The crazy volatility we have become used to continued over the course of November, but for the better for many. We left October’s Rate Wrap talking about ballooning government bond yields through returning bond vigilantes, higher inflation compensation and US economic resilience. However markets in their typical rational ways have more or less decided to discard all this on the back of softer data, allowing both short and long-term yields to fall back as a result. The question is whether markets have overreacted, which is not uncommon (more on this below).

Whilst we can perhaps question the extent of the drop in rates, it’s not a huge surprise that rates are off their highs. The early November central bank meetings of the Federal Reserve and Bank of England added no real information to digest, although the latter’s statement and accompanying Monetary Policy Report more or less confirmed rates are at their peak. There is still some fighting talk from the Fed about being ready to act and ensuring that policy remains tight (including chairman Jay Powell himself), but this has been the case since they stopped raising rates in the summer. Oil prices have fallen back and Brent crude is now at $80 a barrel, effectively declining throughout the entirety of November. Concerns around global demand, coupled with no real wider escalation of the Middle East conflict thus far thankfully, have cooled concerns around the oil supply dynamic. Natural gas prices in Europe have been fairly rangebound too during the month.

There is now a little concern that US economic resilience is running out of steam. Official payroll numbers increased by only 150,000 in October, less than the 297,000 figure for September which was also revised down. More importantly when adjusting the payrolls to measure just cyclically sensitive sectors (not government or education payrolls) the number for October drops to just 55,000. The unemployment rate rose slightly to 3.9%, and the monthly increase in average hourly earnings was just 0.2%, when annualised it comes in at just 3.2% - the slowest pace in two and a half years (Pantheon Macroeconomics). Weekly jobless claims data has been steadily rising with ongoing continuing claims currently at 1.865m. These numbers seemed like they were due, judging by survey and other timely data. But what caused the big readjustment in the rates market was the inflation numbers for October, which seemed to be the nail in the coffin for those pricing in a slim chance of any further hikes in the US.

Headline annual inflation fell to 3.2% (below the 3.3% expected) and annual core inflation dropped to 4%, also below expectations. What is more enlightening is the flat monthly reading in headline inflation as well, and within the detail the cooling of owners’ equivalent rent (the rent a property owner would have to pay to be equivalent to their cost of ownership), the largest contributor to the core basket, to 0.4% month-on-month from 0.6% was also notable, and expected to fall further. The market reaction to the numbers across all assets was significant, but driven mainly by rates. 10-year Treasury yields fell close to 20 basis points after the release to 4.45%, and has fallen below 4.4% since then. The shorter-dated 2-year yield mirrored the move in 10 years, falling from over 5% to 4.8% now.

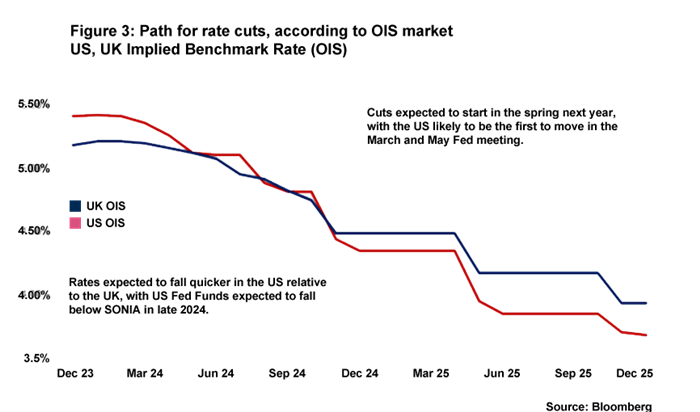

The drop in yields has been driven by the ‘real’ yield component too, reversing a fair chunk of the increase through September and October. It seems as if traders/investors are placing more weight on future expectations of monetary policy where around 100bps of cuts are now priced in for 2024 and 150bps over a two-year horizon, at the expense of concerns around fiscal policy. Bond bulls seem to be returning with the view to lock in higher yields now, and see the value of bond increases given the greater conviction that the Federal Reserve will start cutting rates from the spring onwards. This does not mean that worries around the sustainability of fiscal concerns have gone away, but with Congress agreeing another stopgap package to avoid a shutdown this month, and with plenty of excess cash still able to absorb the supply increase (assets in money market funds that typically invest in short-term US government bills hit a record $5.73trn in November) – its importance has somewhat diminished for the short term.

Circling back to the point around market overreaction, we need to be assessing the pace of any movements in rates going forward. There is enough evidence in November to suggest that the worst may be behind us, and that 10-year Treasury yields above 5% may now be a story of the past. But on the other hand the Federal Reserve (and other global central banks) will not want to see market rates accelerate lower at a similar pace to what we have seen this month as it undoes the work the Fed has done to tighten policy up to this point, which it will want to see hold for a period of time until it’s are even more comfortable that inflation will come back to the target level. Overall, the current conditions have supported a decline in US and global yields, and there is enough conviction across the board that rate cuts are likely across the major economies next year – but we should not get too excited about any further acceleration lower in the future. The conditions seem more suited to a gradual decline in rates over time, but the journey will likely be a bumpy one.

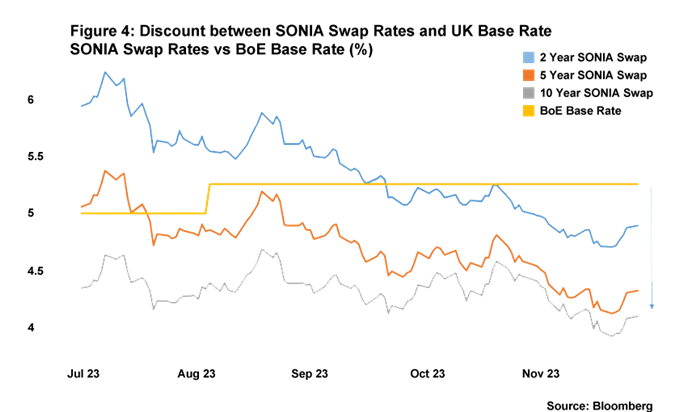

UK Swap rates offering a growing discount to Base Rate

There is no doubt that the events in the US rates market have been the global driver in the past two months, taking the UK rates market along for the ride too. But with the Bank of England now hinting they are at their peak, and with Chief Economist Huw Pill indicating to the market that rate cuts may be on the table by the middle of next year, there is some momentum behind lower swap rates across the whole curve.

With Bank of England base rate at 5.25% (overnight SONIA, another benchmark, trades slightly lower than 5.25%), we are seeing a growing discount between base rate and swap rates, as shown in the chart below. As a reminder, the core of any fixed rate offering in the UK, whether that be mortgages or corporate lending, is these exact swap rates. If we purely look at where the interbank swaps are trading, and don’t take into account the costs on top that would be incorporated into a quote to a borrower, then we can see discounts between 60bps for 2-year swaps to 135bps for 10-year swaps. Remember that these swaps are effectively an average of where markets expect base rate/overnight SONIA rates to be over the period in question, so this builds in the potential for rate cuts already.

However for borrowers who place more weight on the need to improve short-term cash flows they may now be enticed by the discount available, especially on larger quantums of debt. We are seeing interest in swaps pick up, across the entire curve in general, but more so for shorter periods relative to longer fixes. This may be down to jitters around locking in at 4% plus for 7-10 years, given the potential for how far rates can move, whereas the opportunity cost for locking in for shorter periods has reduced with the discount available – despite being at higher rates.

Cameron Willard, Capital Markets

All data in this article, unless otherwise stated, is sourced from Bloomberg