Interest rate expectations jump again

For the second consecutive time – and for only the second time since it became independent – the Bank of England increased interest rates by 50bp in September. But the Monetary Policy Committee (MPC) was split on the decision: three members backed a 75bp increase; five voted for 50bp; one backed a 25bp increase. The Committee did, however, unanimously agree to Quantitative Tightening (QT) of £80bn over the next twelve months, which will include passive QT (not re-investing the proceeds of maturing assets) and active QT of around £10bn of sales per quarter. Recent data on the UK economy has not been positive, with poor retail sales and consumer confidence figures persuading a number of MPC members to opt for a 50bp increase rather than a 75bp increase. Moreover, the announced energy price cap has dramatically lowered the projected peak of inflation, which is now expected in October as opposed to the end of the year. This energy price cap has improved the short-term economic outlook resulting in the bank feeling less pressure to front-load rate increases.

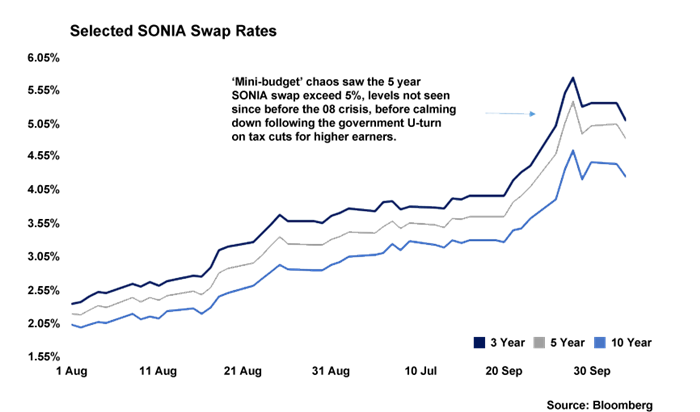

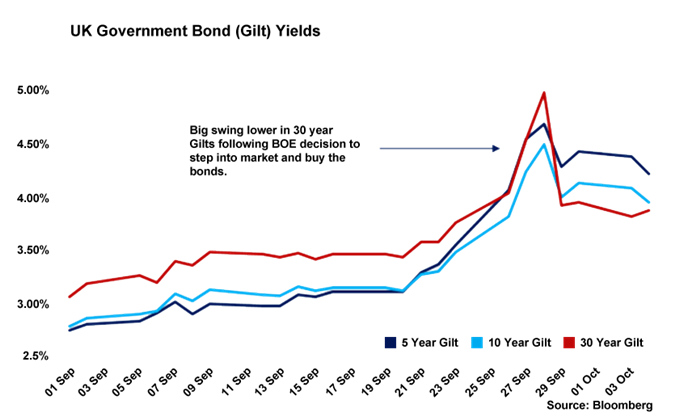

September’s fiscal statement by the Chancellor will now mean the Bank of England adopts an even more vigorous monetary policy. In its recent MPC statement, the bank argued that announcements were likely “to contain news that would be material for the economic outlook” – and, indeed, there were a series of fiscal loosening measures in areas including national insurance, corporation tax and stamp duty which, according to HM Treasury, will cost the exchequer nearly £45bn a year by 2026-27. This, of course, excludes costs associated with the temporary energy price cap. The initial market reaction to the Budget was not encouraging: the pound tanked against the dollar and 10-year gilt yields rose by around 100bp over the course of three days trading, and particular issues surrounding the pensions industry and long-dated gilts led to an intervention by the Bank of England to prop up the market. We will be discussing this in more detail in next month's wrap.

The weakening pound and tight labour market – followed by the negative reaction to the fiscal statement – are prompting markets to price in rapid increases to interest rates. At the time of writing, markets now expect interest rates to be around 5.5% in mid-2023. If interest rates were to reach anything like these levels, there would be a severe impact on UK economic growth prospects as well as a likely correction in the property market.

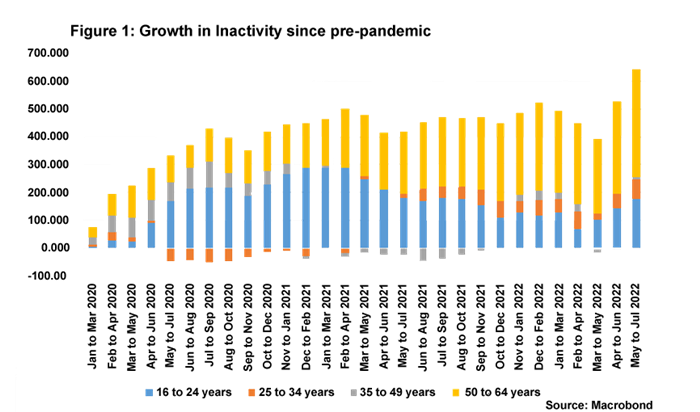

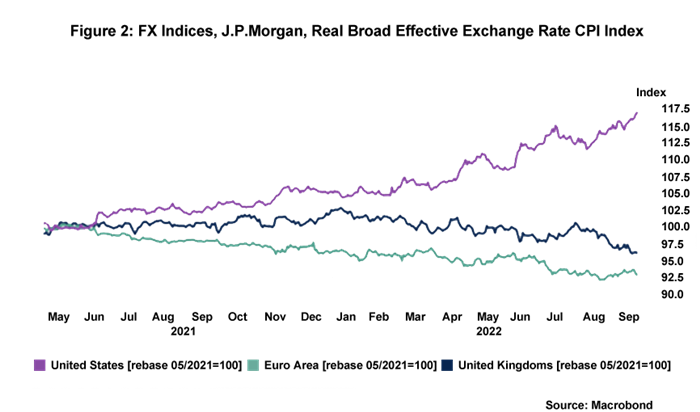

Prior to the fiscal event on 23 September, there were already a number of factors weighing on the minds of MPC members. The latest employment data highlights a UK labour market that remains very tight, with inactivity around 650,000 higher compared to pre-pandemic levels and unemployment registering at just 3.6%. This clearly has the potential to spur on wage growth which is rising in nominal terms, although not for the moment in real terms. And, of course, other central banks are continuing to implement considerable rate increases, including the Federal Reserve's recent 75bp hike. The US's core rate of inflation saw an unexpected jump in August, and the Fed itself has made it clear that the tightening cycle is far from over. MPC members will be mindful of the impact this could have on sterling, which has already seen major falls in recent weeks: in advance of the fiscal event, the British pound was roughly 7% down against the US dollar since early August and the pound's effective exchange rate was down by roughly 4% over the same time period. A weaker pound will, of course, have an inflationary impact given the UK's high import-dependence.