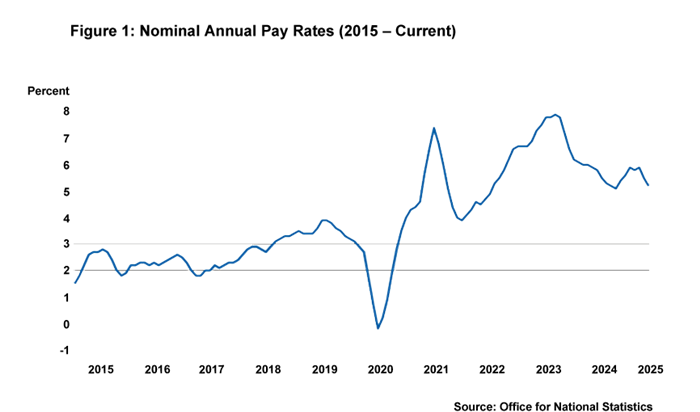

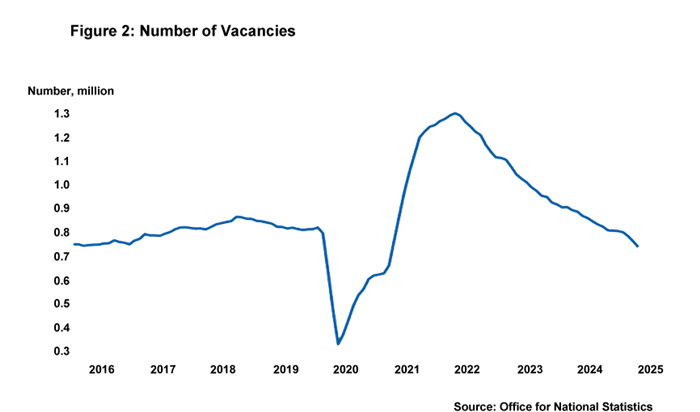

In the run up to June’s Monetary Policy Committee rate decision, most domestic indicators appeared to be pointing in a dovish direction. The labour market has continued to loosen according to numerous metrics. For example, the unemployment rate remains on an upward trajectory, payroll numbers have dropped for seven months running, and vacancies are still falling. Moreover, while remaining elevated, wage rates are showing signs of cooling and Q1’s strong growth went into reverse in April with a m-o-m print of -0.3%.

Yet this still was not enough to convince a majority on the MPC to cut rates in June, as I discussed in a CNBC interview Opens in a new window when the decision was announced. While three members were convinced that monetary policy could be eased by 0.25pp, the other six members voted to hold rates at the current level of 4.25%. Most members on the committee argue that risks to the medium-term pathway of CPI are “two-sided”, meaning they believe that upside risks to inflation remain material. This worry cannot, of course, be easily dismissed given that UK headline inflation is already projected to be north of 3% until at least April next year.

The elephant in the room at the time of the MPC decision was the escalation of conflict between Israel and Iran. At the time of writing, it appears that there has been significant de-escalation but there is clearly a reasonable chance that tensions could rise again over the course of the summer. From a macro perspective, the risks arising from conflict between these two countries – and, by extension, any associated regional conflict – will be seen primarily in the energy market.

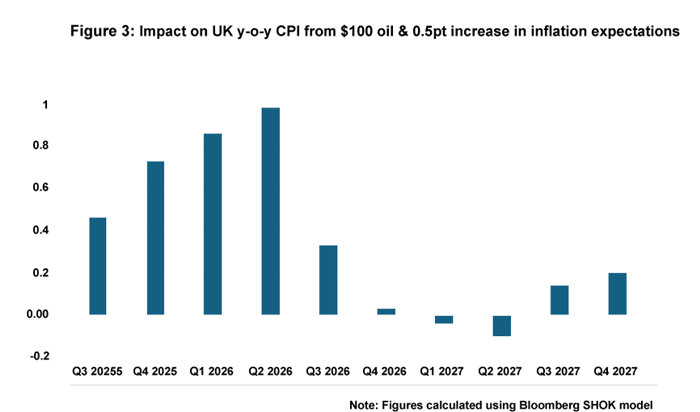

The UK inflation impact arising from a shock to oil prices is worth considering. As discussed in the previous Rate Wrap, UK inflation expectations are showing signs of becoming “de-anchored” (meaning the public’s long-term expectations for inflation may have risen compared to the pre-pandemic norm) which means that rate setters would need to be take any supply-shock induced spike to inflation seriously. When modelling for $100 a barrel oil prices over the course of a year and an increase of 0.5pt in inflation expectations, the increase in inflation is significant (see Figure 3) and would likely warrant a hawkish pivot on the MPC.

For now, that kind of scenario would seem unlikely. Providing domestic indicators of inflation, especially wages and services inflation, continue to show signs of disinflation and there is no unexpected oil price shock, we do appear to be on course for a rate cut in August. We continue to think the cutting cycle will proceed after August although at a cautious pace given the inflation persistence issue. However, the overall landing place for rates in this cycle remains highly uncertain and will depend on whether current and future growth dynamics are driven by either constrained supply or weak demand. This remains a source of disagreement among MPC members, something we will explore in further detail in future rate wraps.

Daniel Mahoney, UK Economist