PS General Election incoming

Rishi Sunak’s announcement of an election came as a major surprise to most Westminster observers but financial markets were unmoved by the news. Political risk in the UK is minimal at the moment: market participants expect a new government after July 4 and are unconcerned by it. Globally, there is no doubt that there could be major market-moving public policy changes – not least in the United States later this year – but we are unlikely to see such changes in the UK.

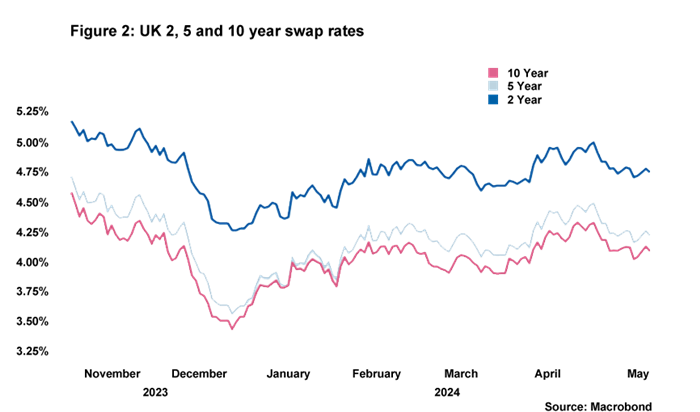

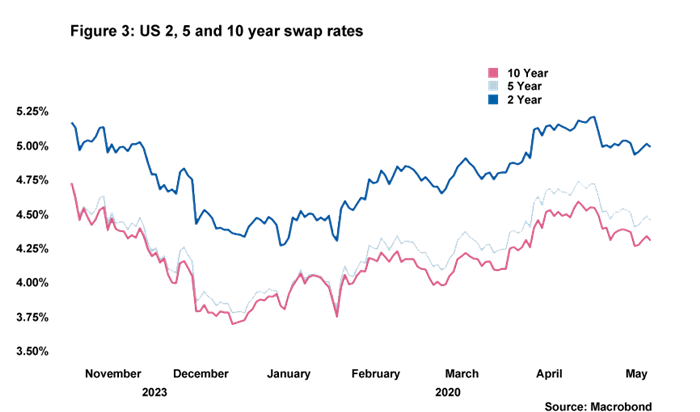

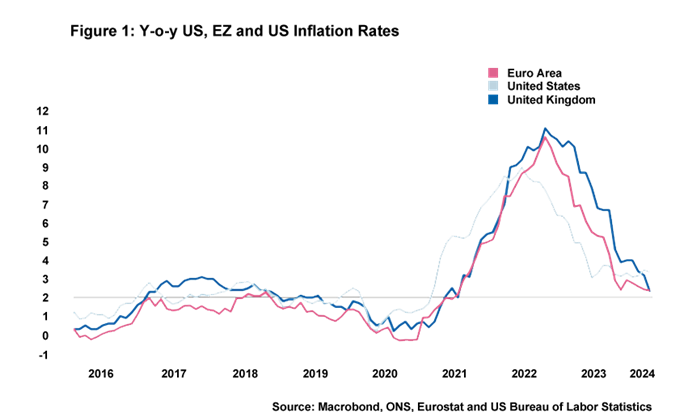

Turning to the latest from the Bank of England, since the last Rate Wrap, we’ve had both an interest rate decision and a new inflation report from the Bank of England. While base rate was held as widely expected, the collective positioning of the Monetary Policy Committee on rate cuts continues to pivot in a dovish direction. Dave Ramsden joined Swati Dhingra in backing a rate cut, leading to a 7 to 2 split on the committee in favour of holding rates. Moreover, the BoE’s new inflation forecast under the assumption that market expectations for interest rates are followed, suggests that inflation will be below 2% by 2026. This is an important signal from the BoE as it suggests its current view is that market expectations for interest rates are too hawkish. Add to this that the UK’s inflation is now notably lower than that in the US, and all the signs were pointing towards a relatively smooth road towards a summer interest rate cut.

However, April’s inflation print has thrown a major spanner in the works. Inflation dropped quite considerably from 3.2% to 2.3%, sitting very close to the Bank of England’s inflation target, but this was above expectations and, crucially, this “upside surprise” was driven by services inflation being stubborn. Markets expected a fall of 0.6pp in y-o-y services inflation but in the event it barely budged and now sits at 5.9%, which remains far higher than the level compatible with the bank’s inflation target in the medium term. Rate setters are scrutinising services inflation especially closely at the moment given how highly influenced it is by wage costs. The bank’s most recent estimates suggest that elevated wage costs are contributing to over four fifths of services inflation. And that, of course, signals signs of persistence in inflation, which may currently be exacerbated by the circa. 10% increase in the National Living Wage that entered into force in April.

This upside surprise to inflation means that a rate cut in June is all but off the table. Before April’s inflation data, markets thought it was a coin-flip as to whether there would be a cut in June; now it is being priced at just a 15% chance (as of 22.05). Of course, it is possible that upcoming data releases could change the calculation once again – there will, after all, be further labour market and inflation figures before the June rate decision – but it would seem unlikely that the data will see enough of an improvement to encourage a further three MPC members to back a rate cut in June.

The first rate cut of this cycle will mark an important moment as it will no doubt help to improve confidence in the UK economy. It is, course, notable now that the June MPC decision will come during the middle of a general election campaign, but the Bank of England will want to ensure that none of its actions could be construed as interfering in the political process and will continue to focus on the data. Our current view is that the direction of travel is for a rate cut in August, although the reaction to April’s inflation figures highlights just how sensitive markets and the MPC are to individual data releases at the moment. So prepare for further surprises along the way…

Daniel Mahoney, UK Economist