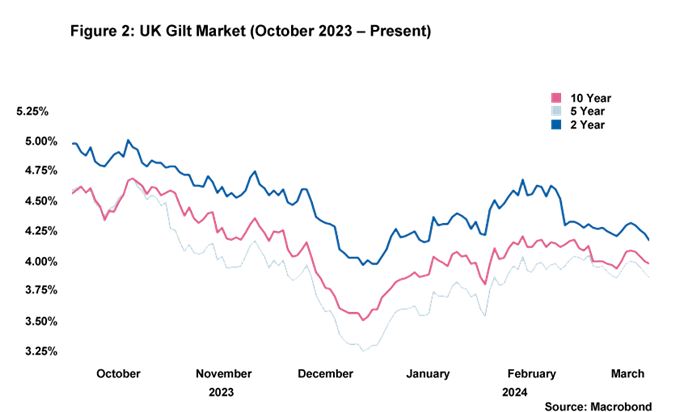

January’s GDP figures would suggest that the UK has emerged out a shallow recession, yet this did not change the very difficult fiscal backdrop facing Chancellor Jeremy Hunt at the March Budget. He had limited fiscal room to cut taxes in a general election year, and as a result, there was very little announced that had not already been publicised across the media in advance. Incidentally, had Hunt been delivering his statement two or three months ago, he would have had quite a bit more room to cut taxes. Ten year government borrowing costs dropped as low as 3.5% at the end of December 2023, but as market expectations for rate cuts started to dial back ten year gilt yields edged back up to around their current level of 4% (see Figure 2 within A view from the dealing desk).

The government will no doubt hope that the medium-term inflation outlook improves over the next few months, potentially reducing borrowing costs and perhaps allowing for one further fiscal event before a general election. After the Budget, we thought Opens in a new window that this would probably mean an autumn election rather than a May election, something the Prime Minister appears to have subsequently confirmed Opens in a new window.

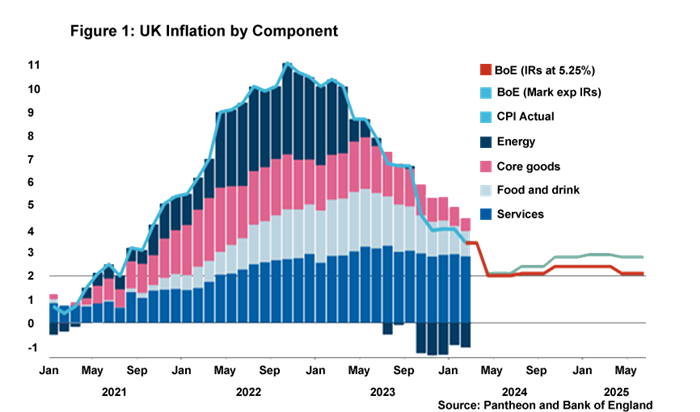

So, what is the current state of play when it comes to the inflation outlook and the prospect of rate cuts? March’s Monetary Policy Committee (MPC) meeting gave us a clue. The voting breakdown indicates a slight “dovish pivot”: the two members voting for a hike in rates in February are now with the majority voting for a freeze in rates. However, the Bank of England’s (BoE’s) overall position remains pretty much unchanged: the MPC will continue to monitor for persistent signs of inflation and review how long Bank Rate should stay at 5.25%. While inflation is expected to meet the 2% inflation target in just a few months’ time, the majority of MPC members need to see further evidence that it can stay at the BoE’s target in the medium term sustainably. In particular, further evidence of cooling nominal wage growth and services inflation is required, although interestingly the minutes of the meeting would suggest there is disagreement among the committee of exactly how much evidence is needed before they can start voting for rate cuts.

Bank of England Governor Andrew Bailey last week clearly indicated that interest rate cuts are "in play" this year. We remain of the view that there are likely to be three rate cuts this year, with the first taking place in the summer. This is a view supported by current market expectations.