Future promises, with an emphasis on future

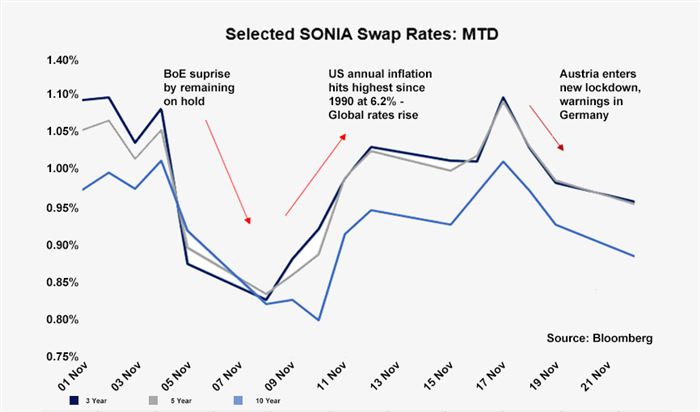

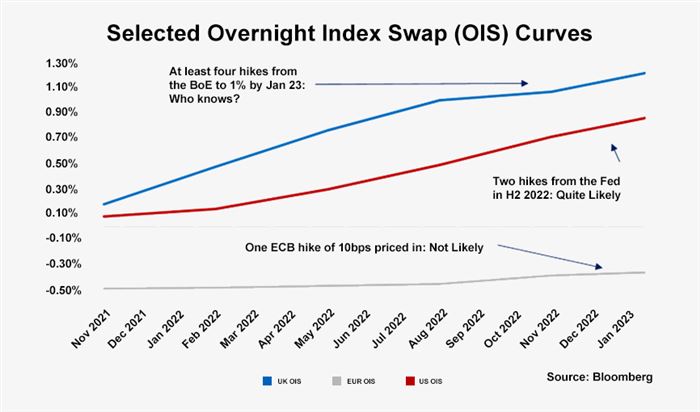

In early November interest rate observers found to their chagrin that they had been over interpreting the pronouncements of the Bank of England Governor Andrew Bailey, and that while interest rate rises remain firmly on the agenda, that are not coming quite a quickly as anticipated. (Should the Governor have done more to correct market misconceptions as they became apparent? Answers on a post card please.) It was in retrospect always a bit of a steep hill to climb to move from the Sept Monetary Policy Committee meeting, when the vote was 9-0 to keep rates at 0.1%, to a majority in favour of tightening. Encouragingly for those of us who think rates should rise, the Committee split its vote by 7-2 in Nov in favour of keeping rates on hold at 0.1%, opening a path forward to tightening. However, despite the (anticipated) surge in Octobers inflationary figures, we note that the next meeting in December will only report the results of the vote, there will not be any more detailed explanation of MPC’s thinking. Thus, our expectation is that a change is most likely in Feb 2022 alongside the next Monetary Policy Report, at which point rates will rise to 0.25%. We expect a further rise to 0.5% in Q4 of 2022, but not much after that as by then consumer demand is likely to have faded.

Parts of inflation may be transitory, but there is more to come before any fading can be expected

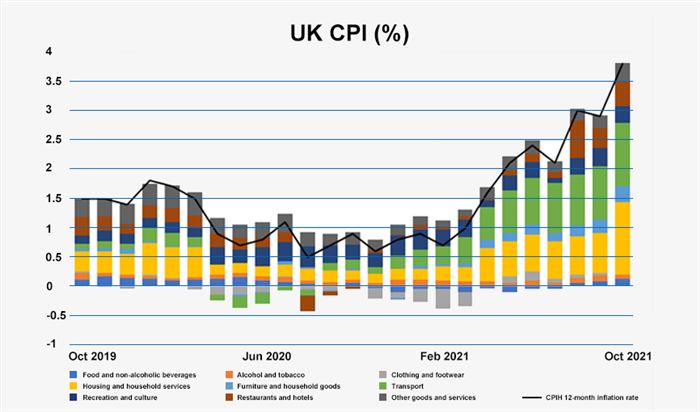

While the Bank of England forecasters maintain that they expect inflation to reach 5% in the first half of 2022, they also maintain that it will fade reasonably quickly thereafter, with inflation expected to be down to its target level of 2% in 2023. The latest data puts inflation at 3.8%, and it looks set to rise further over the autumn and winter as the impact of higher energy prices and tax rises are passed through to consumers; our year-end inflation forecast is for 4.2%. We have for some time argued that much of the inflation story is transitory, and we would continue to argue that the base effect, as well as frictional effects in the labour market opening up post COVID, will pass over the course of 2022. But there have equally always been longer-term inflationary concerns, from a continuation of the above productivity justified wage rises seen in recent months, through to the ultimate impact of significant expansion of the monetary base.

Quantitative Easing: completed

The Bank of England’s Asset Purchase Scheme, known as Quantitative Easing, is now drawing to a close. The November MPC meeting voted by 6-3 to not end the program slightly early, at least some MPC members wishing to signal they would like to see some monetary tightening. Looking forward that signalling disappears as an option as the QE program it is set to reach its goal of GBP 875bn Gilts, GBP 20bn in corporate bonds by the end of Dec. The intention for 2022 remains to cease reinvesting QE proceeds once interest rates hit 0.5% and in the interim the MPC is left to signal its inflationary concerns with either raising rates, giving lots of speeches that they understand the inflationary challenge, or finding some new ways of reinforcing their credibility.

James Sproule, Chief Economist