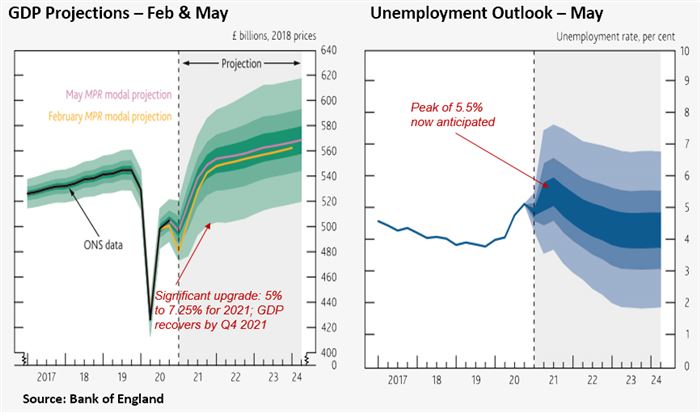

Economic projections for the latter half of 2021 are looking increasingly good and the Bank of England in its latest report reflected this with a whopping increase in the pace of expected growth. As recently as February the Bank of England had forecast GDP growth for 2021 as a whole to be 5.0%, but they have now raised this to 7.25%, which will make this the fastest rate of growth for the UK in the last 80 years.

Any forecast has to acknowledge a number of uncertainties, but looking forward I am remarkably confident on what is going to be driving the economy at least in the short term. This is not an outlook that depends upon raising productivity (something which has proven to be difficult in recent years and where I do not see matters improving particularly quickly) or consumers taking on a lot of new debt (indeed, consumers have been repaying debt leaving their individual balance sheet in better shape than they were before the pandemic). This recovery is being driven in part by income flows which having been saved are now being spent: at least a portion of those accumulated savings are being splurged by consumers and another portion by businesses with a now clearer idea of where to productively invest.

The importance of “forced” savings

The shutdown of our economies lead to a good deal of “forced” savings over 2020 and 2021 – indeed the savings rate rose from its long run average rate of 6% to touch 27% last summer. The result was an accumulation of savings somewhere north of £200bn, more or less evenly split between savings by consumers and those from businesses.

Simply moving consumer spending from being saved to being spent, is the first element supporting the economy in the coming months. In addition there is the potential for at least a portion of the accumulated savings to be spent as well: the Bank of England raised its expectation of this from 5% of accumulated savings to 10% in its most recent report. I think this is still too conservative. The central bank’s analysis, based upon survey data, asked people what they expected to do with their savings, with most people saying they intended to simply continue to save it, the second most common response being to spend. However, my view is that as the recovery gains momentum and residual fears about potential unemployment fade, consumers are going to be willing to dip further and further into their savings. For this reason I have assumed that approximately 20% of savings will be spent over the coming years, a ratio in line with what was spent after the forced savings of the Second World War. To be fair to the Bank of England, they have also indicated that they see the potential for a further rise in the spending of accumulated savings as well.

I am also expecting a good deal of business investment over the next 24 months. Businesses started off 2020 with significant savings, driven in part by concerns over Brexit. However, with a deal now agreed, term planning can be resumed. Perhaps even more critically there are at least some signs of where businesses might productively invest post-pandemic. I can now predict with a bit of certainty that online retail sales will make up 30% of overall sales, up from 20% pre-pandemic; that working remotely which had been the norm for 14% of employees pre-pandemic and hit 38% at the height of the pandemic, is likely to move down to a more sustainable level in the mid 20’s; and that much of the economic pain which has been concentrated in a relatively few sectors is going to stop (benefitting restaurants, and anyone involved in entertainment), while persisting for a few (airlines).

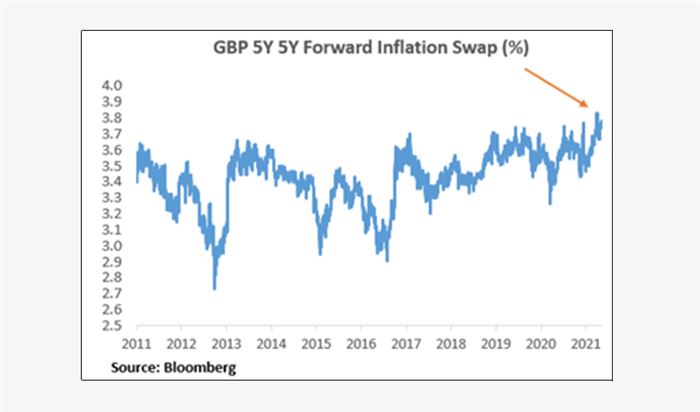

And what about inflation?

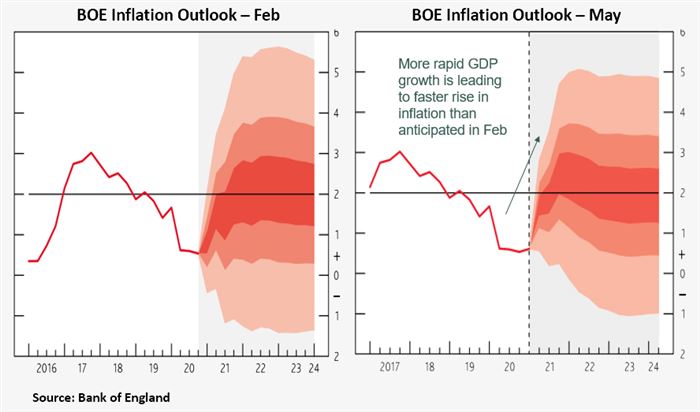

The final question looming ever larger over markets is inflation. Recently I have set out the case for inflation over the next year or so being largely a temporary blip. This was based on three key factors: the base effect, todays inflation is being measured against depressed prices of a year ago; friction, the speed at which consumers start to spend may well overwhelm some businesses which put prices up as a result; and anchored inflationary expectations, people are not expecting or willing to tolerate inflation, thus they will seek alternatives if prices rise. Against this there are growing concerns about input prices, particularly commodities (although commodity prices, barring oil, have traditionally not been a significant enough part of end-product costs to trigger significant inflation) and most importantly the huge expansion of the monetary base, which although it has not lead to inflation over the past decade, could well do in future. Certainly this is something to watch as the economic expansion gathers pace.

James Sproule, UK Chief Economist