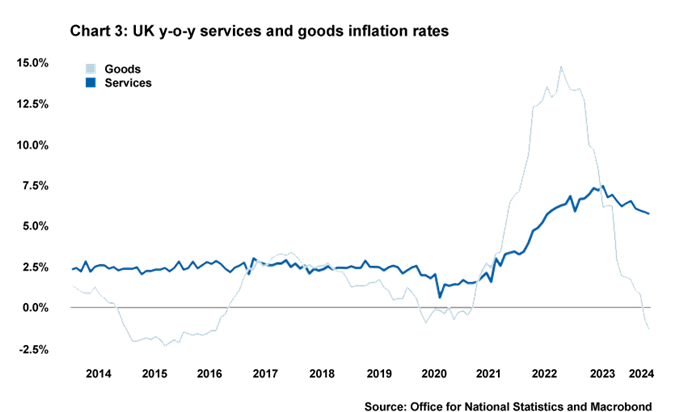

In advance of June’s MPC rate decision, CPI inflation hit the BoE’s 2% inflation target (see Chart 3) but this does not mean “job done”. Inflation will rise again by year end due to base effects in the energy component of CPI and various metrics being tracked by the MPC remain elevated. Both the MPC’s voting breakdown and overall positioning remained the same in June as they did in May: seven members voted to freeze rates; two voted for a 25bp cut; and the majority of MPC members will continue to monitor for signs of inflation persistence in wages, services inflation and labour market tightness.

For there to be a fall in base rate in August, three additional MPC rate setters will need to back a cut. Subject to inflation and labour market data not throwing up any surprises, those MPC members backing a rate freeze in June but subscribing to the “dovish” view on current high services inflation will very likely move their vote for a rate cut in August. So, while the MPC minutes do not give information about the number of MPC members who lie in this camp, they nonetheless give a good indication that a rate cut in August is very much in play. Our view remains that the first rate cut of this cycle will, indeed, be in August with markets (as of 24.06) predicting a 67% chance of this occurring.

Daniel Mahoney, UK Economist