The market is increasingly confident that we are going to see interest rate increases this year, in fact, we may even see two!

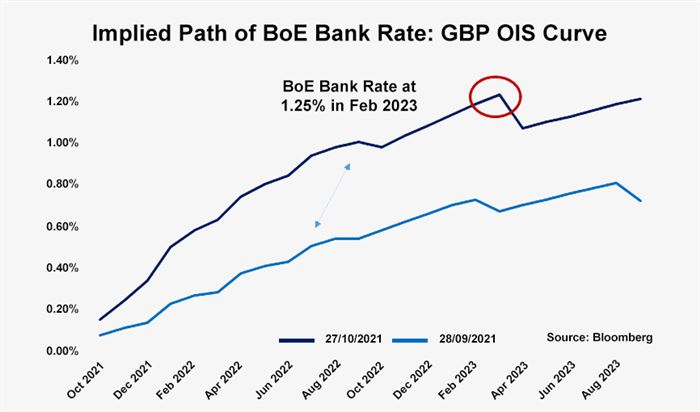

The chart below compares the current market pricing from the last Rate Wrap to what we currently see now, and even in such a short space of time we have seen the timeframe for interest rate increases accelerating dramatically. Money markets are now projecting that we will see a rate hike in next month’s November meeting of 15 basis points, taking BoE Bank Rate to 0.25%, with another 25bps increase in December taking the benchmark rate 0.5%. Looking into 2022-23, by February 2023 the market sees Bank Rate at 1.25%, another three hikes of 25bps.

Central bank media, rather than actual data, have been the driver of the re-pricing through October, with the most blatant communication coming from Governor Andrew Bailey when speaking on an online panel where he said the central bank “will have to act” to curb inflationary forces.. This followed comments from hawk Michael Saunders earlier in the month where he stated that the market was right to price in quicker action from the central bank. We can’t ignore the other side of the coin however, where we find other Monetary Policy Committee members Silvana Tenreyo and Catherine Mann stating their view that more time should be taken before biting the bullet – in fact Tenreyo went as far as saying an interest rate hike could be “self-defeating” (something I will talk about later). Also, reading into Bailey’s remarks however do need some context, as this comment followed talk around medium term inflationary pressure, and seemingly Bailey is still of the believe that current levels of inflation remain in some part transitory.

So why November instead of December? There are arguments to suggest that perhaps there is value in waiting until December where October’s official employment data will be released shortly before. This release is key given it will provide a clearer image on the impact that the end of the furlough scheme had on employment, and therefore labour market slack. An increase in the number of unemployed, as well as increase in the number of underemployed (those who are working fewer hours than they would like), helps to keep a lid on wage growth which is a key ingredient in the recipe of demand led medium term inflationary pressure – which is what the BoE are focusing on. However, one of the main rules of modern central banking is to be clear and concise with the market, providing forward guidance and explanations of decisions so the market is not caught off guard. The November meeting is accompanied by Monetary Policy Report and a press conference which gives the MPC an outlet to explain its decision to hike interest rates, as well as give some form of notice to the market that it will intend to raise rates in December (if they choose to do so).

Given the above and that it is widely expected that the end of the furlough scheme will not adversely affect employment and will not solve all of the labour shortages evident, to me it seems more sensible for lift off to come on November 4th.

Will it be a close call?

The answer is yes, it for sure will not be a unanimous decision. It seems as if we have 2-3 members on either side of the doves and the hawks: Tenreyo, Haskel and Mann for the doves who will not vote to raise rates, whilst Saunders and Ramsden for the hawks who will. That leaves four other members: Bailey, Pill, Broadbent and Cuniliffe. New Chief Economist Huw Pill in his first interview with the Financial Times conceded that the committee makeup is “finely balanced”, and whilst not disclosing how we would vote, he seems to be leaning to the hawkish side as he admitted the current inflationary i=environment is uncomfortable for the central bank. That leaves Bailey Broadbent and Cuniliffe, arguably the three most neutral members, who will be key in swinging the vote. It may hang on Bailey, as its plausible that Broadbent and Cuniliffe vote the way of the Governor, but for the latter two it is rather unknown give how quiet they have been. Either way it will be tight and will likely upset the market if they vote to keep rates on hold.

And longer term?

