Are we now at the peak?

The Bank of England’s (BoE’s) Monetary Policy Committee (MPC) paused its interest rate hiking cycle in September, but the vote to do so was only passed by the finest of possible margins. Members of the MPC voted five to four in favour of holding rates, rather than increasing them by 25bps, with Governor Andrew Bailey casting the decisive vote.

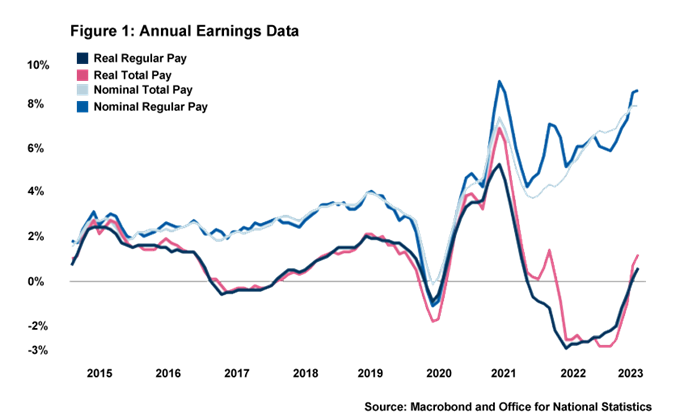

Back in mid-September, no change to interest rates was seen as a very unlikely outcome following the Office for National Statistics’ labour market release. It showed regular private sector pay, a metric examined closely by the MPC, registering at 8.1% in the three months to July, which was 0.8pp higher than the BoE’s estimate released in August. It is true, of course, that the more timely PAYE wage data indicated that pay levels are beginning to ease and there are signs of the labour market continuing to loosen. Yet, this historically high print – which is far from being compatible with a 2% inflation target – seemed to suggest that at least another interest hike was on the cards.

However, August’s inflation numbers changed the calculus. Markets had expected y-o-y CPI inflation to increase but it actually saw a slight fall from 6.8% to 6.7%, and core inflation significantly undershot expectations with notable disinflation being observed in services prices (7.4% to 6.8%). This, along with PMI numbers registering below 50 and therefore indicating a contraction of economic activity, helped tip the balance towards the MPC holding rates steady.

So, at a base rate of 5.25%, have rates finally peaked in this cycle? We feel that we are now probably at that point although markets remain split on the issue. As mentioned in previous Rate Wraps, the full impact of the BoE’s interest rate increases will continue to filter through into the economy so rate setters may now decide simply to allow this to take its course. And, despite a pause in rates, the MPC agreed to tighten monetary policy by continuing its reversal of quantitative easing – “quantitative tightening” (QT). The MPC has agreed to reduce the size of the BoE’s Asset Purchase Programme by £100bn of gilts over the next twelve months, although the BoE would argue this will have a limited impact on tightening financial conditions. Dave Ramsden, MPC member, believes that the £80bn of QT conducted over the previous year has only added around 10bps to the ten-year gilt rate.

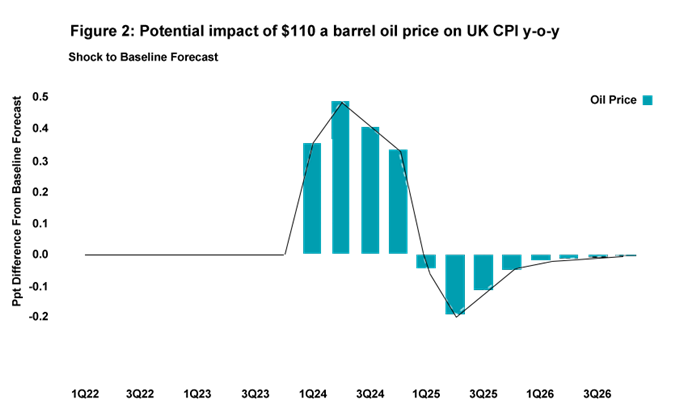

There has been some talk that recent increases in oil prices, driven by Saudi and Russian supply constraints, could somewhat upset the current disinflation trend and risk a second spike in inflation. This is certainly something to watch, but it seems unlikely that movements in the oil price would have anything like the inflationary impact that changes in natural gas prices have had for UK and European economies over the past two years. Bloomberg’s SHOK model, for example, suggests that oil prices moving up to $110 a barrel would only add a maximum of 0.5pp to UK CPI y-o-y inflation at any point.

Nonetheless, getting back to the 2% target will remain a hard slog. If we are at peak rates, it is likely that the MPC will hold rates at 5.25% for the rest of this year and into next year in order to continue its fight against inflation. In future Rate Wraps, we will discuss when rates may start to fall and what MPC members will be considering for future decisions.

Daniel Mahoney, UK Economist