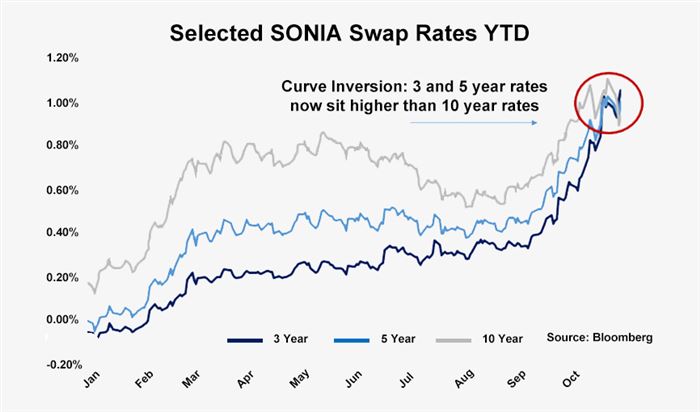

Looking beyond the next year or two becomes a guessing game in many aspects, but what is quite clear amongst market players is that even if rates rise rapidly over the next year, they are not expected to run away. Beyond 2022 the curve has actually inverted, and you only have to look at the swap rates between 3 and 10 years as an example, there’s not much in it as shown below when looking at SONIA swap rates with 3 and 5 year rates rising above 10 year rates.

One explanation could be that as the Bank of England remove stimulus, it will not be by just raising rates, but also via the bank’s balance sheet. Back in the August meeting the BoE confirmed that it will stop re-investing the proceeds of asset purchases (mainly Gilts) when Bank Rate reached 0.5%, which according to market pricing will be the end of this year. The report also confirmed that they may undertake asset sales when Bank Rate reaches 1% which may be achieved by Q3 2022. Therefore as they are tightening financial conditions through asset sales, they may not need to raise interest rates as much. Research by S&P Global on the US QE programme suggests that $250bn of asset purchases is the equivalent of hiking/cutting the Fed Funds rate by 0.25%, and Mark Carney in January 2020 pointed to some research undertaken by the central bank which suggested that £30bn in asset purchases was the equivalent of cutting rates by 0.25% - although the market dynamic is now very different.

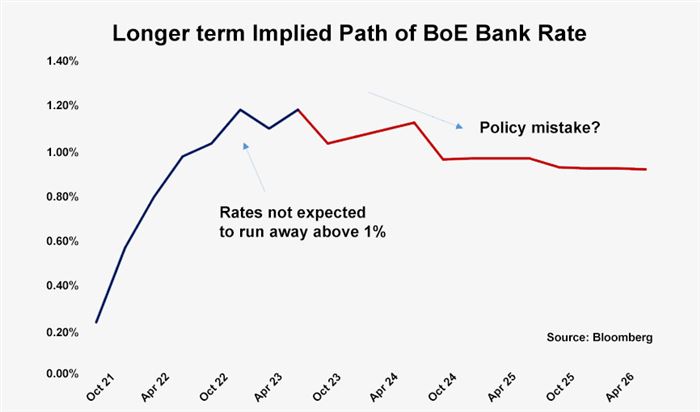

Secondly though, this could indicate that the market sees the potential for a policy mistake, and that the tightening of conditions will weigh on economic growth leading to the re-addition of stimulus from the bank in the years ahead. Remember that raising interest rates will do little to stem supply induced inflationary pressures, whether it be energy shortages or materials shortages that we see now, which erodes the discretionary income available to consumers as prices rise. Couple this with less fiscal support from the government and an increase in the cost of credit from rising rates, and you get a good chance of slower growth. This aides to the “self-defeating” argument made by Tenreyo. Looking at the first chart in this article, but this time with a longer timeframe, we can see that the market sees a potential for rates to come down again in H2 2023When this reversal of tightening could take place is uncertain, but looking at the overnight swap curve on a longer timeframe, the market is signalling for rates to head lower in H2 2023..

The other MPC members will acknowledge this, and perhaps they see it as a worthy price to pay to ensure inflation expectations do not become unanchored. I still find it somewhat puzzling that UK money markets have broken out this far, especially against the US where the market sees a only two hikes in 2022 – perhaps we will see a longer cycle of rate hikes in the US considering inflationary pressures look a little more entrenched.

Unsurprisingly the movements in rates has accelerated interest in hedging products and we on the desk are having plenty of conversations. Conversations around interest rate swaps which swap a floating rate exposure for a fixed rate have certainly picked up again as rate hikes are seemingly around the corner. With the curve inverted too, hedging over longer periods is looking more attractive. Earlier this summer interest rate caps were more popular as market rates were expected to stay low, but in recent weeks the premium to be paid for purchasing a 1.00% cap, a popular choice, has increased sizably.

Please get in touch with your local branch to discuss what hedging options are available.

Cameron Willard, Capital Markets

All data in this article, unless otherwise stated, is sourced from Bloomberg